Key Takeaways

- Long-term renewable PPAs and Group Captive models are replacing short-term DISCOM dependency as the default for mid-to-large C&I buyers

- Digital procurement platforms cut deal timelines from months to days using automated RFPs and live tariff benchmarking

- Hybrid solar-wind and solar-plus-storage portfolios are overtaking standalone projects as 24×7 clean power demands grow

- Real-time DISCOM intelligence has become essential as state-by-state regulatory complexity intensifies

- ESG mandates — SEBI BRSR and Scope 2 accountability — have made renewable procurement a board-level business decision, not just a cost play

Long-Term Renewable PPAs and Group Captive Models Are Going Mainstream

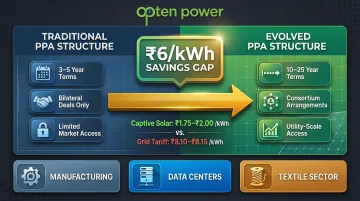

Corporate PPAs and Group Captive Power Purchase Agreements (GCPPAs) are no longer exclusive to large industrial buyers. Mid-sized C&I companies in manufacturing, IT parks, and textile exports are now accessing these structures.

Under Indian regulations, participation requires a 26% equity stake and minimum 51% self-consumption — requirements that were once barriers, but are increasingly manageable through consortium arrangements.

The savings are hard to ignore. In Rajasthan, captive solar landing costs range from ₹1.75–₹2.00/kWh compared to grid costs of ₹8.10–₹8.15/kWh — roughly ₹6/kWh in savings. That spread helps explain why India added a record 7.8 GW of solar open access capacity in 2025 alone.

Real-world adoption patterns:

- Manufacturing clusters, data centers, and textile exporters lead uptake

- Multi-company consortia enable smaller buyers to pool equity for utility-scale projects

- Tata Power Renewable Energy's 13.2 MW group captive agreement with Force Motors and Jaya Hind Industries demonstrates mainstream momentum

As adoption scales, contract structures are also changing. PPAs have shifted from 3–5 year terms to 10–15 years (some extending to 25 years), driven by buyer confidence in project longevity and lender requirements. Procurement teams now evaluate these commitments with the same rigor as capital expenditure decisions.

Key barriers remain:

- Grid connectivity delays across states

- Inconsistent banking regulations by state

- Counterparty credit risk assessment

Digital marketplaces are addressing these by pre-screening developers and standardizing contract terms, cutting negotiation time significantly.

Automated Digital Procurement Platforms Replacing Manual RFP Processes

Traditional energy procurement was slow and opaque. Manual RFP creation, bilateral negotiations lasting 3-6 months, limited price benchmarking, and Excel-based financial modeling left procurement teams with information asymmetry against experienced developers. These manual processes typically spanned three to eight months, with project execution adding another 4-6 months.

Digital platforms have fundamentally changed this dynamic:

- Automated tender engines with modular RFP templates enable structured bid collection from multiple developers

- Real-time capacity discovery across 4+ GW of renewable projects (solar, wind, hybrid)

- Side-by-side tariff, savings, and IRR comparisons replace weeks of manual modeling

- Pre-approved contract frameworks reduce negotiation cycles

Platforms like Opten Power enable C&I buyers to close deals up to 50% faster by streamlining every step from discovery through contract finalization.

The analytics layer behind these platforms does the heavy lifting that once required a dedicated energy team. Instant IRR calculations, payback period analysis, and regulatory charge simulations — covering open access costs like wheeling charges, banking, and cross-subsidy surcharges across Indian states — are now automated. Buyers without in-house specialists make decisions with the same data depth as large corporates.

Portfolio management dashboards matter most to buyers running multi-site or multi-state operations. A single interface covering all renewable contracts, generation performance, and realized savings gives procurement teams the control to spot underperforming assets and act — instead of reconciling numbers across disconnected spreadsheets.

Hybrid Energy Portfolios and Storage Integration for 24×7 Clean Power

Standalone solar or wind projects no longer meet the needs of energy-intensive industries requiring reliable round-the-clock power. Steel, cement, hospitals, and data centers demand more sophisticated solutions.

BloombergNEF reports that rapidly increasing hours of negative power prices are eroding the value of standalone solar and wind deals, pushing buyers toward hybrid portfolios. When solar generation peaks midday but demand doesn't, prices can collapse into negative territory.

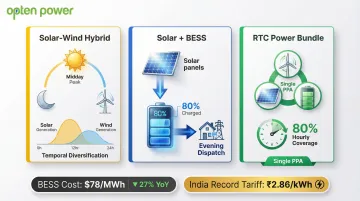

Three dominant hybrid configurations have emerged in India:

- Solar-wind hybrid for geographic and temporal diversification—solar peaks midday while wind generates strongest at night

- Solar + Battery Energy Storage Systems (BESS) for peak-shifting and firm power delivery

- RTC (round-the-clock) power bundles combining wind, solar, and BESS under a single PPA for load-following delivery (for example, Serentica Renewables' 100 MW RTC deal with SECI targeting 80% hourly demand coverage)

Storage costs have dropped sharply. Global 4-hour BESS benchmark costs fell 27% year-on-year to $78/MWh in 2025, making India's solar-plus-storage auction tariffs as low as ₹2.86/kWh economically viable.

Procurement Implications

Buying hybrid or firm power bundles requires co-located asset evaluation, storage dispatch modeling, and more sophisticated contract structures. Automated platforms and expert advisory are now essential to navigate this complexity.

State-Level Regulatory Intelligence and DISCOM Tariff Navigation

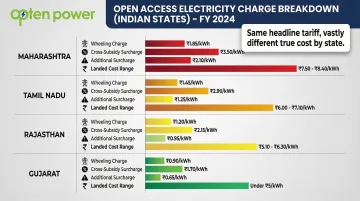

India's regulatory complexity creates a hidden cost trap for energy buyers. Open access charges—wheeling, transmission, banking, cross-subsidy surcharge, and additional surcharge—vary dramatically across states, making headline tariff comparisons meaningless without knowing the true landed cost for a specific consumer in a specific state.

The cost divergence is significant:

- Maharashtra: Cross Subsidy Surcharge ₹1.79/kWh, Additional Surcharge ₹1.36/kVAh, Wheeling ₹0.60/kVAh

- Tamil Nadu: Wheeling/Network Charge ₹1.04/kWh, Cross Subsidy Surcharge ₹1.99/kWh

- Q4 2025 net landed open access costs ranged from under ₹5/kWh to ₹8.4/kWh across states

A project appearing cheaper in one state can be substantially more expensive after regulatory levies in another.

Real-time DISCOM intelligence has become a core capability requirement. Buyers need standardized, updated landing price data across all relevant states to make apples-to-apples cost comparisons. Opten Power's platform covers 16 states and shows buyers the true landed cost in each one, with state-specific charges already factored in.

That kind of visibility only holds value if the underlying regulatory data stays current. In March 2026, Maharashtra's MERC revised Time-of-Day banking rules, clarifying that banked energy can only be drawn within the same or lower tariff time block. Buyers relying on outdated information risk financial penalties or project delays. Across India's 28 states, rule changes like this happen without warning — making continuous regulatory monitoring a commercial necessity, not an afterthought.

ESG Mandates and Scope 2 Emissions Accountability Driving Procurement Decisions

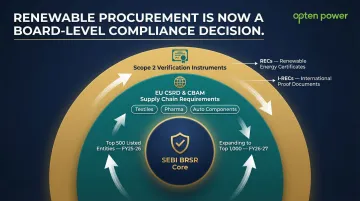

SEBI's Business Responsibility and Sustainability Report (BRSR) framework, introduced in May 2021, is now mandatory for India's top listed companies. The BRSR Core assurance glidepath mandates compliance for the top 500 listed entities in FY25-26, expanding to the top 1,000 in FY26-27. This transforms renewable energy procurement from a cost optimization exercise into a compliance and reporting imperative.

Global supply chain pressure adds another layer. Export-oriented sectors — textiles, auto components, pharmaceuticals — now face procurement requirements from European and American customers under the EU's CSRD and CBAM regulations. For Indian suppliers, this means:

- Verified Scope 1, 2, and 3 emissions data is no longer optional

- High-emission producers risk direct commercial penalties and price renegotiations

- Failure to meet buyer ESG thresholds can disqualify suppliers from contracts entirely

Renewable Energy Certificates (RECs) and I-RECs are now required as proof instruments for Scope 2 claims. CERC's REC Regulations 2022 introduced fungibility across technologies to meet RPO targets, and RE100 technical criteria permit corporate buyers to use RECs for verified renewable electricity claims. For procurement teams, this means documentation and third-party certification carry the same weight as negotiating the lowest tariff.

What's Driving These Commercial Energy Procurement Shifts

These five trends share common underlying drivers specific to India's C&I energy landscape.

Regulatory and Policy Tailwinds

India's target of 50% cumulative electric power installed capacity from non-fossil fuel-based sources by 2030 has created a large, competitive pipeline of renewable capacity seeking long-term offtake. As of December 2025, 51.93% of India's 513,730 MW total installed capacity came from non-fossil sources.

The Ministry of Power's RPO trajectory mandates that by FY 2030, 43.33% of required supply must come from non-fossil sources. This structural demand sustains the PPA market even during uncertain macro environments.

On the compliance side, the Electricity (Amendment) Rules, 2026 (effective March 2026) provide critical clarity: SPVs are now explicitly classified as Associations of Persons, and indirect ownership can satisfy the 26% equity threshold—removing the single largest uncertainty for Group Captive buyers.

Rising DISCOM Tariff Pressure and Grid Reliability Concerns

Commercial and industrial DISCOM tariffs have risen consistently due to cross-subsidy loading and distribution infrastructure underinvestment. Current approved rates illustrate the burden:

| State | Energy Charge | Demand Charge | Source |

|---|---|---|---|

| Tamil Nadu (HT Industry) | ₹7.50/kWh | ₹608/kVA/month | TNEB FY 2025-26 |

| Maharashtra (HT Industry) | ₹7.04/kVAh | ₹575/kVA/month | MSEDCL MYT Order |

High Cross-Subsidy Surcharges (₹1.99/kWh in Tamil Nadu) are levied to compensate DISCOMs for lost cross-subsidy when C&I consumers switch to open access. This creates a direct economic case for moving to renewable sources via open access or captive arrangements.

Technology Cost Deflation

Continued decline in component costs has made renewable PPAs cheaper than grid power for most commercial consumers. Recent benchmarks confirm the shift:

- Global solar module prices hit $0.096/Watt in Q3 2024 — a record low that flows directly into project economics

- SECI's October 2025 solar + storage auction cleared at ₹2.86/kWh, setting a new floor for dispatchable renewable supply

- CERC-approved wind tariffs in December 2025 came in at ₹3.97/kWh

Against Tamil Nadu's ₹7.50/kWh grid rate, the cost argument for renewables is straightforward. The "green premium" objection no longer holds in sun- and wind-rich states.

Competitive Dynamics and Market Maturation

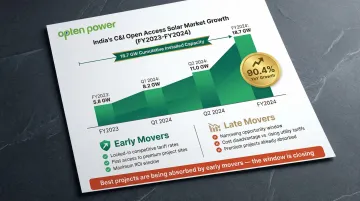

The C&I open access market's annual installed capacity grew 90.4% between FY2023 and FY2024, reaching 18.7 GW cumulative by end-FY2024. As large buyers lock in long-term renewable contracts at favorable rates, smaller competitors face cost disadvantages if they remain on utility tariffs. Mid-sized buyers who delayed procurement decisions are now finding that the window for competitive contract rates is narrowing — the best projects get absorbed by early movers.

How These Trends Are Impacting C&I Energy Buyers in India

The combined effect of these trends is reshaping how businesses plan, budget, and report on energy as a strategic asset.

Operational Impact

Energy procurement is shifting from a reactive, annual budgeting task to a continuous, data-driven function. Procurement, finance, and sustainability teams now need:

- Real-time price monitoring across multiple states and developers

- Developer relationship management to maintain access to competitive pipeline

- Contract performance tracking for multi-year PPAs spanning 10–15 years

- Regulatory compliance monitoring to adapt to evolving SERC orders and open access frameworks

Buyers without dedicated energy teams or digital infrastructure are already falling behind on all four fronts. The financial stakes raise the bar further.

Business and Strategic Impact

CFOs and boards now evaluate energy procurement decisions with the same rigor as capital expenditure. Long-term PPAs represent 10-15 year financial commitments with significant balance sheet implications, requiring scrutiny of:

- Internal Rate of Return (IRR) and payback periods — often the first filter applied by CFOs

- Counterparty credit risk, particularly developer financial stability over a decade-plus horizon

- Regulatory exposure to future changes in open access charges and SERC frameworks

- ESG reporting alignment with SEBI BRSR and global supply chain disclosure requirements

Energy procurement decisions made today will show up on balance sheets — and in sustainability disclosures — for the next decade. Getting them right is a competitive advantage, not just a cost control exercise.

Future Signals for Commercial Energy Procurement in India Through 2027

The trends covered above are still playing out. Over the next 1-3 years, procurement professionals in India should track these early-stage shifts:

BESS-inclusive PPAs go mainstream. As battery costs fall, solar-plus-storage will shift from a premium add-on to the default configuration for most deals — especially for buyers who need firm, round-the-clock power delivery.

Green hydrogen enters the procurement conversation. NITI Aayog projects India's green hydrogen LCOH could fall to $1.60/kg by 2030, approaching parity with grey hydrogen. Sectors that can't easily electrify — fertilizers, steel, chemicals — will begin exploring hydrogen as a viable procurement option once production costs reach that threshold.

CERC/SERC regulatory convergence. India's National Open Access Registry (NOAR) now automates short-term open access (STOA) administration as a centralized platform. Deeper harmonization could further simplify inter-state open access and reduce the state-by-state compliance burden buyers currently navigate.

Short-term power markets demand new capabilities. India's move to 15-minute electricity scheduling and settlement (across MTOA and STOA markets) creates new procurement opportunities alongside new risks. Buyers will need short-term trading capabilities to complement their long-term PPA portfolios.

Hourly GHG matching becomes the standard. The GHG Protocol's proposed Scope 2 Guidance updates (public consultation launched October 2025) would require hourly, location-matched verification of market instruments against actual consumption. Buyers who build these matching capabilities now will be better positioned when these standards take hold in India.

Conclusion

Commercial energy procurement in India in 2026 has outgrown utility bill management. It now demands real-time market intelligence, digital deal infrastructure, and a portfolio mindset — three capabilities that determine whether your energy costs shrink or compound.

Businesses that move early to restructure procurement around the following will build advantages that late movers will struggle to close:

- Long-term renewables — locking in tariffs before grid parity narrows the arbitrage

- Digital procurement platforms — compressing deal timelines and reducing counterparty risk

- Regulatory intelligence — staying ahead of state-level DISCOM changes before they hit the bottom line

- ESG credibility — meeting disclosure requirements before they become mandatory thresholds

Platforms like Opten Power are built for exactly this shift, giving C&I buyers access to 4+ GW of projects, real-time DISCOM pricing, and automated RFP tools in one place. The procurement decisions made in the next 12 months will define energy cost structures for the rest of the decade.

Frequently Asked Questions

What is a corporate Power Purchase Agreement (PPA) and how does it work for commercial buyers in India?

A corporate PPA is a long-term contract between a commercial buyer and a renewable energy developer at a pre-agreed tariff, typically structured as an open access arrangement. Key variants include third-party PPAs (zero upfront capital, developer owns assets) and Group Captive PPAs (26% equity stake, 51% self-consumption requirement, shared ownership).

What is Group Captive energy procurement and who is it suited for?

Group Captive structures require buyers to hold a minimum 26% ownership stake and consume at least 51% of the generated electricity. It's suited for medium-to-large C&I buyers seeking lower tariffs and regulatory benefits like wheeling charge exemptions. Consortia models now make it accessible to smaller buyers who can pool equity stakes to access utility-scale projects.

How much can commercial businesses save by switching from DISCOM tariffs to renewable PPAs?

Savings vary by state, consumer category, and contract structure. In Rajasthan, captive solar landing costs of ₹1.75–₹2.00/kWh compare to grid costs of ₹8.10–₹8.15/kWh—roughly ₹6/kWh in savings. Platforms like Opten Power have documented cost reductions of up to 40% for C&I buyers versus commercial grid tariffs.

What are open access charges and how do they affect the true cost of renewable energy procurement in India?

Open access lets large consumers source power outside their DISCOM, but state regulators add charges—wheeling, banking, cross-subsidy surcharge, transmission, and additional surcharge. These vary widely by state (Tamil Nadu's CSS: ₹1.99/kWh; Maharashtra's: ₹1.79/kWh), so headline tariffs are only meaningful once state-specific levies are factored into the landed cost.

How are ESG and sustainability reporting requirements changing energy procurement decisions for Indian businesses?

SEBI's BRSR mandate for the top 1,000 listed companies and the EU's CBAM and CSRD regulations are driving demand for certified renewable energy. Scope 2 emissions tracking is now a compliance requirement, with RECs and I-RECs serving as proof instruments for corporate reporting and global supply chain accountability.

What should commercial energy buyers look for when evaluating a digital energy procurement platform?

Prioritize platforms that offer:

- Real-time DISCOM tariff intelligence across states to surface true landed costs

- Automated RFP and tendering tools to shorten deal timelines

- Transparent developer comparisons with instant IRR and payback analysis

- Portfolio dashboards for contract oversight across multi-site operations