Introduction

Data centers now rank among the largest corporate PPA signatories globally. Energy procurement has become a make-or-break strategic decision for digital infrastructure operators — and the pressure is only intensifying.

A Power Purchase Agreement (PPA) is a long-term contract between an energy buyer and a renewable energy developer. As AI workloads scale and power demand climbs, data centers are shifting from reactive spot-market purchases to structured, long-term renewable contracts. Global electricity demand from data centers is projected to more than double by 2030, driven largely by generative AI infrastructure buildout.

The operators who understand these PPA trends are better positioned to manage grid bottlenecks, control rising energy costs, and meet net-zero commitments. Those who don't are increasingly exposed.

Key Takeaways

- Data centres in India are moving away from grid dependency toward long-term open access PPAs for reliable, cost-effective renewable power

- Solar-plus-storage and hybrid solar-wind projects are becoming the preferred stack for meeting round-the-clock (RTC) power needs

- Multi-megawatt, 10-15 year C&I PPA contracts are now the standard as buyers lock in long-term energy cost certainty

- RTC and hybrid renewable projects are gaining ground among 24x7 industrial consumers — data centres, steel, and process industries among them

- Rising AI infrastructure demand is accelerating early-stage procurement, pushing large C&I buyers to secure capacity before project pipelines tighten

The Shift From Virtual PPAs to Physical Power Delivery

Virtual PPAs functioned as financial hedges—corporate buyers contracted for renewable energy credits while continuing to draw power from the utility grid. Physical PPAs, by contrast, involve actual electrons delivered directly to the data center site, often bypassing utility infrastructure entirely.

Hyperscale operators are now co-locating solar or hybrid plants on or adjacent to their campuses under "bring your own generation" models. The driving pressure: grid interconnection queues that can stretch 3-5 years, making traditional utility connections incompatible with AI infrastructure timelines.

The goal is physical certainty of power delivery, direct control over generation assets, and the ability to pace power buildout with phased facility construction.

Examples of direct-connect generation:

- Google acquired Intersect Power ($4.75 billion) to secure gigawatt-scale solar-plus-storage capacity

- Microsoft signed a 20-year, 835 MW PPA for direct power from Three Mile Island nuclear plant

- Meta secured a 20-year PPA for the entire output of an Illinois nuclear facility

The same logic is reshaping energy procurement in India, where the regulatory framework offers its own mechanisms for direct generation access.

The India Context: Open Access PPAs and Captive Power

Open Access PPAs and captive renewable power projects allow data centers and large commercial and industrial (C&I) consumers to contract power directly from generators, bypassing DISCOM dependency for a portion of their load. India's data center capacity is projected to reach 4 GW by FY30, with investments exceeding ₹1.5 lakh crore—making early energy procurement decisions a direct factor in cost and delivery timelines.

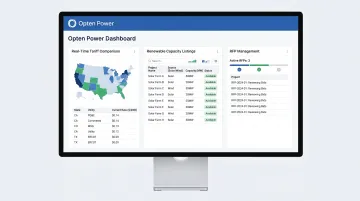

Navigating Open Access PPA procurement across multiple states requires real-time regulatory intelligence. Platforms like Opten Power provide standardized, updated DISCOM landing prices across all states, enabling data centers to compare true PPA costs and make faster procurement decisions without overpaying for grid electricity.

Solar-Plus-Storage as the Core Data Center Power Infrastructure

Battery energy storage systems (BESS) are now a core reliability asset for data centers, not an optional add-on. AI and high-density compute workloads generate power fluctuation patterns the utility grid alone cannot handle. Battery storage steps in to deliver backup capacity and real-time load balancing.

Global BESS growth:

- Utility-scale battery capacity rose 12-fold between 2020 and 2024

- Global BESS deployments soared 53% in 2024

- US battery capacity increased 66% in 2024 alone

That growth reflects a sharper demand signal: hyperscalers now require hourly-matched clean energy, not just annual renewable energy credits. Annual credits no longer satisfy 24/7 carbon-free commitments. Solar-storage configurations address this directly, backing every hour of operation with carbon-free generation.

Hybrid Projects in India

In India, solar-wind hybrid projects offer a practical path to high renewable energy fractions without large BESS deployments. Solar peaks during the day; wind generation picks up at night and through monsoon seasons—together they cover gaps that either source alone cannot.

Key advantages for data centers:

- Maintains reliable power supply across daily and seasonal demand cycles

- Achieves plant load factors significantly higher than single-source projects

- Improves PPA economics by maximising generation across the project lifecycle

Long-Term, Gigawatt-Scale PPA Deals Are Replacing Smaller Contracts

PPA deal sizes and durations have grown significantly. The era of 50 MW, 5-year contracts is over.

Major deals illustrating the shift:

- TotalEnergies signed a 15-year, 1 GW PPA with Google for Texas data centers

- Google secured 1.5 TWh of renewable power for Ohio operations through a 15-year agreement

- Meta signed a 150 MW, 20-year geothermal PPA with Sage Geosystems

Why long terms matter:

- 15-20 year contracts provide price certainty for developers to secure project financing

- Buyers lock in energy costs below projected grid tariff escalation

- PPA prices, despite recent increases to an average of $61.67/MWh in North America — a useful benchmark for global deal benchmarking, still offer long-term savings compared to volatile market rates

These shifts have a direct market consequence: as large buyers lock up available renewable capacity in long-term deals, smaller or later-moving data center operators face a shrinking pool of viable projects and rising prices. The window for locking in competitive rates narrows with each major deal signed.

Diversification Into Firm Renewables — Geothermal, Hybrid, and Beyond

While solar dominates, data centers are increasingly pursuing "firm" or baseload renewable sources—geothermal energy, which runs 24/7 regardless of weather, is gaining traction as an always-on alternative to intermittent sources.

These global deals illustrate how seriously hyperscalers are investing in geothermal capacity:

- Ormat signed a 20-year PPA with Switch for Nevada data centers

- Meta secured 150 MW of geothermal capacity through enhanced geothermal systems

- Google signed a 150 MW geothermal portfolio PPA to support data center operations through NV Energy

- Fervo Energy raised $462 million to accelerate next-generation geothermal deployment

Hybrid Renewables as Accessible Firm Power

Geothermal remains geographically constrained — India has limited viable reserves, making it largely inaccessible for most data center operators here. Hybrid renewable projects (combining solar, wind, and storage) deliver firm power without that constraint, offering a practical path to baseload-quality supply. Hybrid projects can achieve plant load factors significantly higher than single-source projects, improving the economics of a data center PPA.

Benefits of diversified PPA portfolios:

- Reduces availability risk from weather-dependent sources

- Mitigates pricing exposure tied to any single-source dependency

- Higher combined capacity factors translate directly to better PPA economics

- Aligns with 24/7 carbon-free energy goals

What's Driving These PPA Trends in the Data Center Industry

Four converging forces are fundamentally changing how data centers approach energy procurement — and each one is accelerating the others.

AI and Compute Demand Growth

The exponential growth of generative AI infrastructure is the single biggest demand catalyst. Data centers now account for 1-2% of global electricity demand, with projections showing this could reach 4% by 2026. AI workloads require significantly more power than traditional compute—training large language models and running inference at scale drives power density requirements that strain existing grid infrastructure.

Sustainability Mandates and ESG Commitments

Major tech companies and their enterprise clients are bound by net-zero commitments, Scope 2 emissions reporting requirements, and Science Based Targets initiative (SBTi) targets. Over 10,000 companies have now received SBTi validation, and corporate climate target-setting increased 40% in 2025. Renewable energy procurement has become a compliance imperative for most enterprise buyers, not just a cost optimization lever.

Grid Bottlenecks and Interconnection Delays

Traditional utility grid upgrades cannot keep pace with data center load growth. Interconnection backlogs and open access approval delays mean new capacity can take years to come online. That timeline is incompatible with AI infrastructure rollouts, pushing operators toward private wire and direct-connect solutions backed by long-term PPAs.

Cost Efficiency and Procurement Complexity

Managing PPA procurement across multiple geographies means juggling developer tariffs, DISCOM charges, open access regulations, and IRR projections at the same time. For India's data centers, this complexity is compounded by state-level variability across 16+ regulatory jurisdictions.

Platforms like Opten Power address this directly:

- Access 4+ GW of available renewable capacity across solar, wind, and hybrid projects

- Compare real-time tariffs and regulatory costs across states on a single dashboard

- Close deals 50% faster using automated RFPs and pre-approved contract templates

How These Trends Are Reshaping Data Center Energy Strategy

Operational Impact

Energy procurement is becoming a core operational function. Data centers are now embedding energy sourcing into site selection, infrastructure planning, and phased construction timelines — not treating it as a procurement afterthought.

Key operational shifts:

- Private wire configurations allow power buildout to pace with phased facility construction

- Co-locating generation assets reduces reliance on grid interconnection queues

- Direct power agreements enable operational flexibility and load balancing

Business Impact

Capital is concentrating around projects that demonstrate early power procurement and clear paths to grid-independent or hybrid power supply. Developers now hold real leverage as bankable renewable projects grow scarcer in some markets — making early positioning more consequential than ever.

Strategic implications:

- Data centers with secured power procurement gain competitive advantage in site development

- Early movers lock in favorable PPA pricing before market tightening

- Power procurement strategy influences financing terms and project viability

Future Signals

These business dynamics are already shaping near-term policy and technology decisions worth watching.

Watch these near-term developments:

Hourly matching standards: Expanding hourly matching for Scope 2 accounting may push data centers to upgrade from annual RECs to time-matched PPAs, requiring more sophisticated procurement strategies

India's data center market is projected to reach $22 billion by 2030, making early PPA strategy here a tangible source of long-term competitive advantage

Next-generation firm renewables: Enhanced geothermal and next-generation storage are expected to reach commercial scale within 1-3 years, broadening the range of firm renewable options available globally

Frequently Asked Questions

What is a corporate PPA and how does it work for a data center?

A corporate PPA is a long-term contract between a data center and a renewable energy developer to buy power at a fixed or indexed price, either as a financial hedge (virtual PPA) or through direct physical power delivery (physical PPA). This allows the data center to secure clean energy at predictable costs while meeting sustainability commitments.

Which companies are powering data centers with renewable energy?

Major hyperscalers—Google, Microsoft, Meta, and Amazon—collectively account for 50% of global clean energy purchase deals. They're contracting with developers like TotalEnergies, Ormat, and Fervo Energy across solar, wind, geothermal, and hybrid projects to power their data center portfolios.

Are data centers making electricity bills higher for everyone?

In some regions, rising data center demand strains grid infrastructure and can contribute to higher capacity costs for other consumers. Data centers using private PPAs and off-grid solutions help offset this by building independent generation rather than drawing on shared grid capacity.

Where are the newest data centers being built?

India, Malaysia, and Indonesia are among the fastest-growing data center markets in Asia, while the US sees concentrated growth in Texas, Virginia, and Ohio. Across all regions, proximity to renewable energy supply has become the primary factor driving site selection decisions.

Is clean energy still a good investment for data centers?

Clean energy remains a strong investment for data centers. Long-term PPAs lock in cost certainty against volatile grid tariffs, support ESG and net-zero commitments, and are increasingly a prerequisite for AI infrastructure financing and permitting approvals.

How can data centers in India access renewable energy through PPAs?

Indian data centers can procure renewable energy through Open Access PPAs, captive power projects, or group captive structures. Platforms connecting buyers to pre-vetted developers across multiple states simplify this process by enabling real-time tariff comparison, RFP management, and regulatory navigation—helping data centers secure power procurement strategies that align with phased infrastructure timelines.