Introduction

India's solar PPA market is not slowing down in 2026 — but it looks very different from even two years ago. Rising open access charges, revised group captive regulations, and the rapid rise of hybrid solar-wind-storage projects are forcing C&I buyers to rethink how they structure long-term energy contracts.

A solar Power Purchase Agreement (PPA) is a contract where a developer installs, owns, and operates a renewable energy project while the business buyer purchases electricity at a pre-agreed tariff over a fixed term (typically 12 to 25 years). For India's commercial and industrial (C&I) sector, PPAs remain the primary route to affordable renewable power without upfront capital expenditure.

This article breaks down what's changed, what's driving adoption, and what C&I buyers need to evaluate before signing a PPA in the current market.

Key Takeaways

- Solar PPAs in India are being used more in 2026, especially by large C&I enterprises

- Heavy industries are choosing group captive PPA structures to access the lowest available renewable tariffs

- Data centres and round-the-clock operations now routinely require hybrid and storage-linked PPAs

- PPA terms are evolving: shorter durations (12–15 years), flexible pricing, and risk-sharing clauses

- Grid tariff inflation, India's 500 GW renewable target, and open access reforms are pushing more businesses off the grid

Are Solar PPAs in India Being Used More or Less in 2026?

The answer is clear: significantly more.

Unlike Western markets where corporate clean energy buying fell 10% in 2025 due to policy uncertainty, India's C&I PPA market has surged. India added a record 6.9 GW of solar open access capacity in 2024, followed by 7.8 GW in 2025, bringing cumulative installed solar open access capacity to over 30 GW by December 2025.

Three structural forces explain India's divergence from global trends:

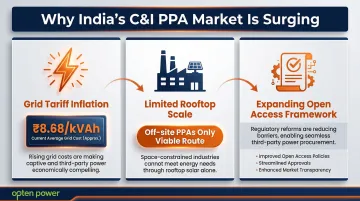

- Persistent grid tariff inflation — Industrial tariffs in states like Maharashtra now reach ₹8.68/kVAh, making locked-in PPA rates highly attractive

- Limited rooftop scale — Most large industrial facilities lack sufficient rooftop area for captive installations, making off-site PPAs the only viable route to renewable energy at scale

- Expanding open access framework — Despite state-level resistance, central regulations are steadily easing barriers for corporate renewable procurement

The buyer profile has shifted noticeably. Fewer small commercial buyers are signing PPAs — complex open access procedures make entry difficult at that scale. Large enterprises now dominate: data centres, steel producers, cement manufacturers, textiles, and IT parks are signing multi-megawatt deals ranging from 50 MW to 1 GW+.

This reflects both the scale economies of PPA contracting and the regulatory sophistication required to operate in India's open access market.

India's national target of 500 GW renewable capacity by 2030 — with the country already at 283.4 GW by March 2026 — keeps developer activity robust and project availability strong. At that scale of activity, structured procurement infrastructure becomes essential. Platforms like Opten Power — with access to 4+ GW of renewable projects across solar, wind, and hybrid across 16 states — give C&I businesses a real-time view of available deals, so they can move faster without the friction of fragmented developer outreach.

Corporate and Group Captive PPAs Dominating C&I Solar

Two PPA structures dominate India's C&I renewable market:

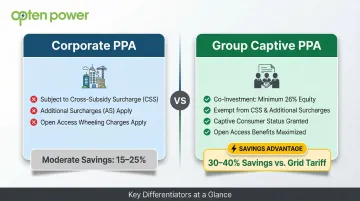

- Corporate PPAs — A business buys power from a third-party developer under open access, paying wheeling charges, cross-subsidy surcharges, and additional surcharges

- Group captive PPAs — Multiple companies co-invest (minimum 26% equity stake collectively) in a project, qualifying as captive consumers and avoiding most surcharges

Why Group Captive is Winning

Group captive structures have surged because they offer statutory exemptions from Cross-Subsidy Surcharges (CSS) and Additional Surcharges (AS) that make third-party PPAs increasingly unviable. In Q3 2024, landed costs of third-party solar open access increased in 12 of 15 major states, driven by rising surcharges.

The 2026 Electricity Amendment Rules addressed captive compliance directly.

Previously, captive users had to consume power in strict proportion to their shareholding — a rigid Unitary Qualifying Ratio (UQR) that created compliance risk. If one member failed to meet consumption requirements, the entire project could lose captive status.

The 2026 amendment now allows the 51% consumption requirement to be met collectively by the group, with individual consumption capped at 100% of proportionate entitlement. Any captive user holding 26% or more ownership is entirely exempt from proportionality caps.

Impact: This significantly de-risks group captive structures, making them easier to finance and more attractive to large C&I conglomerates.

Who's Leading Adoption

Heavy industries dominate group captive contracting:

- Steel and cement producers — Energy-intensive operations with 24/7 baseload demand

- Fertiliser conglomerates — Large multi-site operations that can pool consumption

- Manufacturing groups — Corporate families with multiple subsidiary companies

- Data centres — Rapidly expanding facilities seeking renewable compliance

For example, Ambuja Cements commissioned a 200 MW solar project in Gujarat in December 2024, unlocking an estimated 70% savings in power costs versus grid tariffs.

Group captive PPAs typically reduce energy costs by 30–40% versus grid tariffs by avoiding CSS and AS — a meaningful advantage for industries where power is a primary operating expense.

Hybrid and Storage-Linked PPAs Becoming the Go-To

Standard solar PPAs deliver power only during daylight hours — a critical limitation for industries operating 24/7. To address this, C&I buyers are increasingly turning to hybrid and storage-linked PPA structures.

Hybrid PPAs (Solar + Wind)

Hybrid projects combine solar's daytime peak generation with wind's nighttime generation, delivering a higher plant load factor (PLF) and closer-to-continuous renewable supply. These are particularly relevant for industries that cannot tolerate intermittency or rely heavily on expensive grid backup.

In 2025, SECI concluded a major auction for 2,000 MW of solar paired with 1,000 MW/4,000 MWh of energy storage, discovering a record-low tariff of ₹2.86/kWh. For C&I buyers, that tariff signals firm, round-the-clock renewable power is no longer a premium product.

Storage-Linked PPAs

Storage-linked PPAs include battery energy storage systems (BESS) that firm renewable generation, enabling true round-the-clock (RTC) power delivery. Buyers pay a slightly higher per-unit tariff but gain:

- Firmed power with minimal intermittency

- Reduced reliance on grid backup

- Better load matching for continuous-process industries

These benefits are drawing a specific class of high-consumption buyer into hybrid and storage-linked deals:

- Data centres — Nxtra by Airtel partnered with AMPIN Energy for 125.65 MW of solar-wind hybrid energy

- Hospitals — Requiring uninterrupted power with zero tolerance for outages

- Process industries — Cement, steel, and chemicals with continuous operations

Digital Edge signed an 83 MW solar PPA with Hexa Climate Solutions in 2026 to power its Navi Mumbai data centre, showing how data centre operators are locking in long-term renewable supply before capacity tightens further.

Structural Evolution: How PPA Contract Terms Are Changing in 2026

PPA contracts in 2026 carry shorter durations, dynamic pricing mechanisms, and new risk-sharing structures that didn't exist in standard agreements five years ago.

Shorter Contract Terms

Traditional PPAs ran 20–25 years to match project debt tenors and asset life. In 2026, there's a clear shift toward 12–15 year terms, particularly for corporate open access agreements where flexibility is valued.

The Ministry of Power proposed reducing standard PPA periods from 20 to 15 years, and Rajasthan's 1,000 MW BESS tender reduced contract periods to 12 years to align with battery lifecycle economics.

Pricing Mechanisms

Modern PPAs increasingly include:

- Floor and ceiling price mechanisms — Protecting both buyer and developer from extreme tariff movements

- Performance guarantee clauses — Minimum generation thresholds with compensation for shortfalls

- Escalation caps — Limiting annual tariff increases (typically 2–3%)

Volume Structures

Two models dominate:

- Pay-as-produced — Buyer pays only for actual generation; developer bears generation risk

- Fixed-volume — Buyer commits to minimum off-take with deviation penalties; suitable for predictable baseload demand

Risk-Sharing Provisions

Regulatory uncertainty in several states — variable open access charges, banking restrictions, DISCOM opposition — is driving buyers to include:

- Regulatory risk-sharing clauses — Allocating impact of future regulatory changes between parties

- Step-in rights — Allowing buyers to assume project operation if developer defaults

- Change-of-law provisions — Renegotiation triggers if material policy changes occur

Virtual PPAs (VPPAs)

In December 2025, CERC issued Guidelines for Virtual Power Purchase Agreements, classifying VPPAs as financial instruments for the first time. Under this structure, corporates procure Renewable Energy Certificates (RECs) for compliance without taking physical delivery of power. Settlement occurs on the difference between a pre-agreed strike price and the prevailing market exchange price.

Key Forces Shaping Solar PPA Trends in India in 2026

Regulatory and Policy Environment

India's renewable energy policy landscape in 2026 is characterized by central reform pushing PPA adoption forward and state-level resistance creating friction.

Open access policy reforms:

- CERC's updated grid connectivity norms streamline approval processes

- Standardized deviation settlement mechanisms under CERC DSM Regulations 2022 — renewable generators face graded charges for absolute errors beyond 10%

- State-level DISCOM resistance remains a barrier, with inconsistent open access charge applications

Renewable Consumption Obligation (RCO) mandates:

The Ministry of Power replaced RPO with stringent RCO requirements, mandating 29.91% renewable procurement in FY 2024-25, escalating to 43.33% by FY 2029-30. For large C&I consumers, signing long-term PPAs is the least-cost compliance route compared to buying volatile spot RECs.

Grid Tariff Inflation and Cost Pressures

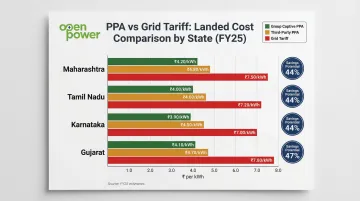

Industrial electricity tariffs have risen significantly over the past five years across major states, and the economic case for PPAs has never been clearer. With industrial grid tariffs in Maharashtra reaching approximately ₹8.68/kVAh, and similar increases in Tamil Nadu, Karnataka, and other states, the arbitrage opportunity for PPA contracting is widening.

Comparative landed costs (FY25 estimates):

| State | Third-Party PPA Landed Cost | Group Captive PPA Cost | Grid Tariff | Savings Potential |

|---|---|---|---|---|

| Maharashtra | ~₹8.00/kWh | ~₹4.50/kWh | ₹8.68/kWh | 30-40% |

| Tamil Nadu | ₹7.50-8.00/kWh | ~₹4.30/kWh | ₹8.00/kWh | 35-45% |

| Karnataka | ₹7.00-7.50/kWh | ~₹4.00/kWh | ₹7.50/kWh | 30-40% |

| Gujarat | ₹5.50-6.50/kWh | ~₹3.50/kWh | ₹6.50/kWh | 25-35% |

The table above shows how wide the gap between PPA and grid costs has grown — and solar generation costs are compressing it further. Utility-scale solar tariffs have fallen below ₹3.00/kWh in most auctions, widening the "savings spread" and making 2026 a strong window for C&I buyers to lock in long-term rates.

Market Dynamics and Developer Landscape

More developers competing for the same C&I load is pushing PPA pricing down and contract terms toward buyers. Key shifts shaping the market include:

- Bid spreads narrowing as developer pipelines scale up across solar, wind, and hybrid projects

- Digital procurement platforms opening competitive tendering to mid-sized C&I buyers who previously lacked access

- Standardized contract templates reducing negotiation timelines and legal friction

Platforms like Opten Power sit at the center of this shift, letting businesses compare tariffs, savings, and ROI across multiple developers in real time. Automated RFPs and pre-approved contract templates help buyers close deals 50% faster than traditional procurement routes.

How C&I Businesses Can Make Smarter PPA Decisions in 2026

Signing a PPA is a 12–25 year commitment that will shape your energy costs for the foreseeable future. Due diligence is critical.

Essential Pre-Signing Steps

1. Assess Load Profile and Baseload Requirements

- Document hourly/seasonal consumption patterns

- Identify minimum baseload vs. peak demand

- Determine renewable energy percentage target (RCO compliance)

2. Model Tariff Savings Against Total Landed Cost

- Calculate base PPA tariff + wheeling + CSS + AS + banking costs

- Compare against current and projected grid tariffs

- Model different scenarios (captive vs. third-party vs. group captive)

3. Validate Developer Financials and Project Readiness

- Review developer balance sheets and past performance

- Confirm project land, permits, and grid connectivity approvals

- Verify power evacuation infrastructure capacity

4. Scrutinize Regulatory Risk in Your State

- Review state electricity commission orders on open access charges

- Understand banking and carry-forward policies

- Assess DISCOM cooperation track record

Compare Multiple Developers

PPA tariffs, escalation clauses, deviation penalties, and contract terms vary significantly across developers. Comparing multiple offers is essential to securing the best commercial terms. Key factors to evaluate side-by-side include:

- Tariff structure and annual escalation rates

- Deviation penalty thresholds and settlement mechanisms

- Banking and carry-forward provisions

- Force majeure and exit clause terms

Platforms like Opten Power make this comparison practical at scale — connecting C&I buyers with verified power producers across 16 states, with instant IRR, payback, and regulatory analysis for each project. Automated RFP engines and pre-approved contracts let buyers close deals 50% faster from discovery to contract execution.

Ongoing Portfolio Management

Selecting the right deal is only half the work. Once a PPA is signed, active monitoring is what actually protects your contracted savings over the long term:

Track these metrics continuously:

- Actual generation vs. contracted/expected generation

- Deviation settlement charges and grid scheduling accuracy

- DISCOM billing accuracy and reconciliation

- Open access charge changes and regulatory updates

- Banking balance utilization and carry-forward limits

Opten Power's Portfolio Management Dashboard consolidates all of this into a single view: contracts, generation data, deviation charges, and regulatory updates across every asset in your portfolio. For C&I buyers managing multiple PPAs across states, that kind of consolidated oversight is what keeps contracted savings from quietly eroding.

Frequently Asked Questions

What is the 20% rule for solar panels?

The "20% rule" refers to the energy cost savings a buyer typically receives under a solar PPA versus grid tariffs. In India's C&I context, savings range from 20–40% depending on state tariffs, open access charges, and contracted PPA rates.

Is a solar PPA worth it for industrial businesses in India in 2026?

Yes — for energy-intensive industries with stable baseload demand, PPAs offer predictable, below-grid tariff power while avoiding large upfront capital expenditure. Savings potential is highest in high-tariff states like Maharashtra, Tamil Nadu, and Karnataka.

What is a group captive PPA and how does it benefit C&I buyers?

A group captive PPA involves multiple companies co-investing (minimum 26% collective equity stake) in a renewable project to qualify as captive consumers. This structure lowers open access surcharges, avoids cross-subsidy charges, and typically delivers 30–40% cost savings versus grid tariffs.

What is a typical PPA contract duration in India in 2026?

Traditional Indian PPA terms run 20–25 years, but 2026 trends show increasing adoption of 12–15 year terms for C&I buyers, particularly for corporate open access agreements where flexibility is valued.

Can a business exit a solar PPA before the contract term ends?

Early exit is typically contractually restricted and incurs buyout costs or penalty payments. Newer contracts increasingly include change-of-law provisions and exit windows, so negotiate exit clauses carefully upfront.

How does a solar PPA compare to outright solar ownership for a large industrial buyer?

Ownership delivers higher long-term savings and asset control, but requires significant upfront capital. PPAs offer zero capex, immediate savings, and fully maintained systems — making them the stronger fit for businesses prioritizing capital flexibility over maximum lifetime returns.