Introduction

Indian commercial and industrial energy buyers face a stark reality in 2026: electricity costs routinely consume 15–30% of operating expenses, compounded by a labyrinth of state-wise tariff complexity, frequently amended DISCOM policies, and mounting pressure from renewable energy mandates. With cross-subsidy surcharges and additional surcharges averaging ₹2.25 per kWh across states—and frequent amendments reshaping the economics of every procurement decision—acting without real-time market intelligence carries a direct cost that shows up on every utility bill.

This blog unpacks what energy market intelligence means for C&I buyers in 2026: the four pillars that separate cost-optimized procurement from expensive guesswork, and how real-time DISCOM data and AI-powered platforms are compressing the journey from insight to signed PPA from months to weeks.

If your procurement team still relies on outdated tariff schedules or broker-sourced capacity lists, you're likely overpaying—and losing ground in India's most competitive renewable energy market to date.

Key Takeaways

- Energy market intelligence in 2026 means instant access to tariff benchmarking, regulatory monitoring, IRR analysis, and demand forecasting in one unified platform

- India's renewable market spans 16+ states with inconsistent DISCOM pricing and open access rules — state-by-state intelligence is essential for effective procurement

- AI-powered platforms let C&I buyers compare PPA offers, run financial models, and execute automated RFPs in hours — not weeks

- Businesses leveraging real-time energy market intelligence can reduce costs up to 40% through better-timed procurement and optimized corporate PPAs

Why 2026 Is a Critical Year for Energy Market Intelligence in India

India's energy market is undergoing a structural transformation that makes 2026 a decisive inflection point for C&I buyers. The country crossed 250 GW of non-fossil power capacity in 2025, with renewable additions accelerating: 44.51 GW of renewable capacity was added between January and November 2025 alone, and solar capacity reached 132.85 GW by year-end. As of April 2026, cumulative solar power stands at 150.26 GW, with wind at 56.09 GW.

This capacity surge is driving unprecedented competition among developers and creating opportunities for C&I buyers—but only for those equipped to navigate the complexity. The C&I open access market grew 90.4% between FY2023 and FY2024, while solar open access capacity additions jumped from 6.9 GW in 2024 to 7.8 GW in 2025, pushing cumulative solar open access capacity past 30 GW.

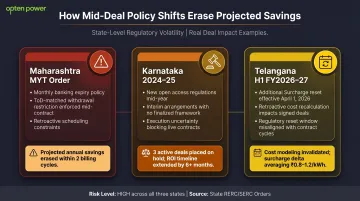

The cost of information gaps is measurable and steep. Without real-time tariff data, C&I buyers routinely overpay on grid power or sign PPAs at non-competitive rates. Maharashtra's revised banking and time-of-day (ToD) rules in 2026, for example, can reduce projected savings by at least 10% for solar open access consumers who didn't factor these restrictions into their financial models. Karnataka's mid-year revision of open access additional surcharges from higher levels to ₹0.40 per kWh reshaped deal economics overnight for third-party open access buyers.

India's regulatory complexity differs from centralized global markets in one critical way: every state operates independently. Each DISCOM answers to its own State Electricity Regulatory Commission (SERC), with distinct open access charges covering wheeling, transmission, cross-subsidy surcharges, banking fees, and standby charges.

Twenty-seven states had notified Green Energy Open Access (GEOA) regulations by April 2025—but state-level deviations remain significant:

- Gujarat charges ₹1.50 per kWh for solar banking through June 2026

- Tamil Nadu applies an 8% in-kind banking charge with strict ToD drawal rules

- Haryana restricts banked power withdrawal during peak load hours

A single national intelligence approach is insufficient. Buyers operating across multiple states need real-time, standardized data for every location—or they're negotiating blind.

The Four Pillars of Energy Market Intelligence for C&I Buyers

Tariff & Landing Price Intelligence

"Landing price" is the total delivered cost of renewable power, including base tariff plus all state levies: transmission charges, wheeling fees, cross-subsidy surcharges, additional surcharges, and banking costs. It's the only metric that enables valid apples-to-apples comparisons between grid power and renewable alternatives—and it varies dramatically across DISCOMs and states.

Tamil Nadu's FY2026 tariff revisions increased transmission tariffs for C&I buyers by 4% and raised cross-subsidy surcharges by 3.2–3.6%, while temporarily reducing additional surcharges to ₹0.10 per kWh for April–September 2025. Karnataka's DISCOM revisions in FY2025–26 replaced previously uniform rate structures with new tiered pricing. Without standardized, continuously updated landing price data across all states, procurement teams cannot identify which geographies deliver the highest ROI or which PPA offers are genuinely competitive.

Opten Power's Real-Time DISCOM Intelligence solves this problem by delivering standardized, updated landing prices across all 16 states where it operates, enabling instant comparison of tariffs, savings, and ROI across developers and geographies. This replaces weeks of manual SERC filing research with actionable data at the point of decision.

Regulatory & Policy Monitoring

Policy shifts—open access approvals, banking regulation amendments, REC pricing changes, RPO obligation updates, and DISCOM tariff orders—can materially alter renewable deal economics mid-procurement. Tracking these changes is a procurement risk management discipline, not a compliance formality.

Recent state-level changes illustrate the stakes:

- Maharashtra MYT order: Introduced monthly expiry of unused banked energy and restricted withdrawal to matching ToD slots, fundamentally changing solar open access economics for buyers who hadn't modeled these constraints

- Karnataka (2024–25): Courts required new open access regulations and interim arrangements, creating execution uncertainty for deals already in progress

- Telangana H1 FY2026–27: Additional Surcharge determination effective April 1, 2026 reset cost assumptions for every open access buyer in the state

Miss one of these changes mid-deal, and projected savings evaporate.

Developer & Capacity Intelligence

Knowing which developers have available, bankable capacity in your geography, what technology types are on offer (solar, wind, hybrid), and each developer's track record is critical to execution risk management. The post-GEOA market has attracted both established players like ReNew and Avaada and newer entrants like Kalpa Power and Ampyr Energy.

Solar open access capacity additions of 7.8 GW in 2025 brought cumulative solar OA capacity past 30 GW, indicating a deep and growing developer pipeline. But not all capacity is equal: greenfield projects carry construction risk, operating assets offer immediate generation but higher pricing, and developer credibility directly affects financing availability and long-term PPA performance.

Opten Power's marketplace provides access to 4+ GW of pre-vetted renewable projects across solar, wind, and hybrid technologies, with verified developer credentials, technology specifications, and capacity availability across 16 states. This developer intelligence is integrated into the platform's instant financial analysis, so buyers can evaluate both deal economics and execution risk simultaneously.

Financial Scenario Modeling

IRR, payback period, and sensitivity analysis—tariff escalation assumptions, generation variability, financing costs—are the essential inputs for procurement decisions. Buyers who lack these models at the RFP stage cannot effectively evaluate competing offers, leaving them vulnerable to overly optimistic developer projections.

A buyer comparing two 10 MW solar PPAs at ₹4.50 and ₹4.60 per unit needs to model far more than the headline tariff gap. The real comparison requires:

- State-specific open access charges

- Banking loss assumptions

- ToD arbitrage opportunities

- Escalation clauses across a 25-year contract term

Without instant scenario modeling, procurement teams either delay decisions to build these models manually or sign deals based on incomplete analysis.

Relying on consultants for financial models, brokers for developer lists, and manual SERC research for tariff data fragments all four pillars across different sources and timelines. A unified intelligence platform that integrates all four at the point of procurement eliminates that fragmentation—and the delays and risk that come with it.

Real-Time DISCOM Intelligence: The Missing Link in Energy Procurement

DISCOM intelligence in the Indian context means real-time, standardized data on tariff schedules, open access charges, banking rules, and regulatory amendments across all State Electricity Regulatory Commissions. This data is notoriously difficult to standardize: each SERC publishes tariff orders in different formats, on different schedules, with frequent mid-year amendments buried in supplementary notifications.

The cost of stale or incomplete DISCOM data is concrete. Buyers who negotiate PPAs without current open access charge data often discover the true landed cost of renewable power is higher than projected, eroding expected savings. Karnataka's reduction of additional surcharges to ₹0.40 per kWh in March 2026 improved third-party open access economics—but only for buyers who updated their models in time. Gujarat's extension of the ₹1.50 per kWh solar banking charge through June 2026 changed financial projections for every solar open access buyer in the state.

These state-level differences make cross-state comparison essential. Real-time DISCOM intelligence lets procurement teams identify the highest-ROI opportunities and avoid states with prohibitive regulatory charges. The spread in outcomes is significant:

- High-charge states (8% banking fees, strict ToD withdrawal constraints): solar open access economics often collapse

- Low-charge states (minimal banking fees, flexible withdrawal windows): the same technology can deliver ₹3–5 per unit savings

Opten Power's Real-Time DISCOM Intelligence standardizes landing prices across all states, enabling instant comparison of tariffs, savings, and ROI across developers and geographies. This directly accelerates deal closure: buyers with complete regulatory clarity can issue precise RFPs and evaluate compliant offers faster. Having open access charge data pre-loaded into every financial model—rather than chased during negotiation—saves weeks and often determines whether a deal closes or stalls.

How AI and Digital Platforms Are Transforming Energy Optimization

Traditional consultant-led energy procurement is slow, expensive (often requiring ₹10–15 lakh mandates), and out of reach for most mid-sized C&I buyers. AI-powered platforms change that equation — delivering financial modeling, market data, and procurement tools that were once available only to large enterprises with dedicated advisory budgets.

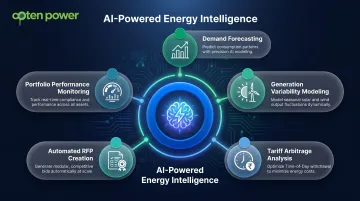

Specific AI capabilities transforming energy optimization include:

- Demand forecasting — predicting consumption patterns to optimize contract sizing

- Generation variability modeling — accounting for seasonal solar and wind output fluctuations

- Tariff arbitrage analysis — identifying optimal ToD withdrawal strategies

- Automated RFP creation — using modular templates to structure competitive bids

- Portfolio performance monitoring — tracking real-time generation, savings realization, and regulatory compliance

One of the most tangible shifts is in how buyers evaluate developer offers. Comparing price, contract terms, IRR, and payback periods across multiple developers in real time gives procurement teams genuine negotiating leverage — and confirmation that they're getting market-rate deals, not just the one they were shown first.

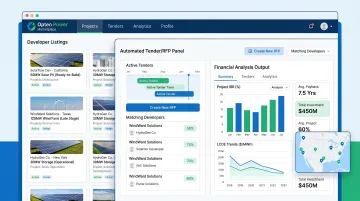

Opten Power's automated tender engine applies this directly: buyers create, distribute, and manage RFPs through modular templates, with bids collected and evaluated on the same platform. Paired with instant IRR and payback calculations, the process cuts traditional procurement timelines by up to 50% — what previously took weeks of back-and-forth now resolves in a matter of hours.

From Intelligence to Action: Optimizing Renewable Energy Procurement

Energy market intelligence only delivers value when it drives better procurement decisions. The right starting point is matching your procurement structure to your consumption profile and location:

- Open access — suited for multi-site operations managing distributed load

- Group captive — preferred by mid-sized buyers seeking minimal capital deployment

- Corporate PPA — designed for large enterprises wanting long-term price certainty

Corporate PPAs represent the most impactful procurement optimization tool for large C&I consumers. These long-term power purchase agreements (typically 15–25 years) lock in below-grid tariffs, delivering both cost certainty and ESG compliance benefits. Well-structured corporate PPAs in India can deliver savings of ₹3–5 per unit for qualifying C&I consumers, though actual savings are highly state-specific and depend on banking regulations, cross-subsidy surcharges, and ToD structures.

Third-party open access often becomes financially unviable when all charges apply; the group captive model—exempt from cross-subsidy and additional surcharges—preserves economics that third-party structures cannot match. Maharashtra's banking restrictions, for example, may reduce savings by at least 10% for third-party solar open access consumers, while group captive structures in the same state maintain full savings potential.

Opten Power's marketplace connects buyers directly to verified renewable capacity and automates the steps between discovery and contract signing:

- Access to 4+ GW of renewable projects across solar, wind, and hybrid technologies

- Automated tender engine with modular RFP templates

- Pre-approved contract templates for Capex, Group-Capex, and Third-Party Open Access structures

- Real-time developer comparison and instant financial analysis

- 50% faster deal closure from discovery to contract finalization

The platform's presence across 16 states and partnerships with India's top power producers ensure that buyers can discover, evaluate, and transact on quality renewable capacity regardless of their geographic footprint.

Buyers with multi-state operations or phased energy needs should diversify across technologies rather than committing to a single structure. Solar covers daytime manufacturing loads; wind suits 24/7 base load industries like steel and cement; hybrid systems serve data centers and hospitals requiring round-the-clock availability. Where feasible, blending short-term and long-term PPAs adds cost optimization without sacrificing operational flexibility.

Financial modeling at the procurement stage prevents expensive post-signing surprises. Buyers who run instant IRR, payback, and regulatory analysis before signing achieve better deal economics than those who rely on developer-provided projections. A 10 MW solar PPA with a projected IRR of 14% based on outdated banking assumptions may deliver only 10% when ToD restrictions and monthly banking expiry are properly modeled.

Energy Portfolio Management: What Top Enterprises Are Doing Differently

Large enterprises have moved from transactional energy buying to portfolio-based management — treating energy as an asset class, not a utility cost center. Consolidated visibility over renewable investments, contracts, and performance metrics enables active, deliberate management of costs and compliance.

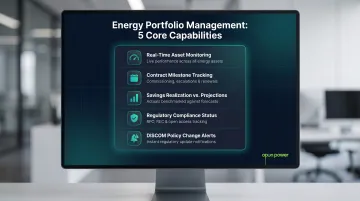

Key capabilities of an energy portfolio management dashboard include:

- Real-time performance monitoring of all renewable assets

- Contract milestone tracking (commissioning dates, tariff escalations, contract renewals)

- Savings realization versus projections

- Regulatory compliance status (RPO obligations, REC purchases, open access renewals)

- Early-warning flags for DISCOM policy changes that could affect portfolio economics

Complete portfolio visibility reduces energy cost leakages. Without consolidated monitoring, enterprises miss generation shortfalls, billing errors, banking deadline violations, and suboptimal dispatch decisions. Maharashtra's monthly expiry of unused banked energy, for instance, means buyers who don't actively manage withdrawal schedules forfeit energy they've already paid for.

The financial exposure compounds further: deviation settlement charges and scheduling penalties in states with strict forecasting requirements add real costs to portfolios managed without oversight.

These cost risks are also driving structured procurement decisions. Top enterprises are formalizing green procurement through GEOA regulations and state-level green tariff policies. RE100 member companies met 56% of their 2023 electricity consumption with clean energy globally, with India contributing a significant share through PPAs and open access structures.

Opten Power's Portfolio Management Dashboard gives buyers a single view across all renewable contracts, technologies, and compliance obligations — so portfolio decisions are driven by data, not scattered spreadsheets.

Frequently Asked Questions

What is energy market intelligence and why does it matter for businesses in 2026?

Energy market intelligence is real-time, structured data covering energy tariffs, regulatory policies, developer capacity, and financial metrics. In 2026, its accuracy determines whether a business overpays or optimizes costs — DISCOM policies shift frequently, and state-wise open access charges can reshape deal economics overnight.

How can Indian C&I companies reduce electricity costs through energy market intelligence?

Real-time tariff benchmarking, continuous regulatory monitoring, and instant financial modeling help procurement teams identify the right structure — open access, group captive, or corporate PPA — at the right time. This prevents overpayment on grid power and accelerates savings by grounding every decision in current data.

What is a Corporate PPA and how does it help with energy cost optimization?

A Corporate PPA is a long-term power purchase agreement (typically 15–25 years) directly between a business and a renewable energy developer. It locks in below-grid tariffs, providing both cost certainty and ESG compliance. Well-structured corporate PPAs in India can deliver savings of ₹3–5 per unit for qualifying C&I consumers with significant electricity demand.

How does real-time DISCOM intelligence improve renewable energy procurement decisions?

Real-time DISCOM intelligence standardizes state-wise open access charges, banking rules, and tariff schedules into comparable data, enabling buyers to calculate the true landed cost of renewable power. This prevents procurement decisions based on incomplete or outdated regulatory assumptions, which often erase projected savings when actual charges are applied post-signing.

What are the key energy market trends in India that C&I buyers must prepare for in 2026?

India added 44.51 GW of renewable capacity in 2025, creating more competitive PPA pricing. Open access regulations continue evolving across 27 states with frequent amendments. Rising RPO obligations are pushing mandatory renewable procurement. AI-powered platforms are democratizing sophisticated energy optimization, making it accessible to mid-size enterprises previously unable to afford consultant-led procurement.

How much faster can businesses close renewable energy deals using a digital marketplace platform?

Automated RFP engines, pre-approved contract templates, and real-time developer comparison can compress deal timelines by up to 50% versus traditional consultant-led procurement. Opten Power's platform moves deals from discovery to contract finalization through automated tendering and instant financial analysis — cutting weeks of manual coordination down to hours.