Introduction

Volatile grid tariffs, mounting investor pressure to cut carbon footprints, and limited visibility into procurement options are pushing businesses toward a clear solution: corporate renewable PPAs. These long-term electricity contracts between businesses and renewable energy developers let companies decarbonize at scale without owning generation assets — and demand for them is accelerating fast.

In 2024 alone, India auctioned a record 59 GW of clean energy capacity — a signal of how quickly this market is maturing. Across Asia-Pacific and Latin America, commercial and industrial buyer participation is at an all-time high. Companies that can't navigate this shift risk falling behind on cost competitiveness, sustainability targets, and investor expectations.

This article covers the four most important trends reshaping how corporate PPAs are being structured and scaled across global markets, what's driving this acceleration, and what forward-looking signals businesses should track.

Key Takeaways

- Corporate PPAs have shifted from niche instruments to mainstream procurement tools, now used across more than 75 countries with rapid growth in emerging markets

- Virtual and sleeved PPA structures offer global flexibility, allowing companies to contract renewable projects regardless of geography

- Multi-buyer aggregation opens PPA access for mid-sized industrial buyers who lack the scale to negotiate independently

- Net-zero pledges, volatile energy prices, and phase-outs of government feed-in tariffs are pushing corporates toward direct renewable contracting

- India is entering a critical growth phase for corporate PPAs, with policy tailwinds and digital platforms cutting deal timelines significantly

Trend 1: Virtual and Physical PPA Structures Are Going Global

Corporate PPAs typically follow two dominant contract structures, each suited to different regulatory environments and buyer needs.

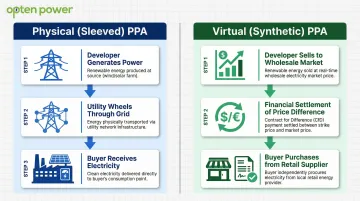

Sleeved (Physical) PPAs

In a sleeved or physical PPA, a utility delivers renewable electricity on the buyer's behalf through the grid. The developer generates power, the utility wheels it through transmission infrastructure, and the buyer receives it at their consumption point.

This structure remains dominant in markets with single interconnected grids—such as parts of Europe and India—where utilities act as intermediaries managing grid balancing and intermittency risk.

Buyers in these markets use back-to-back utility agreements to ensure continuous supply. When solar or wind generation drops, the utility fills the gap with grid power—maintaining operational continuity while the buyer still benefits from renewable energy credits and contracted cost savings.

Where physical PPAs require a shared grid and utility intermediary, virtual structures remove both constraints entirely.

Virtual (Synthetic) PPAs

Virtual or synthetic PPAs are financial contracts where the buyer and developer settle the difference between a strike price and spot price—without physical delivery.

The developer sells electricity into the wholesale market while the buyer continues purchasing from their retail supplier. Each month, they settle the price difference: if the wholesale price exceeds the strike price, the developer pays the buyer; if it falls below, the buyer pays the developer.

Virtual PPAs have become the norm in liberalised markets such as the US and UK because they allow buyers and developers to operate on different grid networks. This eliminates sleeving fees and offers flexibility for companies with dispersed operations.

Managing Basis Risk in Virtual PPAs

Virtual PPAs introduce basis risk when the buyer's retail price and the developer's wholesale settlement price move independently. If retail prices rise while wholesale prices fall, the buyer absorbs a double cost: higher retail bills and a PPA settlement payment to the developer. This risk is managed through:

- Geographic hedging (locating projects near consumption centres)

- Portfolio diversification across multiple projects

- Contractual caps on settlement exposure

- Financial derivatives to hedge price divergence

Pricing Structures Across Both Models

Pricing structures are tailored to whether the buyer wants price certainty or market-linked exposure:

- Fixed-price PPAs lock in a set tariff for the contract term (10–25 years)

- Inflation-linked escalators adjust annually based on CPI or other indices

- Discount-to-market structures with floor and cap provide partial market exposure while limiting downside risk

Long-term fixed-price PPAs (10+ years) are typically required for new-build project bankability, as lenders need revenue certainty to finance construction.

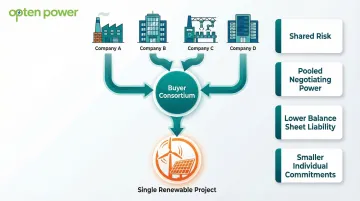

Trend 2: Multi-Buyer PPAs Are Breaking the Scale Barrier

Multi-buyer or aggregated PPA structures allow several corporate off-takers to collectively contract with a single renewable project, making large-scale renewable procurement accessible to companies with smaller energy footprints.

How Aggregation Works

Aggregated structures take two forms:

- Separate individual PPAs where each buyer signs a distinct contract for their portion of project capacity

- Shared buyer vehicle where participants form a consortium or special purpose entity that signs a single PPA, then allocates power and costs among members

Real-World Example: Aggregation in Action

The Melbourne Renewable Energy Project is an early proof of concept: a consortium of public institutions and private buyers collectively procured 110 GWh through a single 10-year PPA. Non-corporate entities led the effort simply because no single participant had enough load to go it alone.

India's C&I sector is following a similar path. Mid-sized manufacturers, IT parks, and commercial complexes — none large enough to anchor a 50 MW project independently — are increasingly exploring group procurement as regulators and developers begin building the legal scaffolding to support it.

Key Advantages

Multi-buyer structures open up procurement to companies that would otherwise be priced out:

- Spreads risk across participants, reducing any single buyer's exposure to project underperformance

- Increases negotiating leverage with developers through pooled demand

- Lowers per-buyer balance sheet liability by distributing project debt across the consortium

- Allows smaller commitments, giving corporates a realistic entry point into long-term renewable contracts

That said, the benefits come with real structural complexity that buyers and developers must plan for upfront.

Complexity Considerations

The operational and legal challenges are worth understanding before committing:

- Competition law requires careful structuring to avoid anti-competitive behaviour among consortium members

- Blended credit ratings of the buyer group directly affect the financing terms developers can secure

- Break-right mechanisms need clear definitions upfront to handle defaults or early exits without unravelling the deal

- Coordination overhead grows with each additional party, especially during contract negotiation

Developers and lenders are increasingly building frameworks to accommodate these structures — because reaching mid-sized industrial buyers requires it. For C&I buyers in India's manufacturing, logistics, and commercial sectors, aggregated PPAs may be the most practical route to securing long-term renewable capacity without the scale of a large multinational.

Trend 3: Emerging Markets—India, Asia-Pacific, and Latin America—Are the New Hot Spots

Emerging markets have crossed a threshold. Economic, regulatory, and technological factors are aligning to make corporate PPA procurement genuinely viable—and increasingly competitive—across India, Asia-Pacific, and Latin America.

India: The Critical Inflection Point

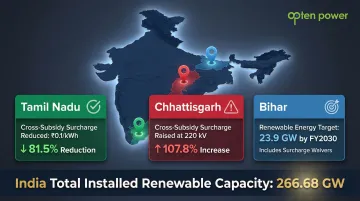

India's corporate PPA market is experiencing rapid maturation driven by converging forces. As of February 2026, India's total renewable energy capacity reached 266.68 GW, including 143.60 GW of solar and 55.13 GW of wind power.

Three policy shifts are strengthening the business case for C&I buyers:

- Open-access charges are being waived through state-level incentives that historically made PPAs unattractive

- Feed-in tariffs are being phased out in favour of competitive auctions, tightening developer pricing

- Renewable Purchase Obligations (RPOs) on corporate buyers are creating a compliance-driven procurement floor

The Ministry of Power's RPO trajectory through 2030 requires obligated entities—including large C&I consumers—to procure escalating percentages of electricity from renewable sources, directly driving corporate PPA demand.

State regulatory environments vary dramatically, which makes tariff intelligence critical:

- Tamil Nadu reduced additional surcharges by 81.5% to ₹0.1/kWh for April–September 2025

- Chhattisgarh raised cross-subsidy surcharges by 107.8% at 220 kV—moving in the opposite direction

- Bihar announced a new policy targeting 23.9 GW of renewable installations by FY 2030, with waivers and energy-banking provisions to attract private participation

Digital platforms are compressing deal timelines. Opten Power's marketplace gives C&I buyers access to 4+ GW of pre-vetted renewable capacity across 16 states, with real-time tariff comparisons, IRR analysis, and state-level regulatory data—enabling deals to close up to 50% faster than traditional procurement routes.

Asia-Pacific: Market Reforms and Supply Chain Pressure

India's scale is matched by accelerating activity across the broader Asia-Pacific region. China is undergoing electricity market reforms to enable direct contracting between corporates and renewable developers. Southeast Asian markets—Singapore and Vietnam in particular—are opening up as multinationals seek to green their manufacturing supply chains, driven by Scope 3 reporting requirements from Western buyers.

Latin America: Unsubsidised Auctions and Landmark Deals

Three markets are driving Latin America's PPA momentum:

- Chile has emerged as a model market—unsubsidised auctions and high wholesale electricity prices create a natural hedge incentive for corporate buyers

- Mexico developed multi-buyer self-supply structures, enabling industrial consortiums to contract shared renewable capacity

- Brazil's non-regulated market for large consumers allows direct bilateral contracting, with landmark deals already signed by mining and manufacturing companies

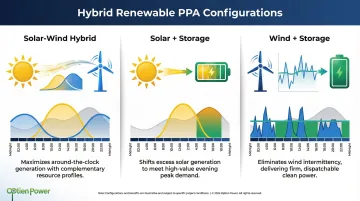

Trend 4: Hybrid Renewable Projects and 24/7 Clean Energy PPAs Are Rising

Traditional single-technology PPAs—solar or wind alone—create timing gaps between generation and consumption, exposing buyers to intermittency and balancing costs.

The Intermittency Challenge

Solar generates only during daylight hours, peaking mid-day when many industrial operations have lower demand. Wind generation varies by season and time of day, often producing more at night. Buyers with continuous operations face grid purchases during non-generation hours, reducing the economic and environmental value of their PPAs.

Hybrid Solutions

Hybrid solar-wind or solar-storage PPA structures address this by combining complementary generation profiles:

- Solar-wind hybrids leverage daytime solar peaks and nighttime wind generation

- Solar-storage projects use batteries to shift solar generation to evening demand peaks

- Wind-storage combinations smooth output and provide dispatchable capacity

In October 2025, ACME Solar Holdings signed a 25-year PPA with Tata Power for a 50 MW Firm and Dispatchable Renewable Energy (FDRE) project at a tariff of ₹4.43/kWh, guaranteeing a minimum annual capacity utilisation factor of 40% and four peak hours of supply with 90% availability.

The 24/7 Clean Energy Movement

Large corporates—data centres, tech companies, and heavy industries with round-the-clock loads—are moving beyond volume-based renewable matching toward 24/7 clean energy procurement frameworks. The shift is driven by scrutiny over what "renewable" actually means on an hourly basis.

Google's commitment to 24/7 carbon-free energy by 2030 illustrates the standard: every kilowatt-hour consumed must be matched with carbon-free generation in the same region at the same time. That's a significant departure from traditional annual matching, where companies buy RECs equivalent to total annual consumption with no regard for when that energy was actually generated.

Market Readiness

Hybrid and 24/7 structures are still emerging, but they're especially relevant in India, where grid curtailment and peak-hour shortfalls make dispatchability a real operational concern—not just a procurement preference. For RE100-committed companies and those under supply-chain sustainability audits, time-matched procurement is moving from a differentiator to a baseline requirement. C&I buyers that move early will be better positioned as disclosure standards tighten.

What's Driving the Global Corporate PPA Scale-Up

Four forces are pushing corporate PPAs from niche instruments to mainstream procurement strategy—and they're all accelerating at once.

Cost Competitiveness

The levelised cost of solar and wind has fallen sharply over the past decade. Research evaluating India's e-reverse auctions between 2017 and 2018 found that the highest winning bids in solar auctions were, on average, 36.49% less than the ongoing solar feed-in tariff in the states that held the auctions. This makes renewable PPAs cost-competitive with or cheaper than grid tariffs in an increasing number of markets.

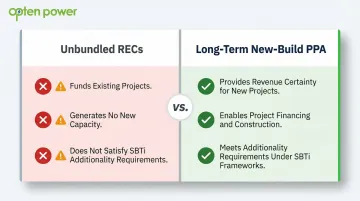

Corporate Net-Zero Commitments

RE100 now includes over 400 member companies pledging 100% renewable electricity. Science-based targets require actual emissions reductions—not just certificate purchases—pushing companies toward additionality-generating instruments like long-term PPAs rather than unbundled Renewable Energy Certificates (RECs).

The distinction matters in practice:

- Unbundled RECs fund existing projects and generate no new capacity

- Long-term PPAs for new-build projects provide the revenue certainty developers need to secure financing

- This additionality is what science-based target frameworks now explicitly require

Policy Inflection: Feed-in Tariff Phase-Out

The global phase-out of fixed feed-in tariffs is pushing renewable developers away from government-backed contracts toward corporate off-takers as their primary revenue certainty mechanism. India formalised this shift when the Ministry of New and Renewable Energy issued Guidelines for Tariff Based Competitive Bidding Process on August 3, 2017, replacing the FIT mechanism with e-reverse auctions.

The result: more PPA-eligible projects entering the market, competing for corporate buyers rather than waiting on government allocations.

Energy Price Volatility

Sharp wholesale electricity price spikes experienced globally—particularly following geopolitical disruptions and fuel price volatility—have heightened corporate demand for long-term price certainty. Fixed-price PPAs provide a meaningful hedge against fuel and carbon price exposure, protecting operating margins from energy cost fluctuations.

Future Signals for Corporate PPAs

Three emerging trends will shape the next wave of corporate PPA evolution.

Scope 3 Accountability

As companies face growing pressure to report and reduce emissions across their value chains, suppliers and manufacturers must contract their own renewable PPAs. This expands the buyer universe well beyond Fortune 500 multinationals to mid-sized industrial companies across sectors like steel, cement, textiles, and logistics.

The cascade effect is significant. Large buyers imposing supply chain sustainability requirements will pull smaller suppliers into PPA markets, multiplying demand across manufacturing ecosystems. Key sectors feeling this pressure first include:

- Steel and cement producers facing embodied carbon scrutiny

- Textile manufacturers under EU due diligence regulations

- Logistics providers tied to Scope 3 reporting mandates

- Industrial suppliers to multinational OEMs with net-zero targets

Digital Procurement Infrastructure

Transaction costs have historically kept mid-sized C&I buyers out of PPA markets. Automated RFP engines, standardised contract templates, real-time DISCOM intelligence, and portfolio dashboards are changing that—compressing timelines and lowering the minimum viable deal size for buyers in emerging markets.

Opten Power's platform reflects this shift directly: instant IRR and payback analysis, real-time tariff comparisons across multiple developers, and automated tender management that cuts procurement timelines by up to 50% for C&I buyers across India's 16 active PPA states.

Regulatory Clarity as the Critical Enabler

For C&I buyers, three regulatory variables determine whether a market is viable: open-access wheeling charges, virtual PPA frameworks, and renewable certificate systems. Where these are transparent and predictable, deal flow follows. Where they remain ambiguous, demand stalls.

India's multi-state policy landscape illustrates the stakes. Dramatic variations in cross-subsidy surcharges and additional surcharges across 16+ active PPA states create real complexity—and real deterrents—for buyers evaluating multi-state procurement strategies.

Standardisation of open-access regulations and transparent, predictable wheeling charges will unlock significant latent demand from C&I buyers currently sitting on the sidelines.

Frequently Asked Questions

What does corporate PPA mean?

A corporate PPA is a long-term electricity contract between a business and a renewable energy developer, with power purchased at a pre-agreed price. Unlike standard utility contracts, it establishes a direct relationship with the generator — delivering both cost certainty and verifiable sustainability credentials.

What is the difference between PPA and corporate PPA?

A traditional PPA is typically between a developer and a utility as the buyer, whereas a corporate PPA replaces the utility with a commercial company as the off-taker. This enables businesses to directly procure renewable power and claim the associated carbon and cost benefits rather than relying on utility-aggregated renewable supply.

How are PPAs structured?

PPAs follow two main structures: the physical or sleeved PPA, where electricity is delivered via a utility intermediary, and the virtual or synthetic PPA, a financial contract settling the difference between a fixed strike price and spot market price. The right structure depends on market regulations and the buyer's geography.

Why are corporates getting real on renewables purchasing?

Falling renewable costs, rising grid tariffs in markets like India, and net-zero commitments under frameworks like RE100 and science-based targets are all accelerating adoption. Companies also need verifiable renewable sourcing — not just certificate purchases — to satisfy investor and stakeholder expectations.

What is EPC and PPA?

EPC (Engineering, Procurement and Construction) refers to the contract under which a developer builds a renewable energy plant, while a PPA is the long-term offtake agreement that determines how the electricity from that plant is sold. An EPC contract precedes and enables the plant construction that a PPA then secures the revenue for.