Introduction

Data centres have emerged as the fastest-growing electricity consumers worldwide, with demand surging to approximately 415 TWh in 2024—about 1.5% of global electricity use—and projected to more than double to 945 TWh by 2030, according to the International Energy Agency. As AI-accelerated servers account for nearly half of this growth, Power Purchase Agreements (PPAs) have evolved from niche procurement tools into critical infrastructure that secures affordable, reliable, and clean electricity at unprecedented scale.

Traditional utility contracts can no longer satisfy the reliability, cost predictability, and sustainability demands of modern AI-driven data centres. Grid interconnection queues have ballooned to nearly 2,300 GW in the U.S. alone, with median wait times exceeding four years. Meanwhile, hyperscalers face mounting pressure from Science-Based Targets, 24/7 carbon-free energy (CFE) pledges, and ratepayer protection mandates that require self-provisioned power infrastructure.

These pressures are forcing a fundamental restructuring of how data centres source power. This article examines what's driving that shift: the pivot from virtual to physical power delivery, gigawatt-scale deals driven by AI workloads, mandatory battery storage integration, and "build, bring, or buy" generation policies. For operators in the U.S., Europe, and India's rapidly expanding market, understanding these trends is essential to securing capacity and locking in costs before constraints force reactive decisions.

Key Takeaways

- Data centres are shifting from virtual PPAs to physical, behind-the-meter delivery to bypass grid bottlenecks and guarantee real-time reliability

- AI demand has scaled PPA deals from hundreds of megawatts to gigawatt range — creating a seller-led market where prices are climbing fast

- Battery storage in PPAs is now mandatory for hyperscalers targeting 24/7 carbon-free energy

- Emerging ratepayer protection mandates across the U.S. and beyond are pushing data centres to self-provision power and renegotiate contract terms

- India's data centre build-out unlocks lower tariffs and cleaner compliance pathways through renewable PPAs spanning 16 states

The Shift from Virtual PPAs to Physical, Behind-the-Meter Power Delivery

What Virtual PPAs Were—and Why Data Centres Are Moving Away

Virtual PPAs (vPPAs) have historically dominated corporate clean energy procurement. These are financial contracts-for-difference that settle the gap between a fixed strike price and the prevailing market electricity price, transferring environmental attributes without physically delivering power to the buyer's facility.

According to market documentation, vPPAs served as hedges against price volatility but left buyers exposed to basis risk (the mismatch between contracted project node prices and actual load-zone electricity costs).

For data centres running AI workloads that demand instantaneous power reliability, this structure is inadequate. Virtual PPAs cannot guarantee real-time deliverability when compute spikes occur, nor do they address grid interconnection delays that routinely stretch beyond four years.

Physical PPAs and Direct-Connect Configurations

Physical PPAs involve actual electricity delivery via the grid or private wire, enabling behind-the-meter and direct-connect arrangements. By co-locating renewable generation on or adjacent to data centre campuses, operators bypass sluggish interconnection queues entirely and achieve power delivery certainty that financial hedges cannot provide.

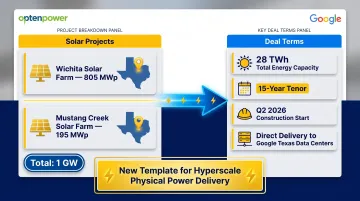

The Google-TotalEnergies Template:

In February 2026, TotalEnergies signed a 1 GW, 15-year solar PPA with Google covering the Wichita (805 MWp) and Mustang Creek (195 MWp) projects in Texas. The deal represents 28 TWh of solar capacity directly serving Google's Texas data centres, with construction beginning Q2 2026. This structure eliminates basis risk and provides phased buildout that matches data centre commissioning timelines—a new template for hyperscale physical power delivery.

Vertical Integration: Hyperscalers Owning Generation Assets

In December 2025, Alphabet acquired developer Intersect Power for $4.75 billion to advance co-located data centre and power sites. The move reflects a broader shift in how hyperscalers approach energy: rather than contracting for power, they are acquiring generation assets outright. For independent developers, this reshapes competitive dynamics — hyperscalers now compete directly with their former PPA counterparties.

Why Physical Delivery Is Accelerating:

- Eliminates basis risk between contracted and delivered power

- Provides grid-bypass certainty amid interconnection delays

- Enables modular phased buildout synchronized with data centre construction schedules

- Supports hourly matching requirements under proposed GHG Protocol Scope 2 updates

AI-Driven Demand Scaling PPA Deals to Gigawatt Proportions

The Magnitude of AI's Energy Appetite

Generative AI has dramatically accelerated data centre energy demand. The IEA projects data centre electricity consumption growing around 15% annually through 2030—more than four times the rate of total electricity demand growth. U.S. data centre demand is expected to rise approximately 130% by 2030, while China's could increase 170%.

This surge has saturated available renewable project supply. As of end-2024, nearly 2,300 GW of capacity sat in U.S. interconnection queues, with only about 13% of projects requesting interconnection between 2000-2019 reaching operation. Median wait times rose from under two years (2000-2007) to over four years (2018-2024).

A Seller-Led Market with Rising Prices

The demand-supply imbalance has flipped the PPA market. In 2025, Amazon, Google, Meta, and Microsoft signed 16,777 MW of renewables contracts—roughly 80% of the 20,448 MW global total. Yet overall corporate clean energy deals fell 10% to 55.9 GW.

2025 PPA Price Movements:

- North American solar and wind PPA prices rose about 9% in 2025

- Q4 2025 solar prices increased 3.2% quarter-over-quarter

- ERCOT wind prices spiked 19% year-over-year

- Median 4-hour battery energy storage agreements reached approximately $13/kW-month

Evolving Deal Structures

As prices climb, standard 10–15 year PPAs are giving way to bespoke risk-sharing agreements. Buyers now accept higher prices, looser structures, and greater variability risk in exchange for securing scarce capacity.

In Texas, wind prices surged on premiums for capacity near data hubs. Market commentary notes that deals are trending toward longer tenors, modular buildouts, and flexible risk allocation to accommodate interconnection delays.

Despite gigawatt-scale individual deals, total corporate PPA volumes contracted. The pool of bankable projects is shrinking due to supply chain constraints, policy uncertainty, and permitting bottlenecks—even as hyperscaler demand surges.

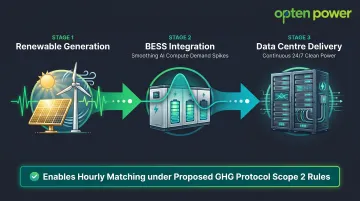

Storage-Backed PPAs Become Non-Negotiable for 24/7 Clean Energy Goals

From "Nice to Have" to Core Requirement

Hyperscalers' 24/7 carbon-free energy targets demand round-the-clock clean power matching that solar or wind alone cannot deliver. Battery Energy Storage Systems (BESS) have moved from optional add-ons to foundational components of data centre PPAs as a result.

In 2025, 108 GW of new battery storage was deployed worldwide, a 40% year-over-year increase that brought global installed capacity to roughly 11 times 2021 levels. India is tracking this momentum, with utility-scale BESS projects gaining ground in renewable-heavy states. Storage-backed PPAs are emerging as a fast-growing product category among corporate buyers.

How Storage-Backed PPAs Work for Data Centres

BESS assets are deployed to manage specific load fluctuations caused by high-density AI compute. When training runs or inference workloads spike, storage systems smooth demand surges that could destabilize local distribution lines. This ensures:

- Continuous clean power delivery across 24-hour cycles

- Grid stability support during demand peaks

- Compliance with hourly matching standards under proposed Scope 2 accounting rules

The Hourly Matching Complication

Proposed changes to GHG Protocol Scope 2 accounting standards emphasize hourly matching and deliverability requirements. A second public consultation is scheduled for 2026, with final publication targeted in 2027.

This tightens what qualifies as "clean" power, raising the bar for how storage assets are integrated into PPA structures. Storage is no longer just operationally necessary; it is becoming mandatory for emissions reporting compliance.

Policy Mandates Are Forcing Data Centres to Self-Provision Power

The Ratepayer Protection Pledge

On March 4, 2026, the White House announced the Ratepayer Protection Pledge, signed by Amazon, Google, Meta, Microsoft, OpenAI, Oracle, and xAI. The companies committed to:

- Build, bring, or buy new generation resources for their data centres

- Cover 100% of power infrastructure upgrade costs without passing them to ratepayers

- Coordinate with grid operators to improve reliability

- Make backup generation available during scarcity events

This landmark policy formalizes the expectation that hyperscalers must self-provision their energy needs, reshaping PPA risk allocation and contract terms.

Texas Legislation and Regulatory Actions

Texas has moved aggressively to protect grid reliability. A 2025 law grants ERCOT authority to disconnect data centres during firm load shed events, pairing mandatory curtailment with voluntary demand response programs. In March 2026, the Public Utility Commission of Texas proposed Rule 16 TAC 25.194 to implement interconnection standards for new 75 MW+ loads, imposing substantial financial and disclosure requirements to mitigate stranded assets.

India's Parallel Mandate Environment

This regulatory pressure extends well beyond the US. India's Renewable Purchase Obligation (RPO) norms, open access regulations, and state-level DISCOM policies are creating a comparable compliance landscape. Data centres increasingly must demonstrate credible renewable procurement — making PPAs not just a cost play but a compliance necessity.

With India's data centre capacity projected to reach approximately 4 GW by FY2030, operators are turning to marketplace platforms to navigate multi-state procurement, compare real-time tariffs, and close deals faster through automated RFP tools — the kind of infrastructure Opten Power was built to support.

What's Driving the Data Centre PPA Market Boom

AI and Compute Infrastructure Growth

The IEA attributes nearly half of net data centre demand growth to accelerated AI servers in its base case. AI workloads are far more energy-intensive than traditional cloud computing, requiring instantaneous power reliability and higher load factors. This has inflated contracted capacity requirements from hundreds of megawatts to gigawatt scale.

Grid Interconnection Bottlenecks

Traditional grid queue delays are a primary driver pushing data centres toward private wire and behind-the-meter PPA configurations. With median U.S. interconnection wait times exceeding four years and only 13% of projects historically reaching operation, physical PPAs that bypass queues entirely have become essential.

Corporate Sustainability Commitments

Science-Based Targets, 24/7 CFE pledges, and ESG reporting requirements create non-negotiable internal mandates for clean power procurement. Renewable PPAs are the preferred vehicle over unbundled RECs or green tariffs because they support additionality—funding new renewable capacity rather than claiming existing supply.

Tariff and Energy Cost Volatility

Rising utility electricity tariffs make long-term locked PPA rates a strategic hedge against energy price volatility. For data centres, energy typically accounts for 40–60% of operating costs — making price certainty a financial priority, not just an operational preference.

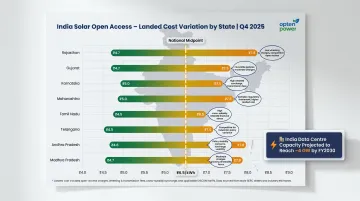

In India, this calculus is especially tangible. Landed costs for solar open access ranged from below ₹5/kWh to about ₹8.4/kWh across states in Q4 2025, with state-level charges creating wide variation. Platforms like Opten Power let operators compare live PPA tariffs, savings projections, and IRR across multiple renewable developers in real time across 16 states — cutting procurement timelines significantly.

Competitive and Financial Dynamics

Early PPA commitments are becoming a competitive advantage. Operators who secure capacity now:

- Lock in pricing before costs rise further

- Secure scarce capacity that will become harder to procure

- Accelerate data centre commissioning timelines in capacity-constrained markets

Future Signals for Data Centre PPAs: What to Watch in 2025–2027

Hybrid Solar-Wind-Battery PPAs Becoming Standard

As 24/7 CFE requirements tighten, single-technology PPAs will give way to bundled hybrid structures combining solar, wind, and storage. Watch for how hourly matching standards evolve under revised Scope 2 accounting rules and how project developers price these bundled structures. Market commentary highlights a shift toward solar-plus-storage and hybrid configurations designed for physical deliverability and hourly matching.

India as the Next Major Data Centre PPA Growth Market

India's data centre capacity crossed about 1,700 MW in 2025, with roughly 440 MW added that year. The 2026 pipeline is approximately 500 MW—implying near 30% year-over-year growth. India's combination of falling solar/wind tariffs, large open-access policy windows, and surging cloud/AI infrastructure investment positions it as one of the most significant emerging markets for data centre PPAs globally.

By November 2025, India's non-hydro renewable installed capacity exceeded 203 GW, providing substantial supply for corporate PPA offtake. Operators can tap into this growing capacity to meet RPO compliance and hedge against volatile DISCOM tariffs. How regulators — both CERC at the centre and SERCs at the state level — formalize open-access rules will determine how quickly that supply becomes accessible to data centre buyers.

Regulatory Tightening on Self-Provisioning

Expect more governments to formalize the "build, bring, or buy" principle — first seen in the U.S. Ratepayer Protection Pledge — into binding frameworks. For Indian data centre operators, the parallel questions sit with state utility regulators and open-access policy. Three regulatory signals worth monitoring:

- Tariff structure: Whether enforceable agreements replace voluntary commitments on grid cost recovery

- Curtailment protocols: How grid operators define and compensate for renewable curtailment events

- Infrastructure cost allocation: Which rules govern who pays for transmission upgrades tied to large loads

Conclusion

Data centre PPAs are no longer a niche procurement vehicle—they have become the central mechanism through which the AI infrastructure boom is being powered, structured, and held accountable to sustainability and affordability commitments.

Several forces are reshaping how data centres source and structure energy:

- Virtual PPAs giving way to physical agreements with direct grid delivery

- Gigawatt-scale deals setting a new floor for hyperscaler procurement

- Storage integration becoming a standard contract requirement

- Policy mandates in the U.S., EU, and India tightening additionality and reporting rules

Operators who move early will secure supply and lock in costs ahead of competitors still relying on legacy utility contracts.

Whether in the U.S., Europe, or India's fast-growing data centre corridor, the ability to move through PPA markets with speed and clear visibility will separate leaders from laggards in the years ahead.

For data centres operating in India, Opten Power provides access to 4+ GW of renewable capacity across solar, wind, and hybrid projects. Operators can compare real-time tariffs across 16 states and close deals up to 50% faster through automated procurement tools and pre-approved contract templates.

Frequently Asked Questions

What is a Power Purchase Agreement (PPA) for data centres?

A data centre PPA is a long-term contract between a data centre operator and a renewable energy developer or generator to purchase electricity at a pre-agreed price and volume. It helps operators secure cost-stable, clean power while supporting new renewable capacity development.

Why are data centres shifting from virtual PPAs to physical PPAs?

Virtual PPAs are financial hedges that do not guarantee actual power delivery, whereas physical/direct-connect PPAs ensure on-site or behind-the-meter delivery. Physical PPAs bypass grid interconnection queues and provide the instantaneous power reliability that AI compute loads demand.

How does AI growth affect data centre energy procurement?

AI workloads are far more power-intensive than traditional cloud computing, pushing deal sizes to gigawatt scale and creating a seller-led PPA market. Buyers now face higher prices and increasing competition for a shrinking pool of bankable renewable projects.

What role does battery storage play in data centre PPAs?

Battery energy storage systems (BESS) are integrated into data centre PPAs to smooth compute load fluctuations and ensure round-the-clock delivery against 24/7 carbon-free energy (CFE) goals. Storage-backed PPAs are increasingly standard for hyperscale operators.

What does the Ratepayer Protection Pledge mean for PPA markets?

The pledge holds major tech companies accountable for self-provisioning their power infrastructure, directly accelerating PPA deal volumes and reshaping contract risk allocation. It is also setting a regulatory template that markets including India are beginning to follow.

How can Indian data centres benefit from renewable energy PPAs?

India's open access framework, falling renewable tariffs, and RPO compliance requirements make PPAs a strong financial and compliance fit for data centre operators. Platforms like Opten Power give operators access to 4+ GW of solar, wind, and hybrid capacity across 16 states, with real-time tariff comparisons and automated tools to close deals faster.