Introduction

Data centers are among the fastest-growing electricity consumers globally. The International Energy Agency projects that data center electricity consumption will more than double to around 945 TWh by 2030—growing at roughly 15% annually, over four times faster than total electricity demand growth. In India, the trajectory is equally dramatic: installed capacity has nearly tripled from approximately 520 MW in 2020 to 1.5 GW by mid-2025, with projections reaching 2.9–6.5 GW by 2030 as AI and cloud computing drive power demand sharply higher.

Clean energy procurement is now a business imperative for data center operators. Rising grid tariffs, tenant ESG demands tied to scope 3 emissions accounting, and tightening Renewable Purchase Obligations (RPOs) are forcing operators to secure structured renewable supply.

This guide breaks down what clean energy procurement means for data centers, how the process works, the main mechanisms available, and what separates successful deals from costly missteps.

Key Takeaways

- Clean energy procurement enables data centers to source electricity from renewable generators through structured PPAs, certificates, or on-site installations

- Drivers include volatile grid tariffs, tenant scope 3 reporting requirements, India's 43.33% RPO target by 2029-30, and long-term cost hedging

- Primary mechanisms: Corporate PPAs via open access, Renewable Energy Certificates, captive/group captive plants, and utility green tariffs

- State-level open access rules, DISCOM policies, and wheeling charges vary widely, affecting landed costs and procurement feasibility

- 24x7 load requirements demand hybrid projects (solar + wind + storage) or banking arrangements to ensure continuous supply

What Is Clean Energy Procurement for Data Centers?

Clean energy procurement is the formal process by which a data center secures electricity generated from renewable sources—solar, wind, or hybrid—through structured supply agreements, financial instruments, or owned assets, rather than relying entirely on the standard utility grid mix.

The core objectives are:

- Reduce carbon intensity of electricity consumption across operations

- Lock in predictable pricing through long-term supply agreements, shielding against grid tariff volatility

- Enable verifiable sustainability claims demanded by tenants, investors, and regulators

For hyperscale tenants and co-location customers tracking Scope 3 Category 13 emissions (downstream leased assets under the GHG Protocol), demonstrating clean supply is no longer optional—it's contractual.

Passive grid-supplied renewable energy—where a utility happens to carry a green mix—differs fundamentally from active procurement. When a data center directly structures its own clean energy supply, it gains cost control, ESG credibility, and temporal matching of generation to consumption. In India, this also intersects with Renewable Purchase Obligation (RPO) compliance under the Ministry of Power framework, adding a regulatory layer that grid-passive approaches cannot satisfy. Globally, frameworks like 24/7 Carbon-Free Energy (CFE) standards—increasingly required by hyperscalers like Google and Microsoft—make active procurement the only credible path forward.

Why Data Centers Are Investing in Clean Energy Procurement

Scale of Electricity Consumption

Data centers operate continuously at megawatt-scale loads, currently accounting for approximately 1.5% of global electricity consumption. AI workloads are compounding this rapidly. Average rack power densities have climbed from 1-3 kW in the early 2000s to around 8 kW today, with high-density racks drawing 15-29 kW.

Specialized AI infrastructure like NVIDIA DGX H100 systems consume 10.2 kW per system alone. At that scale, energy cost and carbon exposure become top-tier operational risks.

Tenant and Investor ESG Requirements

That energy risk feeds directly into tenant pressure. Hyperscalers, cloud companies, and enterprise co-location tenants now mandate clean energy commitments from their data center providers. Under GHG Protocol, emissions from leased assets fall under scope 3 category 13 — meaning a data center operator's carbon footprint flows into the tenant's reported figures.

Major buyer requirements include:

- Microsoft: 100% carbon-free electricity from suppliers by 2030

- Google: 24/7 carbon-free energy matching by 2030, with 100% clean energy across supplier operations

Operators who cannot demonstrate a verified clean supply chain risk losing tenancy to competitors who can.

Regulatory Compliance Pressure

In India, Renewable Purchase Obligations require large consumers to source a defined percentage of electricity from renewables. The Ministry of Power has mandated an RPO trajectory reaching 43.33% by 2029-30, applicable to designated consumers including open access and captive users. The threshold has been lowered to 100 kW under the Green Energy Open Access Rules 2022.

Non-compliance attracts penalties up to ₹10 lakh per failure under Section 26(3) of the Energy Conservation Act.

Cost Economics of Clean Energy

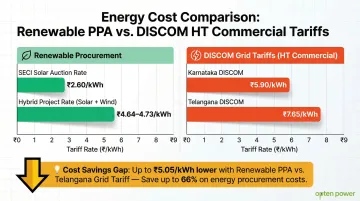

Solar and wind power purchase rates have declined sharply. India achieved the second most competitive solar LCOE globally in 2024 at USD 0.038/kWh — a 91% decrease since 2010. By comparison, DISCOM HT commercial tariffs range considerably higher:

- SECI solar auctions: tariffs as low as ₹2.60/kWh

- Hybrid projects: ₹4.64–4.73/kWh

- Karnataka DISCOM HT tariff: ₹5.90/kWh

- Telangana DISCOM HT tariff: ₹7.65/kWh

The gap between renewable procurement rates and grid tariffs illustrates the cost case for active procurement — when structured correctly.

Energy Price Certainty and Risk Hedging

Long-term PPAs (typically 10-25 years) lock in power costs at a fixed or modestly escalating rate, protecting data centers from grid tariff hikes and fuel cost pass-throughs endemic to conventional utility supply. This price certainty is critical for data centers with thin operating margins and long-term tenant contracts requiring predictable cost structures.

How the Clean Energy Procurement Process Works

The procurement lifecycle follows a structured path: energy needs assessment → market discovery and developer evaluation → contract structuring → regulatory approvals → commissioning and ongoing portfolio management. Each stage has regulatory, technical, and commercial dependencies that must be managed in parallel.

Step 1: Energy Audit and Requirement Assessment

The process begins with a rigorous internal assessment. Before approaching the market, the data center must establish four foundational parameters:

- Total contracted load (in MW) across current and projected capacity

- Hourly and seasonal consumption profile — 24x7 baseload operations differ fundamentally from day-peaking commercial loads

- Delivery voltage level required at the point of interconnection

- Clean energy proportion — how much load will be served through renewable sources versus grid backup

This assessment directly informs technology selection (solar, wind, or hybrid) and the appropriate contract structure.

Step 2: Market Discovery and Developer Comparison

Data centers issue Requests for Proposals (RFPs) to renewable developers, evaluating projects across tariff, technology type, project location, and regulatory status. Platforms like Opten Power accelerate this process by connecting buyers to 4+ GW of pre-vetted renewable projects across solar, wind, and hybrid technologies in 16 states. Each project comes with real-time DISCOM landing prices, instant IRR and payback analysis, and regulatory impact assessment. This reduces what traditionally takes months to days, accelerating deal closure by up to 50% through automated RFP management and structured bid collection.

Step 3: Contract Structuring and Regulatory Approvals

Two parallel workstreams must be completed before a project moves to commissioning: commercial contract negotiation and regulatory clearance.

Key contractual elements to agree on:

- Tariff structure (fixed, escalating, or indexed to market)

- Contract tenor and renewal terms

- Scheduling and deviation settlement obligations

- Force majeure and curtailment protections

- Termination provisions and exit clauses

Regulatory approval pathway:

- Open access application with the relevant state commission

- Short-term or long-term transmission access allocation

- DISCOM connectivity agreement execution

- Power banking or scheduling arrangements

Approval timelines typically span 6–18 months and must be built into project planning from day one. Pre-approved contract templates can reduce negotiation friction and accelerate closure considerably.

Clean Energy Procurement Mechanisms Data Centers Use

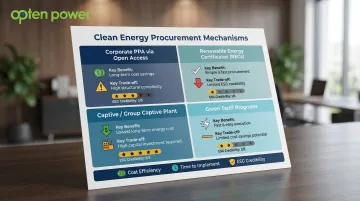

Corporate Power Purchase Agreements (PPAs) via Open Access

A data center contracts directly with a renewable energy developer to receive power delivered through the grid under open access regulations—governed by the Electricity Act 2003 and the Green Energy Open Access Rules 2022. This is the most common long-term procurement route for large load centers. When structured well, it can reduce effective energy costs by up to 40% compared to DISCOM commercial tariffs.

In 2024, India added 6.9 GW of solar open access capacity—a 77% increase over 2023—bringing cumulative installed capacity to 20.2 GW. State-level implementation varies significantly: Karnataka issued new Open Access Regulations in 2025, while Maharashtra operates under MERC Distribution Open Access Regulations with distinct charge structures. Key variables to negotiate carefully include:

- Contract tenor — typically 15–25 years, affecting bankability and pricing

- Banking rights — determines how surplus energy is stored and drawn down

- Wheeling charges — vary by state and can significantly affect landed cost

Renewable Energy Certificates (RECs)

RECs allow data centers to claim renewable attributes for each MWh generated by a registered renewable plant, without physically receiving that power. Under CERC REC Regulations 2022, each certificate represents one MWh of renewable electricity injected into the grid. Obligated entities purchase RECs through power exchanges or traders to meet RPO compliance.

Key limitation: RECs do not guarantee temporal or geographic matching of supply to consumption. Because RECs are reconciled annually and detached from generation time and location, they fall short of advanced clean energy standards like 24/7 CFE frameworks increasingly demanded by hyperscale tenants. The Science Based Targets initiative notes that annual matching with unbundled RECs lacks accuracy and can overstate emissions reductions, failing to incentivize dispatchable low-carbon technologies needed for true grid decarbonization.

Captive and Group Captive Renewable Plants

Data centers can fully own a renewable project or co-own one through a group captive structure, which requires a minimum 26% equity stake per Electricity Rules 2005. Recent 2026 amendments clarified that for group captive structures (Association of Persons), the 51% consumption requirement can be met collectively by users—making it easier to onboard new consumers into the group.

Primary advantage: Exemption from Cross-Subsidy Surcharge (CSS) and Additional Surcharge (AS), which can add ₹1.79–1.87/kWh in states like Maharashtra and Karnataka. This exemption typically achieves the lowest per-unit energy cost. Group captive models can deliver per-unit savings of ₹3–5/kWh with strong IRRs while requiring minimal equity. Trade-offs to weigh include:

- Higher upfront capital for fully owned projects

- Land acquisition and grid connectivity requirements

- Balance-sheet implications of asset ownership

- Longer development timelines versus procured power

Green Tariff Programs and Utility Partnerships

State utilities offer structured green tariff options that let large consumers pay a premium to be allocated renewable generation from the utility's portfolio. Direct utility co-investment or co-serve models take this further—enabling data centers to partner on infrastructure in exchange for preferential energy access and cost-sharing.

Compared to PPAs and captive structures, green tariff programs offer:

- Simpler execution — no developer procurement or asset management required

- Lower cost optimization — premium pricing limits savings versus direct PPAs

- Regulatory predictability — terms set by the utility, reducing negotiation complexity

For data centers prioritizing speed of procurement over cost minimization, green tariffs offer a workable entry point. Those with higher load requirements and longer planning horizons typically find PPAs or captive models deliver better long-term economics.

Key Factors, Misconceptions, and Common Pitfalls

Regulatory and Landed Cost Complexity

Open access charges—including wheeling and transmission charges, cross-subsidy surcharges, and additional surcharges—vary materially across Indian states and can erode the cost advantage of a PPA if not modeled accurately at the outset.

Illustrative example: Consider a base solar PPA tariff of ₹2.60/kWh applied in two states:

Maharashtra (MSEDCL): CSS of ₹1.79/kWh + AS of ₹1.36/kVAh pushes the landed cost near ₹5.75/kWh (before wheeling, transmission, and losses)—barely competitive with the DISCOM tariff.

Karnataka (BESCOM): CSS of ₹1.87/kWh with no AS currently levied results in a significantly lower landed cost, demonstrating why location strategy and state-specific regulatory modeling are critical for data center procurement decisions.

Load Profile and Intermittency Mismatch

Data centers require constant, round-the-clock power—servers operate 24/7 in both active and passive modes, creating near-constant baseload consumption. Solar generation is daytime-only and wind is variable, creating a fundamental mismatch.

Solution: Hybrid projects combining solar, wind, and Battery Energy Storage Systems (BESS) have become essential for meeting continuous load requirements. Real-world examples show this model gaining traction:

- ReNew's 3.3 GW RTC Hybrid project integrates wind, solar, and 100 MWh BESS across multiple states, delivering 24/7 clean energy under a 25-year PPA

- Princeton Digital Group partnered with Tata Power Renewables to implement hourly carbon-free electricity matching for its Mumbai data center

Procuring solar-only PPAs without addressing the nighttime and monsoon gap is a common planning error—one that leaves data centers dependent on grid backup.

Misconception—RECs Equal Genuine Clean Energy

Many data center operators assume purchasing RECs fully satisfies their clean energy and sustainability claims. Leading frameworks—including Science-Based Targets initiative methodology and 24/7 CFE standards—require temporal and geographic matching between clean generation and consumption, not merely annual volume offsets.

Data centers relying solely on RECs face growing credibility challenges with tenants and investors who demand hourly-matched supply that actually displaces fossil generation at the moment of consumption.

Underestimating Procurement Complexity and Timelines

Operators frequently miscalculate the time required for open access filings, DISCOM approvals, grid connectivity agreements, and regulatory hearings. The typical end-to-end timeline spans 6–18 months from initial RFP issuance to commercial power delivery, depending on regulatory approval complexity, filing queues, project construction stage, and PPA negotiation depth.

Automated RFP management tools and pre-approved contract templates—such as those available on Opten Power—can cut deal closure timelines by up to 50%, compressing the discovery, evaluation, and contract finalization stages into a single managed workflow.

Frequently Asked Questions

How do data centers typically approach clean energy procurement?

Data centers typically pursue clean energy through three parallel tracks: renewable energy credits (RECs) procured by tenants, low-carbon backup fuels such as hydrogenated vegetable oil (HVO) that can cut generator emissions by roughly 85%, and energy-efficient facility design targeting a PUE of 1.25 or lower. Tenant emissions (scope 3, category 13) are generally treated as a shared responsibility between the facility operator and its customers.

What is the difference between a PPA and a REC for data center energy procurement?

A Corporate PPA is a long-term contract for the physical or financial delivery of renewable electricity (typically under open access), while a REC is a tradeable certificate representing the environmental attribute of 1 MWh of renewable generation that can be purchased independently of physical power supply. PPAs offer greater cost certainty and ESG credibility than RECs alone.

How long does a clean energy procurement deal typically take for a data center?

Most deals take 6 to 18 months from initial RFP to commercial power delivery. The range depends on regulatory approval complexity, open access filing queues, the project's construction stage, and how involved the PPA negotiation becomes.

What factors determine whether open access PPAs or captive solar are the better choice for a data center?

The right model depends on several factors:

- Load size — captive solar becomes viable above a certain MW threshold

- Capital availability — open access PPAs suit off-balance-sheet procurement preferences

- State-level open access charges — particularly Cross-Subsidy Surcharge (CSS) and Additional Surcharge (AS)

- Timeline — open access PPAs can be structured faster than commissioning a captive asset

What is an acceptable PUE target for data centers pursuing green energy certification or green financing?

A design-average PUE of 1.4 or lower is the commonly cited eligibility threshold under green finance frameworks, including ICMA Green Bond Principles-aligned instruments and SEBI's green bond disclosure norms in India. Facilities targeting the most competitive financing terms typically aim for 1.2–1.4, which also strengthens broader sustainability credentials.