Introduction

Indian businesses consumed over 1,300 TWh of electricity in 2023, and a growing share of that is now procured directly from renewable sources through corporate power purchase agreements (PPAs). For commercial and industrial (C&I) buyers, this shift isn't optional — grid tariff hikes, tightening ESG disclosure norms, and volatile gas prices are pushing the transition forward whether companies plan for it or not.

Many C&I businesses still struggle to navigate the shift: finding bankable developers, understanding state-level regulations, and locking in contracts before pricing windows close.

This article breaks down where the gas-to-renewables transition stands today — what's accelerating adoption, what's creating friction, and where procurement strategy needs to go next.

Key Takeaways

- Global corporate clean energy PPA volumes fell 10% to 55.9 GW in 2025, the first decline in nearly a decade, yet deals are growing larger and more structured

- Buyers are moving past simple solar and wind contracts toward hybrid, co-located, and firm power solutions for consistent 24x7 supply

- Big Tech hyperscalers control 49% of global corporate clean energy buying, fueling demand for nuclear and geothermal at scale

- Finalizing in late 2027, updated GHG Protocol Scope 2 rules are pushing procurement toward hourly matching and tighter quality standards

- India's C&I renewable market is splitting: early movers are closing complex, multi-technology deals while most buyers still have room to act

Corporate PPA Market at a Crossroads After Nearly a Decade of Growth

After years of uninterrupted growth in corporate clean energy contracting globally, 2025 saw the first meaningful pullback. Corporations announced deals for 55.9 GW of clean power in 2025, a 10% decrease from the record set the prior year.

This pullback is a market-maturation signal, not a reversal of the clean energy transition. The contraction is concentrated among smaller, less experienced buyers struggling with rising project costs, grid complexity, and policy uncertainty — large buyers are actually scaling up their ambitions.

Regional divergence tells the story:

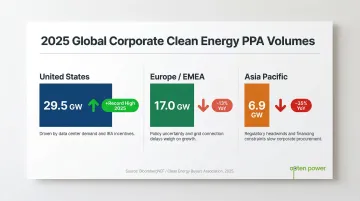

- United States: Set a new record at 29.5 GW, driven almost entirely by Big Tech deals in nuclear, hydro, and geothermal

- Europe (EMEA): Dropped 13% to 17.0 GW as negative power pricing hours eroded standalone solar and wind deal economics

- Asia Pacific: Plummeted 35% to 6.9 GW, primarily due to slowdowns in India and South Korea

The number of unique corporate buyers in the US dropped 51% year-on-year to just 33, indicating severe market concentration.

Why this matters for C&I decision-makers: The "easy era" of straightforward, low-cost solar PPA signing is evolving into a more complex procurement environment where due diligence, deal structure, and counterparty quality matter more than ever. This dynamic is playing out in India too, where C&I buyers face their own layer of complexity — state-level DISCOM rules, open access charges, and a fragmented developer landscape. Buyers who can move efficiently through this environment, whether through experienced advisors or platforms like Opten Power that consolidate project access and automate procurement, are better positioned to secure competitive PPA rates and stronger contract terms.

Simple Solar and Wind Offtakes Are Giving Way to Hybrid and Firm Power Solutions

Simple, single-technology renewable PPAs are losing ground to hybrid structures: co-located solar-plus-storage, wind-solar combinations, and baseload-like products. The shift reflects a fundamental demand change — buyers need reliable, round-the-clock supply, not just lower-carbon power on paper.

Why the Shift Is Happening

Steel plants, cement facilities, data centres, and hospitals run 24x7. Intermittent supply alone doesn't work for them. The push for "firm" or "dispatchable" clean power is a direct operational requirement. In 2025, BloombergNEF tracked 5.8 GW of co-located and hybrid deals globally, with baseload-like products accounting for 5.2 GW of that activity.

Battery Costs Are the Structural Enabler

The global benchmark cost for a four-hour battery project fell 27% year-on-year to a record low of $78/MWh in 2025. As storage becomes cheaper, hybrid deal economics are becoming competitive with simple offtakes.

Concrete examples include:

- Meta's 2.1 GW solar portfolio with 350 MW of integrated storage across ERCOT, SPP, and MISO

- Amazon's 200 MW solar + 100 MW/400 MWh battery energy storage system in California

- Combined 4.7 GW of nuclear power contracted by Meta and Amazon for firm, zero-carbon baseload

The same economics are playing out in India. Recent CERC-approved tariffs for hybrid projects range from ₹2.86 to ₹3.36/kWh — putting solar-plus-storage and wind-solar combinations well within reach for C&I buyers comparing against conventional grid rates.

Big Tech Dominates as Smaller Corporate Buyers Pull Back

Technology hyperscalers—particularly Meta, Amazon, Google, and Microsoft—are responsible for 49% of all global corporate clean energy activity in 2025. Meta and Amazon alone contracted a combined 20.4 GW. This concentration of buying power is reshaping how developers prioritise deals globally — and the pressure is filtering through to commercial and industrial buyers across India too.

The two-speed market reality

As hyperscalers lock up large generation blocks and push developers toward high-complexity bespoke deals, smaller C&I buyers face a more crowded procurement environment. The market remains open, but competing for quality project capacity now demands a sharper approach:

- Real-time DISCOM intelligence to track landing prices across states

- Pre-vetted project capacity with transparent, comparable tariff structures

- Automated RFP management to reduce deal timelines and negotiation friction

- Aggregation mechanisms that give mid-sized buyers comparable leverage

The practical consequence: Mid-sized businesses and industrial buyers can no longer rely on ad-hoc procurement approaches. Platforms like Opten Power are built specifically for this gap — connecting Indian C&I buyers to 4+ GW of renewable capacity across 16 states with the deal infrastructure to close faster and negotiate smarter.

Scope 2 Accounting Changes Are Redefining What Qualifies as Clean Energy

The GHG Protocol—the global standard for corporate carbon accounting—is updating its Scope 2 guidance, with proposed changes that would require hourly matching of energy consumption with renewable generation, and stricter geographic boundaries. While India's regulatory framework operates through CERC's REC mechanism and SEBI's BRSR disclosures, multinational C&I buyers with global reporting obligations are already restructuring procurement in response.

What hourly matching means in practice

Under the proposed hourly matching framework, annual or monthly renewable energy certificate (REC) claims will no longer be sufficient to substantiate "100% renewable" assertions. Buyers will need to demonstrate that clean power was available on the grid at the same hour they were consuming electricity.

Solar attributes, for example, can only cover the hours when solar is produced or discharged from storage. Any gap hours must then be covered by other carbon-free attributes or residual mix emission factors — which is why hybrid portfolios and co-located storage are gaining traction.

Market response is already underway

Forward-looking buyers are already redesigning procurement structures to meet this standard:

- Co-located storage deals enable time-matched supply

- Hybrid portfolios combine solar and wind to smooth output profiles

- Granular certificate trading platforms are emerging to track hourly carbon-free energy

The GHG Protocol's public consultation closed in January 2026, with final publication expected in late 2027.

Once published, buyers still relying on annual REC-based claims will face pressure to restructure portfolios — particularly those with net-zero commitments tied to Science Based Targets or global ESG reporting standards. For India-based operations with cross-border parent companies, aligning domestic procurement with these tightening definitions is becoming a near-term planning priority.

India's Corporate Clean Energy Market — Growing Complexity, Growing Opportunity

India's corporate renewable energy procurement market—one of the largest and fastest-growing in Asia—experienced a slowdown in 2025, contributing to the Asia Pacific regional decline. However, the underlying demand from C&I sectors (manufacturing, steel, cement, data centres, IT parks, hotels) remains structurally strong as tariffs rise and net-zero commitments deepen.

Market bifurcation underway

A small segment of Indian C&I buyers—typically large, multi-site industrials—are moving toward long-term PPAs, open access, and group captive structures with increasing sophistication. The majority, however, are still in the early stages of evaluating their options.

India added 7.8 GW of solar open access capacity in 2025, with the C&I sector's share of overall renewable installations reaching 37.9% in FY2024. As of November 2025, total non-fossil power capacity reached 262.74 GW, crossing the 50% milestone five years ahead of the 2030 target of 500 GW.

Falling Tariffs Create a Cost-Lock Window

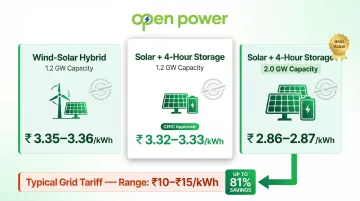

India's 2030 renewable energy targets, falling solar and wind tariffs, and expanding state-level open access frameworks create a window for C&I buyers to lock in long-term energy cost savings. Recent CERC-approved tariffs demonstrate the opportunity:

- 1.2 GW Wind-Solar Hybrid: ₹3.35–₹3.36/kWh

- 1.2 GW Solar + Storage (4-hour): ₹3.32–₹3.33/kWh

- 2.0 GW Solar + Storage (4-hour): ₹2.86–₹2.87/kWh

Key procurement barriers

Navigating DISCOM regulations, state-level tariff variations, and developer quality requires informed procurement decisions. The primary friction points include:

- Complexity of comparing developer proposals across states

- Opaque DISCOM charges and banking regulations

- Slow RFP-to-contract timelines

- Limited visibility into available project capacity

Platforms like Opten Power address these barriers by providing real-time DISCOM intelligence, access to 4+ GW of pre-vetted renewable capacity, and automated RFP management across 16 states, enabling C&I buyers to close deals 50% faster.

Sector-specific opportunity

Heavy industries with 24x7 operations (steel, cement, process industries) and high-consumption services (data centres, hospitals, IT parks) stand to gain the most from locking in renewable tariffs under long-term PPAs. For a mid-size steel plant consuming 50+ MU annually, even a ₹0.50/kWh reduction in landed cost translates to crores in annual savings—while simultaneously satisfying scope 2 emissions reporting requirements.

What's Driving the Corporate Gas-to-Renewables Transition

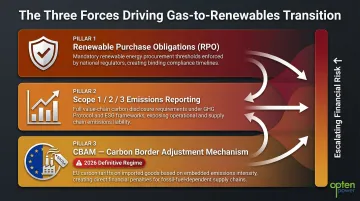

Four forces are accelerating corporate energy switching — and they're reinforcing each other fast enough that inaction is now the riskier financial position.

Cost Competitiveness and Tariff Risk

Renewable energy has become the cheapest source of new power generation globally and increasingly in India. In 2024, the global weighted-average LCOE for onshore wind was $34/MWh and solar PV was $43/MWh — well below fossil fuel alternatives in most markets.

Locking in a long-term PPA price protects against future gas price volatility and grid tariff escalation, making the financial case for transition stronger than it has ever been. For Indian C&I buyers facing grid tariffs of ₹10–15/unit, renewable PPAs at ₹3–5/unit represent savings of up to 40–50%.

Regulatory and Compliance Pressure

Three overlapping compliance pressures are now creating direct financial consequences for energy-intensive industries that stay fossil-fuel dependent:

- Renewable Purchase Obligations (RPOs) — national and state-level mandates with penalties for non-compliance

- Scope 1/2/3 emissions reporting — increasingly required by investors, lenders, and global supply chain partners

- CBAM (Carbon Border Adjustment Mechanism) — an EU import tariff on embedded carbon in steel, aluminium, cement, fertilisers, and other exports

CBAM enters its definitive regime in 2026. Certificate prices will track EU ETS auction rates weekly — meaning the carbon embedded in Indian exports now has a measurable, escalating cost.

ESG and Investor/Customer Expectations

Institutional investors, global supply chain partners, and end customers are increasingly requiring credible renewable energy use as a condition of doing business or securing financing. Approximately 50% of Fortune 500 companies participate in at least one climate initiative, though only 936 companies (10% of studied companies) have committed to sourcing 100% renewable electricity according to CDP.

Technology Enablement and Market Infrastructure

Digital procurement platforms, falling storage costs, and improved grid interconnection have made switching to renewables faster and more accessible. A process that once took years of specialist negotiation can now be initiated through marketplace tools offering instant IRR analysis, automated RFP management, and pre-approved contract templates.

Future Signals for Corporate Clean Energy Procurement

Trends in clean energy buying are shaped by forces that compound over time. These are the developments most likely to reshape corporate procurement strategy in the next 1–3 years:

Storage-integrated PPAs are reaching cost parity with standalone solar deals. With battery costs falling 27% year-on-year and BloombergNEF forecasting a further 25% LCOE reduction in battery storage by 2035, co-located storage is fast becoming the default structure in high-penetration markets where negative pricing hours are rising.

The GHG Protocol Scope 2 update will split the market in two. Once the final standard lands in late 2027, contracts with hourly matching will command a clear premium over legacy annual REC-based claims. Companies still relying on annual RECs will face both a repricing event and a compliance scramble at the same time.

India's state-level policy environment will set the pace for C&I procurement. Open access charges, banking regulations, and group captive frameworks vary significantly by state and are actively shifting. Over the next 24–36 months, the gap between favourable and unfavourable tariffs will widen — making early, informed action the most effective cost lever available.

Conclusion

Corporate clean energy buying is not slowing down—it is maturing. The transition from gas and conventional power to renewables is accelerating in sophistication, even as headline deal volumes fluctuate. Businesses that understand the structural trends and act early will secure better tariffs, better contract terms, and stronger ESG positioning.

The core takeaways are consistent regardless of where you operate:

- Global trends — hybrid power adoption, Scope 2 compliance pressure, and Big Tech-driven demand — are reshaping procurement expectations for all buyers

- India-specific pathways through open access and corporate PPAs offer C&I buyers direct access to competitive tariffs right now

- The pricing window is real: early movers consistently lock in better rates and longer contract terms than latecomers

For C&I buyers, the next move is concrete: compare tariffs across developers, model your savings, and move before your competitors do.

Frequently Asked Questions

What is clean energy procurement?

Clean energy procurement is how businesses source electricity from renewable or low-carbon sources—through mechanisms like PPAs, open access, or green tariffs—to power their operations while reducing fossil fuel dependency and carbon emissions.

Why are corporations increasingly purchasing renewable energy?

Three main drivers are converging: falling renewable tariffs that make it the cheapest available energy option, rising regulatory and investor pressure around ESG and emissions reporting, and the need to hedge against fossil fuel price volatility over long planning horizons.

What is a Power Purchase Agreement (PPA) and how does it work for corporates?

A corporate PPA is a long-term contract between a business and a renewable energy developer that locks in a fixed electricity price for a set period—typically 10 to 25 years. This structure delivers cost certainty and a credible mechanism to claim renewable energy use.

Who is the largest corporate purchaser of renewable energy?

Meta, Amazon, Google, and Microsoft are consistently the top global buyers, collectively accounting for 49% of annual global corporate PPA volumes in 2025. These hyperscalers are driving demand for both traditional renewables and frontier technologies like nuclear and geothermal.

What is the outlook for renewable energy by 2030?

BloombergNEF forecasts global renewables capacity will reach 10.3 terawatts by 2030, though this falls 13% short of the 11.6 terawatts required under the Net Zero Scenario. Achieving this pathway requires an average of $1 trillion (USD) per year invested in renewable energy globally from 2024 to 2030.

How can Indian businesses start their transition from fossil fuel energy to renewables?

Start with three steps:

- Assess your current energy consumption and identify procurement options available in your state—open access, group captive, or third-party PPA.

- Compare developer proposals and tariffs across multiple projects using a unified platform.

- Evaluate the financial case with IRR and payback analysis to confirm viability before committing.