Introduction: What Is Third-Party Ownership Financing in Energy Projects?

For energy-intensive industries like cement, energy costs account for up to 40% of total production costs — yet direct ownership of renewable assets requires significant upfront capital that most commercial and industrial buyers cannot easily deploy. That gap between the need for clean energy and the ability to finance it is exactly the problem third-party ownership solves.

Third-party ownership (TPO) financing separates the party that finances and owns the energy asset from the party that consumes the energy. A developer or financier owns the plant; the business buys the power at a contracted tariff — with no capital on the balance sheet.

This model has reshaped how industries access clean energy in India, accelerating sharply after the Green Energy Open Access (GEOA) Rules 2022 lowered the eligibility threshold from 1 MW to 100 kW. India added 7.8 GW of solar open access capacity in 2025 alone, bringing cumulative installed capacity to over 30 GW.

This article breaks down the main TPO structures — PPAs, leases, and RESCO models — along with the financial, regulatory, and risk considerations that determine which one fits your business.

Key Takeaways

- TPO means a developer or investor owns the energy asset while your business pays only for the energy it consumes

- The three main structures are Power Purchase Agreements (PPAs), leases, and partnership flip arrangements

- TPO eliminates upfront capital costs and maintenance obligations but limits your control and direct access to tax benefits

- Choosing the right structure depends on your financial profile, risk tolerance, and long-term energy goals

What Is Third-Party Ownership in Energy Projects?

Third-party ownership is a financing and operational model where an external developer or investor procures, builds, owns, and operates the energy system on or off the buyer's site, while the buyer (off-taker) pays for the energy generated under a structured contract.

Why TPO Emerged

Most C&I businesses — including manufacturers, data centres, hospitals, and IT parks — lack the capital, technical expertise, or appetite to directly own energy infrastructure, yet need stable, cost-effective power.

The CAPEX model accounted for 85–88% of rooftop solar installations in India between 2024 and 2025 — a figure that reflects how much upfront capital direct ownership demands. TPO structures address this directly, letting businesses access renewable energy without pulling capital away from core operations.

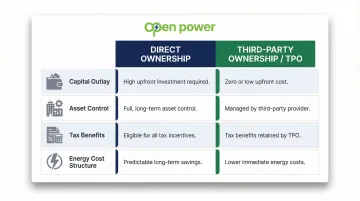

TPO vs. Direct Ownership

| Direct Ownership | TPO | |

|---|---|---|

| Capital outlay | Paid by the business | Paid by the developer |

| Asset control | Business owns the system | Developer/SPV owns the system |

| Tax benefits | Business claims depreciation | Developer captures incentives (e.g., 40% accelerated depreciation under Section 32 of the Income Tax Act) |

| Energy cost | Based on actual system costs | Lower contracted rate passed through by developer |

Key Parties in TPO Structures

Every TPO structure involves four primary stakeholders:

- Off-taker (energy buyer): Consumes the energy and pays contracted rates

- Developer/SPV (asset owner and operator): Finances, builds, owns, and operates the energy system

- Tax equity investor (where applicable): Provides capital to capture tax benefits, particularly in flip structures

- Lender: Provides debt financing to the developer or SPV

The Indian Context

In India, TPO structures are most commonly deployed under open access regulations. State-level DISCOM rules, banking provisions, and wheeling charges significantly shape which structures are viable. For example, Karnataka recorded a 240% quarter-over-quarter increase in cross-subsidy charges in 2025, while Tamil Nadu introduced an 8% banking charge and eliminated banking entirely for Third-Party Open Access transactions.

State-level policy shifts like these can move a project from viable to unviable — which is why structure selection always starts with a state-specific regulatory and cost analysis.

The Main TPO Financing Structures Explained

Power Purchase Agreement (PPA)

In a PPA, the developer installs and operates the renewable energy system — typically solar, wind, or hybrid — and the off-taker agrees to purchase the electricity generated at a pre-negotiated rate over a fixed term, typically 15–25 years in India.

Two Main PPA Variants in India:

- On-site (captive) PPAs: The system is installed at the buyer's premises; power is consumed directly without grid transmission.

- Off-site (group captive or third-party sale) PPAs: Power is generated remotely and wheeled through the grid under open access. Regulatory treatment, cross-subsidy charges, and banking rules differ significantly from on-site models.

PPA Pricing Mechanics:

PPAs can feature fixed-rate or escalating-rate structures. The developer monetises tax benefits — particularly the 40% accelerated depreciation available under Section 32 of the Income Tax Act — to offer a competitive tariff. The AD benefit can impact PPA tariffs by around ₹0.2-0.3 per kWh.

State open access incentives lower the landed cost of power compared with on-grid DISCOM tariffs by 25-30%, driving C&I capacity additions.

Platforms like Opten Power enable businesses to compare live PPA tariffs, savings projections, and IRR across multiple developers across 16 states in real time, accelerating decision-making.

Solar/Renewable Energy Lease

In the lease model, the business leases the renewable energy equipment from a third-party owner for a fixed period (typically 10–15 years), paying a regular lease fee rather than a per-unit energy charge. The business consumes all generation from the system.

Key Distinction from a PPA:

In a lease, the off-taker pays for the equipment's availability (fixed periodic payment) regardless of how much energy is produced. In a PPA, payments are tied to actual energy output.

The lease model is less common in India compared to PPAs — the OPEX/RESCO model accounted for only 12-15% of rooftop solar installations in 2024-2025. However, it may suit businesses that want more operational control without full ownership.

Partnership Flip / Tax Equity Structure

In a partnership flip, a developer and a tax equity investor jointly form a Special Purpose Vehicle (SPV) to own and operate the project. Initially, the tax equity investor holds the majority economic interest to capture available tax incentives — such as the 40% accelerated depreciation under India's Income Tax Act.

After the investor has realised its targeted return — typically within 5–7 years — ownership "flips" predominantly to the developer.

Pathway to Ownership:

This structure enables the off-taker to acquire the project at a pre-agreed fair market value after the flip period. Key structural features include:

- Tax equity investor holds majority interest during the incentive capture phase (typically 5–7 years)

- Ownership shifts to the developer once the investor's target return is met

- Off-taker gains a contractual option to purchase at fair market value post-flip

- Higher transaction complexity makes this structure more common in large-scale utility or C&I projects

In India, investors use tax arbitrage by placing RE asset SPVs in a Hold-Co structure, allowing the 40% accelerated depreciation to be offset against external sources of taxable income — a structuring approach shaped by domestic tax law rather than the grant-based incentives common in other markets.

TPO vs. Direct Ownership: Key Differences

The right financing structure depends on your capital priorities, risk appetite, and operational preferences. This comparison covers the key dimensions C&I buyers and project financiers typically evaluate.

| Criteria | Direct Ownership | PPA | Lease/Flip |

|---|---|---|---|

| Upfront Capital Required | High (full project cost) | None or minimal | None or minimal |

| Asset Ownership | Buyer/developer | Third-party (TPO) | Third-party; transfers at flip point |

| Balance Sheet Impact | On-balance-sheet | Off-balance-sheet | Off-balance-sheet |

| Tax Benefit Utilization | Buyer retains | TPO monetizes | TPO monetizes pre-flip; buyer post-flip |

| Operational Responsibility | Buyer | TPO | TPO (typically) |

| Energy Cost Structure | Variable (market-linked) | Fixed or escalating tariff | Fixed or escalating tariff |

| Typical Contract Term | Asset life (20–25 years) | 10–25 years | 10–20 years |

| Best Suited For | Entities with strong tax appetite and capital access | C&I buyers seeking predictable costs with zero capex | Investors seeking near-term returns with eventual ownership transfer |