Introduction

Indian commercial and industrial (C&I) businesses exploring solar open access quickly face a critical fork in the road: should you own equity in the generating plant (captive model), or simply purchase power through a PPA from an independent developer (third-party model)?

The choice goes beyond finances. It shapes your regulatory exposure, ESG credentials, operational flexibility, and savings trajectory for the next two decades.

The stakes are real. Choosing the wrong structure can mean paying avoidable cross-subsidy surcharges of ₹2+ per unit, locking into unfavorable contract terms, or leaving lakhs in potential savings unrealized.

Getting it right requires understanding how each model works — operationally and financially — within India's evolving regulatory landscape under the Green Energy Open Access (GEOA) Rules, 2022. This guide covers cost structures, compliance obligations, ESG implications, and the practical criteria that should drive your decision.

Key Takeaways

- Captive open access means you hold equity in the solar plant—either self-owned or through a group captive structure

- Third-party open access means buying power via a PPA with no ownership stake

- Captive is exempt from cross-subsidy surcharges in most states—delivering ₹2–3/unit higher savings for energy-intensive industries

- Third-party requires no capex, deploys faster, and suits an OPEX model, though CSS applies in most states

- The right choice hinges on your load profile, capital readiness, state regulations, and ESG commitments

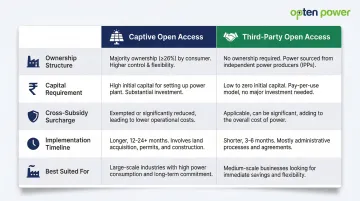

Captive vs Third-Party Solar Open Access: Quick Comparison

| Factor | Captive Open Access | Third-Party Open Access |

|---|---|---|

| Ownership Structure | Equity ownership — self-owned (100%) or group captive (minimum 26% stake) | No ownership; power purchased via long-term PPA (10–25 years) |

| Capital Requirement | Requires upfront CAPEX or equity stake commitment | Zero CAPEX; pure OPEX model funded by developer |

| Cross-Subsidy Surcharge | Exempt in most states under Section 42(2) of the Electricity Act, 2003 | Applicable in most states; ranges from ₹0.13/kWh (Gujarat) to ₹2.11/kWh (Maharashtra) |

| Implementation Timeline | Longer: equity structuring, SPV formation, regulatory approvals | Faster: PPA signing, GOAR registration, wheeling agreements |

| Best Suited For | Energy-intensive industries (steel, cement, data centers) with continuous 5+ MW loads and strong balance sheets | Commercial real estate, IT parks, hotels with 1–10 MW loads wanting savings without capital commitment |

What is Captive Solar Open Access?

Captive solar open access is defined under the Electricity Act, 2003 and GEOA Rules 2022 as an arrangement where the consumer either fully owns the generating plant or holds at least 26% equity in a group captive structure and consumes a minimum of 51% of the plant's annual output.

Unlike third-party consumers who need a minimum 100 kW contracted load, captive consumers face no minimum load threshold. This makes it accessible even for smaller businesses through group captive arrangements.

Two Captive Structures:

| Structure | Who It Suits | Key Condition |

|---|---|---|

| Self-Captive | Single large industrial (10+ MW baseload) with dedicated land | 100% plant ownership |

| Group Captive | Mid-sized C&I companies pooling demand via SPV or consortium | 26% equity stake per member |

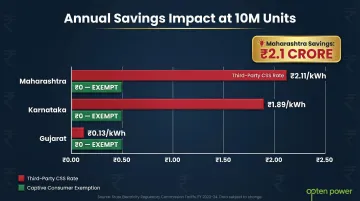

The Financial Advantage: Cross-Subsidy Surcharge Exemption

The most significant benefit of captive structures is statutory exemption from cross-subsidy surcharges (CSS) under Section 42(2) of the Electricity Act, 2003. This exemption is recognized across major industrial states:

- Maharashtra: Third-party consumers pay ₹2.11/kWh CSS for FY 2025-26; captive pays ₹0

- Karnataka: Third-party CSS is ₹1.89/kWh; captive is exempt

- Gujarat: Third-party CSS is ₹0.13/kWh; captive is exempt

For a facility consuming 10 million units annually, this exemption translates to ₹2.1 crore additional annual savings in Maharashtra alone.

Operational Control and Visibility

Captive consumers gain full visibility into plant scheduling, output, and performance. For industries with 24×7 continuous loads, including steel mills, cement plants, data centers, and process industries, this control directly impacts production uptime.

Use Cases of Captive Solar Open Access

- Energy-intensive industries (steel, cement, aluminum, fertilizers) with baseloads above 5 MW see the strongest payoff — the CSS exemption compounds into better long-term economics over a 20+ year horizon

- IT parks and data centers use captive arrangements for round-the-clock cost certainty and verifiable ESG credentials tied to owned generation

- Textile clusters, pharma parks, and industrial estates increasingly form group captive SPVs to share plant costs without any single company funding the full project

The group captive model is gaining traction in Rajasthan and Tamil Nadu, backed by the Supreme Court's October 2023 judgment affirming group captive structures under proportionality rules (consumption within ±10% of ownership).

What is Third-Party Solar Open Access?

Third-party solar open access allows any C&I consumer with a contracted load of 100 kW or more to sign a Power Purchase Agreement (PPA) directly with an Independent Power Producer (IPP). The developer owns, builds, and operates the solar plant entirely. Power is wheeled through state transmission/distribution networks to the consumer's meter, and the consumer pays an agreed per-unit tariff for the PPA duration (typically 15-25 years).

Financial Model: Zero Capital, Higher Regulatory Risk

The consumer makes zero capital investment — the IPP funds everything. Solar tariffs are lower than DISCOM rates, but the effective landed cost must account for:

- Wheeling charges

- Transmission charges

- Cross-subsidy surcharges (the largest variable)

- Scheduling and deviation charges

- Load despatch center fees

Unlike captive consumers, third-party buyers are subject to CSS in most states — and state commissions can revise these surcharges at any time. According to IEEFA's 2022 analysis, the third-party model has become "financially unviable in most states" due to high CSS and Additional Surcharges (AS), with Punjab and Tamil Nadu seeing savings turn negative.

Maharashtra illustrates the risk directly: MERC Order Case No. 226 of 2022 introduced Additional Surcharges with no ceiling, severely impacting third-party OA economics and triggering widespread industry appeals.

Speed and Flexibility Advantage

That regulatory risk does come with a trade-off benefit: speed. Third-party PPAs deploy faster because the consumer only needs to complete PPA signing, GOAR portal registration, and wheeling agreements — no equity due diligence or SPV formation required. For businesses looking to demonstrate ESG progress on a tight timeline, this is the primary draw.

Use Cases of Third-Party Solar Open Access

Third-party open access suits specific business profiles more than others:

- Commercial real estate — Malls, IT campuses, warehouses, and hospitals in the 1-10 MW load range where upfront capex commitment isn't feasible or strategic

- Multi-facility operations — Businesses across multiple states can sign separate PPAs with local IPPs in each state, sidestepping the complexity of inter-state captive structuring; relevant for retail chains, logistics parks, and distributed manufacturers

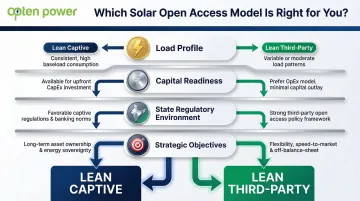

Captive vs Third-Party: Which Model Is Right for You?

The decision framework hinges on four factors:

| Factor | Captive | Third-Party |

|---|---|---|

| Load Profile | Continuous load above 5 MW with 24×7 consumption | Moderate load (1–10 MW) with daytime or variable consumption |

| Capital Readiness | Can commit equity upfront or join group captive SPVs | Need savings without capex; prefer pure OPEX models |

| State Regulatory Environment | States with confirmed CSS exemption (Karnataka, Maharashtra, Rajasthan, Gujarat) | States with lower CSS/AS rates or multi-state operations needing flexibility |

| Strategic Objectives | ESG reporting requires owned generation; maximum long-term cost certainty | Speed to deployment and contractual flexibility outweigh lifecycle savings |

The Grey Zone: Group Captive as a Bridge

For mid-sized companies wanting captive benefits without fully self-funding a plant, group captive SPVs offer a practical middle ground. Opten Power's marketplace supports this decision by letting businesses:

- Compare captive and third-party deals across 16 states in real time

- Evaluate true landed costs including all applicable charges

- Identify group captive pools available for participation

The platform surfaces options without pushing a predetermined model — useful when the right structure isn't immediately obvious.

State-Level Variability

That flexibility matters, because no single answer applies nationally. According to Mercom India's 2025 analysis, Karnataka, Maharashtra, Rajasthan, Tamil Nadu, and Gujarat account for over 85% of solar open access capacity additions, driven by industry-friendly frameworks and clearer CSS treatment. States like Haryana and Andhra Pradesh historically restricted third-party OA through high charges or approval delays, driving consumers almost exclusively to group captive models.

Real World Examples

UltraTech Cement

UltraTech Cement (Aditya Birla Group) acquired a 26% equity stake in AMPIN C&I Power Forty Four's 30 MW solar project in Odisha in March 2026 and a 60 MW solar-plus-storage project by Sunsure Energy in Uttar Pradesh in the same period.

Challenge: Rising DISCOM costs for energy-intensive cement manufacturing and ESG pressure to decarbonize operations

Model Chosen: Group captive with equity participation

Outcome: Long-term tariff certainty and CSS exemption delivering estimated savings of up to ₹0.5/kWh compared to grid tariffs, according to Ember's 2025 cement sector analysis

CapitaLand India Trust

CapitaLand India Trust (CLINT) commissioned a 21 MW captive solar plant in Tamil Nadu in January 2024 to supply 30 million kWh annually to its office spaces.

Challenge: Consistent baseload demand across multiple IT parks and office complexes requiring long-term energy cost predictability

Model Chosen: Captive (given the scale and long-term energy certainty required)

Outcome: Annual supply of 30 million kWh locked in at fixed tariffs, reducing exposure to DISCOM rate revisions across Tamil Nadu operations

Key Takeaway: Captive wins on total lifecycle savings and regulatory predictability where CSS is waived; third-party wins on speed, flexibility, and zero capital commitment. The right model depends on your load profile, capital appetite, and timeline.

Opten Power's marketplace lets you compare tariffs, IRR, and payback across captive and third-party deals across 16 states. See which model fits your load profile before committing to a structure.

Conclusion

Captive and third-party open access each serve distinct business profiles—there's no universal winner. The right choice hinges on load size, capital strategy, state regulations, and operational objectives rather than one model being inherently superior.

| Decision Factor | Lean Captive | Lean Third-Party |

|---|---|---|

| Load size | >2 MW, stable | <2 MW or variable |

| Capital position | Available for CAPEX | Prefer zero upfront |

| State surcharge regime | High CSS exemption benefit | Lower surcharge states |

| Speed priority | Long-term cost certainty | Faster deployment |

Energy-intensive industries in high-surcharge states typically gain ₹2-3/kWh through captive's CSS exemptions and tariff predictability. Businesses that need solar savings without capital exposure get there faster through third-party PPAs.

Before committing to either structure, compare landed tariffs, regulatory costs, and projected savings across both models for your specific state and load profile — the numbers, not the model name, should drive the decision. Platforms like Opten Power let C&I buyers run this comparison across multiple developers in real time, covering both captive and third-party options across 16 states.

Frequently Asked Questions

What is open access solar?

Open access solar is a procurement mechanism under the Electricity Act, 2003 and Green Energy Open Access Rules 2022. It allows C&I consumers to source power directly from solar generators — bypassing their local DISCOM — to reduce costs and meet clean energy targets.

What is the difference between captive and third-party solar open access?

In captive open access, the consumer owns equity in the generating plant (at least 26% for group captive) and consumes 51%+ of generation. In third-party, the consumer simply buys power via a PPA from an independent developer with no ownership stake involved.

Which open access model gives better savings — captive or third-party?

Captive typically offers higher net savings because it is exempt from cross-subsidy surcharges in most states — a ₹2–3/kWh advantage. Third-party can still deliver savings, but CSS applicability reduces net benefit significantly. Capex-constrained businesses often start with third-party and migrate to captive as they scale.

What charges apply under solar open access in India?

Key charges include wheeling charges, transmission charges, cross-subsidy surcharge (CSS), scheduling charges, load despatch center fees, and deviation settlement charges. CSS is the most impactful variable and is often waived or reduced for captive consumers.

Who is eligible for solar open access in India?

Under the GEOA Rules 2022, any consumer with a contracted demand of 100 kW or more is eligible for third-party open access. Captive consumers have no minimum load threshold, making group captive an option even for smaller enterprises.

Can a company participate in both captive and third-party open access simultaneously?

Yes, a company can have a captive arrangement for one facility and a third-party PPA for another. Many large C&I consumers with multi-state operations use a hybrid procurement strategy to optimize savings and flexibility across their portfolio.