Introduction

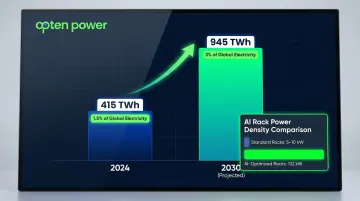

Data centers, once minor participants in energy markets, have emerged as the single largest buyers of clean electricity globally. In 2024, these facilities accounted for approximately 1.5% of global electricity consumption, totaling 415 terawatt-hours (TWh). AI workload expansion is now accelerating that demand faster than any prior year.

That consumption scale is translating directly into procurement dominance. Data centers led global corporate clean energy procurement in 2024, contracting more than 17 GW of deals — over a quarter of announced capacity globally. As these operators tighten their grip on clean energy markets, the implications for developers, regulators, and buyers across Asia are hard to ignore.

This article covers:

- Why data centers are buying clean power so aggressively in 2026

- The procurement mechanisms operators rely on (PPAs, RECs, direct investment)

- Risks emerging as demand concentration reshapes renewable energy markets

- What India's regulatory environment means for data center operators here

Key Takeaways

- AI workloads and cloud expansion are pushing data center electricity demand to record highs, making the sector one of the top clean energy buyers in 2026

- Amazon, Meta, Google, and Microsoft alone accounted for 49% of 55.9 GW in global corporate clean PPAs signed in 2025

- PPAs remain the dominant procurement route, but co-location with renewable plants and 24/7 carbon-free energy sourcing are gaining traction

- Concentrated buying by data centers risks crowding out other corporate offtakers — often without adding net new renewable capacity to the grid

- Indian data centers navigate a fragmented state-by-state regulatory landscape; Opten Power's real-time Discom intelligence and 4+ GW marketplace simplify procurement across 16 states

Why Data Centers Have Become the World's Largest Clean Energy Buyers

The AI-Driven Demand Explosion

Training large language models and running inference workloads consume orders of magnitude more power than standard cloud computing. Traditional data center racks operate at 5-10 kW per rack, while AI-optimized facilities using systems like Nvidia's GB200 NVL72 architecture are rated at up to 132 kW per rack — more than 13 times the power density. Electricity consumption in accelerated servers is projected to grow by 30% annually, compared to just 9% per year for conventional servers.

That gap in power density is reshaping how energy markets work. The IEA projects global data center electricity consumption will more than double to reach around 945 TWh by 2030, representing just under 3% of total global electricity consumption — up from 1.5% today.

The 24/7 Uptime Constraint

Unlike manufacturing facilities that can shift loads or commercial buildings that close at night, data centers require continuous, uninterrupted power. This makes reliable clean energy sourcing far harder — and more urgent — than for virtually any other industrial buyer.

A single hour of downtime can cost millions in lost revenue and damaged customer trust. Operators must prioritize reliability and sustainability together, not as competing priorities.

The Net-Zero Commitment Driver

Voluntary sustainability goals — not direct regulation in most markets — are the primary force pushing procurement today. The largest operators have set binding public targets:

- Google: 24/7 carbon-free energy on every grid by 2030

- Microsoft: 100% zero-carbon energy matched around the clock by 2030

These commitments — not government mandates — are what's driving most of the procurement surge. Germany, China, and Ireland are notable exceptions where regulators have imposed direct requirements, but they remain outliers globally.

The Scale Effect

As individual data centers grow to gigawatt-scale campuses, a single facility can consume as much electricity as a mid-sized city. This forces operators to engage in wholesale renewable energy markets rather than simple utility tariffs. The scale creates both opportunity — allowing operators to command favorable long-term pricing — and responsibility, as their procurement decisions increasingly shape regional and national energy markets.

How Data Centers Are Securing Clean Energy: Procurement Mechanisms in 2026

Power Purchase Agreements (PPAs)

Long-term PPAs have become the dominant procurement instrument for data center operators. These contracts lock in price and volume of clean electricity, typically for 10-25 years, providing both cost certainty and sustainability credentials.

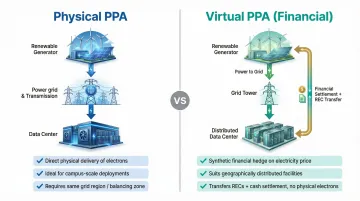

Physical PPAs involve direct delivery of electricity from a renewable generator to the data center (or into the same grid region), while virtual PPAs (also called financial PPAs) function as synthetic hedges: the buyer receives renewable energy credits and a financial settlement based on the difference between the contracted price and market rates, without physical delivery.

Internet giants accounted for 43% of clean PPAs signed in 2024, demonstrating how thoroughly hyperscalers have come to dominate this market. Virtual PPAs suit operators with distributed facilities across multiple grids, while physical PPAs work best for large campus deployments with direct grid access.

Co-location with Renewable Plants

An emerging model involves building or co-locating data centers directly adjacent to large solar or wind farms, bypassing grid constraints and accessing cheaper power. This approach eliminates transmission costs and reduces grid dependency, but intermittency remains the central barrier to wider adoption.

Solar and wind generation fluctuates with weather and time of day, creating periods when the co-located renewable plant cannot meet the data center's constant demand. Operators are exploring hybrid projects combining solar, wind, and battery storage as solutions, but storage costs and technical complexity remain real barriers.

Round-the-Clock Carbon-Free Energy (24/7 CFE)

That intermittency problem is precisely what 24/7 CFE targets. A growing set of hyperscalers now commit to hourly matching of electricity consumption with carbon-free generation — not just annual matching. Google maintained a global average of 64% CFE across data centers in 2023, with 10 grid regions achieving at least 90% CFE.

Hourly matching requires a sophisticated portfolio of dispatchable and storage resources, including:

- Dispatchable renewables: hydro and geothermal

- Battery and long-duration storage

- Nuclear power (increasingly included in CFE frameworks)

This standard is far more rigorous than annual matching, which lets companies claim 100% renewable power by offsetting nighttime fossil fuel use with extra daytime solar purchases.

Renewable Energy Certificates (RECs) and Their Limitations

RECs and similar instruments — India's RECs, Europe's Renewable Energy Guarantees of Origin — remain the easiest entry point for data centers beginning their clean energy journey. A REC represents proof that one megawatt-hour of electricity was generated from a renewable source and fed into the grid.

RECs are increasingly seen as insufficient for credible decarbonization claims. The core problem is additionality: purchasing RECs from already-operational projects doesn't increase renewable capacity on the grid. It shifts paper claims around without financing new clean energy infrastructure.

Opten Power: Simplifying India's Fragmented Procurement Landscape

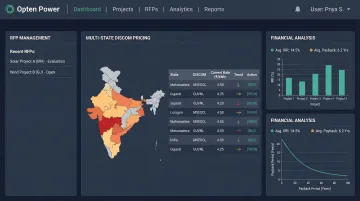

For data center operators in India, navigating bilateral negotiations state by state creates significant procurement friction. Opten Power's unified marketplace addresses this by enabling discovery, comparison, and transaction across 4+ GW of renewable capacity — solar, wind, and hybrid — spanning 16 states.

The platform provides automated RFP creation and management, real-time DISCOM pricing intelligence covering state-specific charges, and instant IRR and payback analysis. This allows procurement teams to compare developers, model financial outcomes, and close deals up to 50% faster than traditional bilateral processes — without managing varying state regulations independently.

Renewable Energy Sources Powering Today's Data Centers

Solar and Wind (and Hybrid)

Solar and wind are the cost leaders for most data center operators, offering the lowest levelized cost of energy and wide geographic availability. However, their intermittency creates challenges for always-on data center loads.

Hybrid solar-wind projects with battery storage address this directly. The combination works because:

- Solar peaks during daytime hours; wind typically generates more at night

- Battery storage fills the gaps between generation windows

- The blended profile reduces curtailment and improves capacity utilization

For data centers requiring 24/7 reliability, hybrid projects deliver a more consistent power profile than single-source installations.

Nuclear as a Reliability Play

Solar and wind solve the cost problem, but not the round-the-clock reliability problem. That gap is driving renewed interest in nuclear — specifically as a dispatchable, carbon-free baseload source that runs regardless of weather.

Growing interest from US hyperscalers in small modular reactors (SMRs) and existing nuclear capacity reflects the search for always-on clean power to sit alongside variable renewables.

Major nuclear agreements include:

- Microsoft's 20-year PPA for 835 MW from the Three Mile Island Unit 1 restart, expected online in 2028

- Meta's 20-year PPA for 1,121 MW from the Clinton Clean Energy Center in Illinois, starting in 2027

- Amazon's PPA for 1,920 MW from the Susquehanna nuclear plant through 2042

These deals are largely a US and European story for now. In India, nuclear power remains under government control — private sector PPAs are not permitted under current regulations, which means Indian data centre operators cannot replicate this procurement model directly.

Emerging Options: Green Hydrogen and Long-Duration Storage

Green hydrogen and long-duration energy storage are being explored for multi-day backup and peak demand smoothing. Neither is commercially viable at scale yet — both require significant cost reductions and infrastructure build-out before they can replace conventional backup generation.

For Indian data centres and C&I buyers today, solar-wind hybrid with battery storage remains the most accessible path to high-reliability renewable power while these technologies mature.

The Hidden Risks: When Green Demand Outpaces Green Supply

Displacement Risk

Data center operators captured approximately 43% of available clean energy contracts in 2024, raising concerns that they may be crowding out other industrial and commercial offtakers who also have decarbonization targets. If hyperscalers are simply claiming existing renewable capacity without financing new projects, they displace other buyers without creating net new renewable generation.

This creates a zero-sum dynamic in which data centers meet their sustainability commitments while other sectors struggle to access clean energy, potentially slowing economy-wide decarbonization.

Grid Strain in Data Center Hotspots

Concentrated data center demand in regional hubs creates localized grid congestion, forcing costly infrastructure upgrades. Ireland provides a clear example: data centers consumed 22% of the country's power in 2024, with projections to reach 31% by 2034.

In response, Ireland's Commission for Regulation of Utilities now requires data centers to bring onsite dispatchable generation and/or storage equivalent to or greater than their demand. This regulatory shift forces operators to contribute new capacity rather than simply drawing from the existing grid.

Additionality and Greenwashing Risk

Procuring RECs or PPAs from already-operational renewable projects doesn't technically increase the renewable capacity available on the grid. Additionality — the principle that clean energy procurement should finance new capacity, not just claim existing generation — is increasingly demanded by investors, regulators, and enterprise customers.

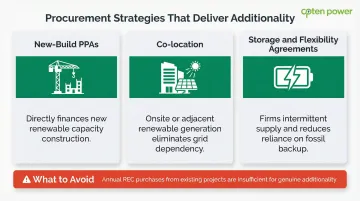

Annual REC purchases from existing projects risk greenwashing without delivering real emissions reductions. Procurement strategies that genuinely deliver additionality include:

- New-build PPAs that directly finance construction of incremental renewable capacity

- Co-location of renewable generation onsite or adjacent to the data center facility

- Storage and flexibility agreements that firm up intermittent supply and reduce grid dependence

What the Clean Energy Surge Means for Data Centers in India

India's Data Center Growth Trajectory

India is one of the fastest-growing data center markets in Asia, driven by digitalization, AI adoption, cloud migration, and supportive government policy. India's operational data center capacity reached 1.3 GW to 1.53 GW in 2025, with an additional 2.9 GW of supply expected by 2030.

Nearly 90% of existing capacity is concentrated in Mumbai, Chennai, Delhi-NCR, and Bengaluru, creating regional grid pressure similar to Ireland's experience.

India's Clean Energy Procurement Landscape

Data centers in India can access renewable energy through open access (state and inter-state), group captive structures, and bilateral PPAs. However, each route comes with different DISCOM charges, wheeling and banking regulations, and state-level approvals.

State-level charges vary significantly and stack up fast:

| Charge Type | State | Rate |

|---|---|---|

| Cross-subsidy surcharge (CSS) | Maharashtra (HT Industry) | ₹1.79/kWh |

| Cross-subsidy surcharge (CSS) | Karnataka | ₹1.12/kWh |

| Additional surcharge (AS) | Maharashtra | ₹1.39/kWh |

| Wheeling charges | Maharashtra | ₹0.60/kVAh |

| Banking charge (solar, daily settlement) | Gujarat | ₹1.5/kWh |

| Banking charge (wind/hybrid) | Gujarat | No charge |

Without accurate, state-by-state cost visibility, operators risk underestimating landed energy prices by 20–30% — which can materially distort PPA economics at scale.

The Renewable Energy Opportunity

India's 500 GW renewable target by 2030 and the large pipeline of solar, wind, and hybrid projects give data centers a clear path for data centers to lock in long-term, low-cost clean power. India's total installed power generation capacity reached 520.5 GW as of January 31, 2026, with renewable energy sources accounting for 263.18 GW.

Renewable tariffs in India are increasingly competitive with grid power for large consumers, particularly when structured through well-negotiated PPAs that lock in prices for 15-25 years.

Opten Power's Role in India's Data Center Procurement Race

For data center operators navigating India's fragmented state-by-state energy market, Opten Power's unified marketplace — covering 16 states with 4+ GW of available renewable capacity — offers clear advantages:

- Standardized, updated DISCOM landing prices across all states so operators can compare costs accurately and never overpay

- Modular RFP templates and structured bid collection from multiple developers — cutting procurement timelines by up to 50%

- Instant IRR, payback period, and regulatory impact assessments for data-driven decisions at speed

- A single dashboard to monitor all renewable energy investments, active contracts, and assets

For data centers requiring reliable, round-the-clock power, Opten Power's hybrid energy offerings — combining solar's daytime generation with wind's nighttime output — deliver grid stability and optimized tariffs critical for 24/7 operations.

Frequently Asked Questions

Why are data centers buying so much renewable energy in 2026?

A combination of voluntary net-zero commitments, rapidly growing AI-driven electricity demand, and emerging government regulations is pushing data center operators to lock in large-scale clean energy contracts. PPAs are the dominant instrument, providing both cost certainty and sustainability credentials.

What is a Power Purchase Agreement (PPA) and how do data centers use it?

A PPA is a long-term contract between a data center and a renewable energy generator, fixing the price and volume of clean electricity — typically for 10–25 years. Data centers use them to stabilize energy costs while meeting sustainability commitments.

What renewable energy sources are best suited for data centers?

Solar and wind are the most cost-effective options, but their intermittency means hybrid projects with battery storage or supplementary hydro are preferred for data centers that need 24/7 reliability. Dispatchable, carbon-free baseload sources are gaining traction globally for this reason.

Do data centers buying clean energy actually help the environment?

The answer hinges on additionality — whether procurement finances new renewable capacity (net positive) or simply claims existing generation (neutral to grid). 24/7 CFE commitments and new-build PPA structures are the more credible approaches that drive real emissions reductions.

How can data centers in India procure renewable energy?

Indian data centers can access renewable energy through open access, group captive structures, or bilateral PPAs. Navigating state-by-state DISCOM regulations is complex — Opten Power aggregates capacity and real-time pricing across 16 states, simplifying procurement for C&I buyers.

What risks should data centers consider when buying clean energy?

Key risks include grid strain in data center hubs, potential displacement of other clean energy buyers, contract tenor risks, and the regulatory complexity of ensuring procurement genuinely reduces carbon emissions rather than just offsetting on paper. Structures that require hourly matching and finance new-build capacity offer the strongest protection against greenwashing exposure.