This guide covers what open access solar is, how India's market has grown, why C&I companies are shifting away from DISCOMs, the land and regulatory challenges slowing adoption, and how businesses can get started.

Key Takeaways

- Open access solar lets C&I consumers buy power directly from independent producers, bypassing DISCOMs

- India is on track to add 7.8 GW in FY2025, with 45+ GW already in the pipeline

- Businesses cut energy costs up to 40% while meeting Scope 2 emissions targets

- Land acquisition delays and ISTS waiver expiry are major execution bottlenecks

- Instant tariff comparison across 4+ GW of capacity in 16 states — available through platforms like Opten Power

What Is Open Access Solar and How Does It Work?

Open access solar is a regulatory mechanism under the Electricity Act, 2003 that allows eligible C&I consumers to procure solar power directly from independent power producers (IPPs). Instead of buying from the state DISCOM at retail tariffs, businesses use the transmission or distribution grid to wheel renewable power from off-site generators.

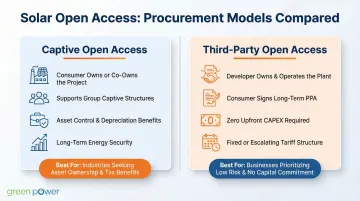

Two Primary Models

| Model | Ownership | Best For |

|---|---|---|

| Captive Open Access | Consumer owns or co-owns the project (on-site or off-site); group captive arrangements allow multiple consumers to co-invest | Large enterprises seeking asset control, depreciation benefits, and shared equity structures |

| Third-Party Open Access | Developer owns and operates; consumer signs a long-term PPA and pays only for delivered energy | Businesses with high grid tariffs but limited CAPEX — zero upfront investment required |

Key Stakeholders and Their Roles

- Renewable energy generator: Produces and sells solar power

- State or central transmission utility: Provides wheeling infrastructure to move power from generator to consumer

- DISCOM: Handles last-mile delivery and billing

- C&I consumer: Buys power, pays wheeling and regulatory charges

Charges Beyond the Solar Tariff

The landed cost of open access solar includes:

- Wheeling charges: Fees for using the grid (₹0.29/unit in Karnataka, ₹0.76/unit in Maharashtra)

- Cross-subsidy surcharge (CSS): Compensates the DISCOM for lost revenue (₹0.60/unit in Karnataka, ₹2.11/unit in Maharashtra for HT-1 industry)

- Additional surcharge (ASC): Recovers stranded fixed costs (₹0.40/unit in Karnataka from March 2026)

- Banking charges: Fees for storing surplus solar generation on the grid for later use

These charges vary significantly by state and must be modeled before signing any PPA. Maharashtra's high CSS erodes viability for some consumers, while Karnataka's lower charges strengthen the business case.

Eligibility Thresholds

Knowing the applicable charges narrows the shortlist of viable states — but eligibility thresholds determine whether a facility qualifies at all.

The Ministry of Power's Green Energy Open Access Rules, 2022%20Rules,2022.pdf) set the national floor at 100 kW of contracted demand or sanctioned load. Karnataka, Maharashtra, Rajasthan, and Gujarat have all aligned to this threshold. Tamil Nadu sets a slightly lower bar at 63 kVA (roughly equivalent, but measured in apparent rather than active power).

This threshold replaced the earlier 1 MW floor, bringing mid-sized industrial and commercial facilities into scope.

India's Open Access Solar Market: By the Numbers

India's open access solar market delivered record performance in 2025. The country added 7.8 GW of open access solar capacity during the year, a 0.5% increase from 2024's 7.7 GW. Cumulative capacity crossed 30 GW by December 2025, with over 45 GW in the pipeline across various stages of development.

State Leaders Driving Adoption

Karnataka led 2025 additions with 24.5% market share, followed by Maharashtra and Rajasthan. These three states account for a disproportionate share of India's C&I solar demand, driven by high industrial load and relatively mature open access regulations.

Q4 2025 told a different story at the state level:

- Maharashtra: 27% of quarterly additions

- Tamil Nadu: 22% of quarterly additions

- Gujarat: 17% of quarterly additions

The shift reflects uneven regional commissioning cycles rather than a change in underlying demand.

Mixed Signals in Q4 2025

Despite a strong annual headline, Q4 2025 recorded a 32% YoY slowdown — 1.6 GW added versus 2.3 GW in Q4 2024. The culprit was timing, not demand. Developers front-loaded installations into H1 2025 to lock in waived ISTS transmission charges ahead of the June 2025 deadline, leaving fewer projects ready for Q4 commissioning.

Why C&I Businesses Are Choosing Open Access Solar

Cost Savings as the Primary Driver

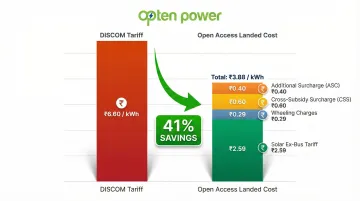

Open access solar tariffs undercut prevailing DISCOM commercial and industrial rates. In Karnataka, BESCOM's HT-2(a) industrial tariff is ₹6.60/kWh plus ₹345/kVA/month demand charge. A typical open access landed cost might be ₹2.59/kWh (ex-bus tariff) + ₹0.29 (wheeling) + ₹0.60 (CSS) + ₹0.40 (ASC) = ₹3.88/kWh—a 41% reduction.

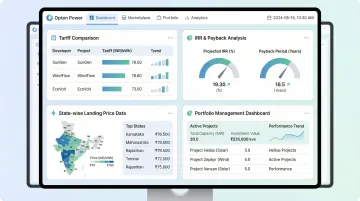

Long-term PPAs (typically 15-25 years) lock in tariffs, shielding businesses from DISCOM rate escalations averaging 5-8% annually. Platforms like Opten Power enable instant tariff comparison across 4+ GW of available capacity, letting buyers compare landed costs and ROI across multiple developers in real time.

ESG Compliance and Scope 2 Emissions Reduction

Open access solar enables direct accounting of renewable energy consumption toward Scope 2 greenhouse gas targets. RE100 technical criteria align with GHG Protocol Scope 2 market-based accounting, allowing companies to claim zero-emission electricity when procuring renewable power via PPAs.

Indian corporate adoption is accelerating on both fronts:

- Over 15 Indian companies are RE100 members, sourcing 39% of their electricity from renewables — including Infosys, Dalmia Cement, Tata Motors, and Mahindra Holidays

- 445 Indian businesses have set SBTi goals, including Wipro, ACC Limited, and UltraTech Cement

CDP climate disclosures align with TCFD recommendations, making verified renewable procurement data essential for investor reporting and sustainable finance access.

Energy Security and Long-Term Price Predictability

Energy costs represent 26-28% of operating expenses in cement manufacturing, 20-40% in iron and steel, and 15-20% in textiles. Long-term PPAs eliminate exposure to fossil fuel price volatility and DISCOM tariff hikes — a direct hedge for any energy-intensive operation.

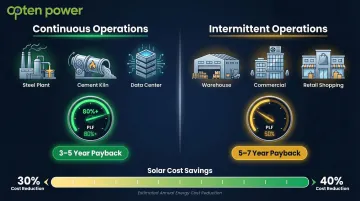

A steel plant running at 80%+ plant load factor (PLF) with predictable 24x7 consumption achieves the highest savings and fastest payback. Intermittent operations like warehouses see lower absolute savings but still benefit from reduced daytime energy costs.

Investor and Lender Confidence

Measurable renewable procurement improves ESG ratings, directly influencing access to institutional capital and green financing. The EU's Carbon Border Adjustment Mechanism (CBAM) adds a harder commercial edge: it applies to aluminium, cement, electricity, fertilisers, hydrogen, and iron and steel exported to the EU, with the definitive phase beginning January 2026.

CBAM could compress profit margins for Indian steel exporters by 9-22%. Since Scope 2 emissions cover purchased electricity, open access renewable procurement directly reduces embedded carbon liability — improving both export eligibility and margin protection.

Sector-Specific Payoff

The math works differently for high-load, 24x7 operations versus intermittent consumers:

- Continuous operations (steel plants, cement kilns, data centres): High consumption at 80%+ PLF means every unit of solar offsets expensive grid power, delivering maximum savings and 3-5 year payback

- Intermittent operations (warehouses, commercial complexes): Lower PLF reduces absolute savings, but daytime solar still cuts peak grid consumption; payback extends to 5-7 years

Data centres and IT parks with ₹10-15/unit grid tariffs see the strongest business case for third-party open access, achieving 30-40% cost reductions with zero CAPEX.

Key Challenges Slowing Open Access Adoption

Land Acquisition Bottlenecks

Developers cite fragmented land ownership, unclear titles, outdated records, and lengthy conversion approvals as major project delays. Securing contiguous, litigation-free parcels near substations is cumbersome and time-consuming.

Specific challenges include:

- Multiple farmers: Assembling 50-100 acres often involves negotiating with 20+ landowners

- Deceased owners: Land records not updated after inheritance, requiring legal clearances

- Conversion delays: Agricultural land conversion to non-agricultural use takes 6-12 months in many states

- Proximity to substations: Land near high-voltage substations commands premium prices; remote land is cheaper but increases evacuation costs

Transmission and Grid Connectivity Constraints

Moving projects to semi-rural or remote locations (where land is cheaper) increases evacuation distances, raises transmission infrastructure costs, and creates right-of-way challenges. Developers must invest in dedicated transmission lines, which can add ₹0.30-0.50/kWh to landed costs.

For C&I buyers, that cost addition is often decisive. When the delivered tariff closes within ₹0.50/kWh of DISCOM rates, the savings case no longer justifies switching.

ISTS Charge Waiver Phase-Out and Its Ripple Effects

The Inter-State Transmission System (ISTS) charge waiver previously exempted solar and wind projects from transmission charges for power wheeled across states. The waiver applied 100% to projects commissioned by 30 June 2025.

For projects commissioned between 1 July 2025 and 30 June 2026, 25% of ISTS charges apply. By July 2028, 100% of charges will apply.

The waiver expiry hit both project economics and developer confidence. Mercom India noted that the phase-out led to front-loaded installations in H1 2025, resulting in a 32% YoY drop in Q4 2025 installations — developers rushed to commission before the deadline, thinning the pipeline for the rest of the year. Inter-state open access projects now carry higher landed costs, pushing many buyers toward intra-state arrangements or hybrid structures instead.

Regulatory Inconsistencies and Approval Delays

Open access rules, banking policies, CSS levels, and connectivity approval timelines vary significantly across states. This creates planning uncertainty for multi-state C&I consumers and developers working across geographies.

Banking rules illustrate how wide that variance can be:

- Gujarat: Allows daily energy banking for solar projects between 7 AM and 6 PM

- Maharashtra: Restricts banked energy drawal to the same or lower Time of Day (ToD) tariff slots; energy banked during solar hours (09:00-17:00) cannot be drawn during peak evening hours

- Karnataka: Allows monthly banking subject to a 4% payment

Cross-subsidy charges add another layer of inconsistency. States like Odisha and Rajasthan levy CSS even on behind-the-meter captive projects — contrary to standard rules that exempt captive consumers. For an industrial plant that budgeted zero CSS, an unexpected ₹0.30-0.60/kWh levy can wipe out the project's payback case entirely.

State Policies and the Regulatory Landscape

Karnataka: Strong Policy Framework, High Industrial Demand

Following the Karnataka High Court striking down the central MoP GEOA Rules 2022, the Karnataka Electricity Regulatory Commission (KERC) issued Terms and Conditions for Open Access Regulations, 2025. The High Court directed that until new regulations are framed, petitioners are entitled to a monthly banking facility subject to a 4% payment.

Karnataka's low wheeling (₹0.29/unit) and CSS (₹0.60/unit) charges make it one of India's most competitive open access markets.

Rajasthan and Gujarat: Land Availability, RPO-Driven Push

Rajasthan issued the RERC Green Energy Open Access Regulations 2025Regulations2025.pdf), providing a detailed banking mechanism for captive RE power plants. The state's abundant land and strong solar irradiation make it a preferred location for large-scale projects.

Gujarat is moving in a similar direction. Its Integrated Renewable Energy Policy 2025 proposes a single-window clearance mechanism to cut approval timelines, while GERC has extended the ₹1.50/kWh banking charge for green open access through June 2026 — giving developers near-term cost certainty.

Maharashtra: Streamlined Non-Agricultural Approvals

Maharashtra is governed by MERC Distribution Open Access Regulations, 2016 and subsequent amendments. A significant recent change: MERC's MYT Order (Case 75 of 2025) introduced "same-slot banking," restricting energy drawal to the same time slot in which it was banked.

In practice, this means C&I consumers can no longer offset nighttime consumption with daytime solar credits — a direct hit to open access economics. That said, Maharashtra's scale and streamlined land conversion processes keep it among the top open access states for large C&I buyers.

Emerging Policy Solutions

Across these states, a consistent set of structural gaps is slowing project velocity. Industry advocates are pushing for policy fixes that address these directly:

- Digitised land records to eliminate title disputes and speed up acquisition

- Pre-approved land banks near substations, ready for renewable project development

- Designated renewable energy zones with pre-cleared evacuation infrastructure

- Unified single-window clearances across state departments

- Enforced 15-day connectivity approvals, as mandated under MoP Green Energy Open Access Rules — timelines that remain inconsistently applied in practice

For C&I buyers and developers, progress on these fronts will matter as much as the tariff framework itself. Shorter project timelines mean faster payback and lower execution risk.

How C&I Businesses Can Get Started with Open Access Solar

Step 1 — Assess Eligibility and Define Objectives

Verify your facility's sanctioned load and state-specific open access thresholds (100 kW in most states). Determine whether captive or third-party open access better suits your capital availability and control preferences.

Before starting procurement, quantify your targets clearly:

- Cost target: A steel plant paying ₹6.60/kWh DISCOM tariff targeting ₹3.80/kWh landed cost aims for 42% savings

- ESG commitment: Are you targeting 50% renewable energy by 2028 to meet RE100 obligations?

- Timeline: Define when savings need to materialise relative to your capex cycle

Anchoring these measurable outcomes upfront keeps developer negotiations focused and avoids scope drift.

Step 2 — Identify and Evaluate Developers

Compare available capacity, project location, PPA terms, tariff structure, and developer track record. In a fragmented market, doing this manually across dozens of developers is slow and opaque.

Opten Power's marketplace (4+ GW of capacity across 16 states) lets C&I buyers compare tariffs, savings, and ROI across developers in real time. Automated RFP engines and pre-approved contracts close deals 50% faster, cutting weeks off manual negotiation cycles.

Opten Power's platform provides:

- Instant IRR, payback, and regulatory analysis

- Standardised, updated landing prices across all states for accurate cost comparisons

- Modular PPA templates that reduce contracting friction

- Portfolio management dashboard to monitor all renewable investments from one interface

Step 3 — Navigate the PPA and Compliance Process

Key elements of an open access PPA include:

- Tariff escalations of 2–3% annually — confirm the cap and base year in the contract

- Contract tenure typically runs 15–25 years, so exit provisions matter

- Force majeure scope — verify whether regulatory changes qualify, not just natural disasters

- Grid connectivity obligations — confirm the developer owns transmission infrastructure and evacuation approvals

Approvals required from state or central transmission utilities include:

- Open access permission from the State Load Despatch Centre (SLDC)

- Connectivity approval from the transmission or distribution licensee

- Metering and scheduling arrangements

Ongoing compliance requirements:

- Renewable Purchase Obligation (RPO) certificate submission

- Renewable Energy Certificate (REC) tracking (if applicable)

- Quarterly energy accounting and reconciliation

Work with experienced advisors or platforms to avoid common contracting pitfalls: ambiguous tariff escalation terms, undefined force majeure scope, or unclear metering responsibilities.

Frequently Asked Questions

What is open access solar and how does it work in India?

Open access solar allows eligible C&I consumers to procure solar power directly from independent producers by using the transmission or distribution network, bypassing the default DISCOM supply, under the framework of India's Electricity Act, 2003.

What is the minimum load required to qualify for open access solar in India?

Most states set the minimum threshold at 100 kW of sanctioned or contracted load (Tamil Nadu at 63 kVA). Thresholds vary by state and procurement mode (captive vs. third-party). Verify exact requirements with your state electricity regulatory commission.

What charges apply on top of the solar tariff in open access procurement?

Main additional charges include wheeling charges (for use of the grid), cross-subsidy surcharge (CSS), additional surcharge (where applicable), and banking/scheduling charges. These vary by state and materially affect the effective landed cost—often adding ₹1-3/kWh depending on the state.

Which states in India have the most favourable open access solar policies?

Karnataka, Rajasthan, Gujarat, and Maharashtra lead on policy clarity, land availability, and industrial demand. Karnataka offers low CSS and wheeling charges; Rajasthan and Gujarat have streamlined approvals; Maharashtra has strong industrial demand, though recent banking rule tightening adds complexity.

How does open access solar compare to rooftop solar for C&I consumers?

Rooftop solar is limited by available roof space and is better suited for smaller loads (typically under 500 kW). Open access (especially third-party or group captive) scales to meet large industrial demand without space constraints, though it involves more complex approvals and additional charges like CSS and wheeling.

What is the impact of the ISTS charge waiver expiry on open access solar?

The ISTS charge waiver expired in June 2025. Projects commissioned after 30 June 2025 face 25–100% of ISTS charges (phased in through July 2028), raising landed costs for inter-state open access and driving a shift toward intra-state arrangements or hybrid models.