Introduction

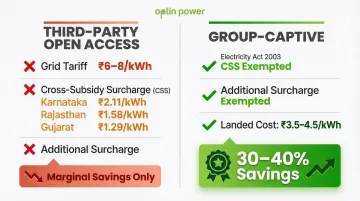

Solar open access (OA) enables commercial and industrial (C&I) consumers to procure solar power directly from generators, bypassing distribution companies (DISCOMs) to access competitive tariffs. For C&I buyers facing industrial grid tariffs ranging from ₹6–8/kWh in states like Karnataka and Maharashtra, OA delivers landed costs as low as ₹3.5–4.5/kWh—translating to savings of 30–40% on annual energy bills.

India hit record solar OA installations in 2025, crossing 7.8 GW of new capacity and surpassing 30 GW cumulative. June 2025's expiry of the 100% ISTS charge waiver triggered a commissioning rush, followed by a Q4 slowdown that reshaped project timelines heading into 2026.

With 45+ GW in the development pipeline and regulatory divergence intensifying across states, 2026 is shaping up as a defining year for the market. This article covers the key policy shifts, state-level trends, and commercial strategies C&I buyers, developers, and investors need to track.

Key Takeaways

- India added 7.8 GW of solar open access in 2025, crossing 30 GW cumulative, with 45+ GW in the pipeline entering 2026

- ISTS charge waiver expiry in June 2025 front-loaded commissioning in H1, pushing Q4 installations down 32% year-on-year

- Group-captive structures dominate due to cross-subsidy surcharge and additional surcharge exemptions — with Green Day-Ahead Market (G-DAM) volumes up 18% QoQ as a parallel revenue channel

- Wind-solar hybrid and solar-plus-storage are becoming the go-to configurations for 24x7 industrial power needs

- State-level regulatory divergence on banking, OA charges, and approvals remains the biggest execution risk for 2026

C&I-Led Demand Surge and Record Capacity Milestones

India's solar OA market reached its highest-ever annual installation of 7.8 GW in CY2025, marginally up from 7.7 GW in 2024. Cumulative capacity crossed 30 GW by year-end, marking the sector's maturation from opportunistic growth to structural market presence.

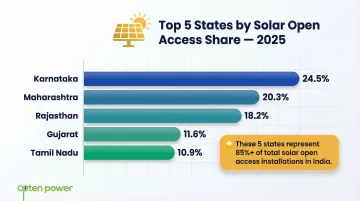

Geographic concentration remained sharp, with five states driving the bulk of activity:

- Karnataka: 24.5% of 2025 additions

- Maharashtra: 20.3%

- Rajasthan: 18.2%

- Gujarat: 11.6%

- Tamil Nadu: 10.9%

Together, these states accounted for over 85% of total installations, driven by sustained C&I demand for decarbonization and cost management. Maharashtra, Tamil Nadu, and Gujarat led specifically in Q4 2025.

That momentum stalled sharply in Q4 2025. Installations dropped to 1.6 GW — down 29% QoQ and 32% YoY from Q4 2024.

The drop traces directly to the June 2025 expiry of the 100% ISTS charge waiver, which pushed developers to rush commissioning in H1, leaving a thinner pipeline for later months. C&I buyers should expect similar dynamics in 2026 as phased ISTS charges continue reshaping project economics.

Despite the Q4 dip, underlying demand remains strong. More than 45 GW of solar OA projects were under development or in pre-construction phases as of end-2025, driven by:

- Rising grid tariffs (now ₹6–8/kWh for industrial consumers in key states)

- Mandatory Renewable Purchase Obligation (RPO) compliance deadlines

- Corporate net-zero commitments accelerating procurement timelines

Navigating a 45 GW pipeline across fragmented state regulations is no small task. Opten Power addresses this directly—offering 4+ GW of available renewable projects across 16 states through real-time DISCOM intelligence, automated RFPs, and instant IRR analysis. The platform connects C&I buyers with developers without the complexity of managing multi-state procurement independently.

Regulatory Shifts: ISTS Waivers, Green OA Policy, and State-Level Divergence

ISTS Charge Waiver Expiry Reshapes Project Economics

The June 2025 expiry of the 100% ISTS charge waiver altered interstate solar OA project viability. Projects commissioned before June 30, 2025, secured a 25-year waiver on inter-state transmission charges. Post-June projects now face phased charge reintroduction:

| Commissioning Period | ISTS Waiver | Duration |

|--------------------------|----------------|--------------|

| Before June 30, 2025 | 100% | 25 years |

| July 1, 2025 – June 30, 2026 | 75% | 25 years |

| July 1, 2026 – June 30, 2027 | 50% | 25 years |

| July 1, 2027 – June 30, 2028 | 25% | 25 years |

| After June 30, 2028 | 0% | N/A |

Projects commissioned in FY27 will pay 50% of full ISTS charges for 25 years—adding ₹0.15-0.25/kWh to landed costs. This cost escalation is pushing developers and C&I buyers toward intra-state OA configurations or hybrid models that optimize for lower transmission dependencies.

Green OA Policy Implementation Faces State Resistance

The Centre's Green Energy Open Access Rules (2022) established a 100 kW eligibility threshold, mandated monthly banking (up to 30% of consumption), and designated a Central Nodal Agency for single-window approvals. State-level deviations continue to undermine these provisions across three key areas:

- Eligibility thresholds ignored: Many states retain 1 MW minimum limits despite the Centre's 100 kW rule, locking out smaller C&I consumers.

- Banking effectively eliminated for TPOA: Tamil Nadu's GEOA Regulations 2025 introduced an 8% banking charge, explicitly banning banking for third-party power purchase. Andhra Pradesh capped banked energy at 30% of monthly consumption, with unutilized surplus paid at just 75% of the latest SECI tender rate.

- DISCOM entrenchment delays approvals: States resist removing DISCOMs as nodal agencies, creating approval bottlenecks and ongoing jurisdictional litigation with the Centre.

State-Level Regulatory Divergence Dominates Execution Risk

Regulatory inconsistency across states is the single biggest execution risk for 2026:

Maharashtra and Rajasthan have introduced multi-year tariff structures that give buyers long-term cost visibility. Most other states still issue annual tariff orders, creating meaningful uncertainty for 20-25 year PPAs. On banking, Karnataka offers relatively flexible terms, while Telangana and Haryana have imposed time-of-day constraints that compress OA project returns.

Cross-Subsidy Surcharges remain elevated for third-party OA consumers in FY26, despite Green OA Rules:

- Karnataka (BESCOM): ₹2.11/kWh

- Rajasthan (JVVNL): ₹1.58/kWh

- Gujarat (DGVCL): ₹1.29/kWh

At these CSS levels, third-party OA savings are marginal against grid tariffs for most C&I buyers. Group-captive structures — which carry CSS and Additional Surcharge exemptions — offer a more defensible economics case, which is why procurement strategy in 2026 increasingly defaults to this route.

Wind-Solar Hybrid and Energy Storage: The Next OA Configuration

Wind-Solar Hybrids Deliver Stable Power Profiles

Wind-solar hybrid OA projects are gaining traction among C&I consumers requiring consistent power generation. Hybrid configurations offer:

- Better Capacity Utilisation Factor (CUF): Solar peaks during daytime hours; wind generates more at night and during monsoons, smoothing generation curves

- Reduced grid instability: More predictable generation reduces reliance on banking or grid backups

- Optimized tariffs: Combined resource availability lowers per-unit costs compared to standalone solar

States like Gujarat, Karnataka, and Tamil Nadu are leading hybrid OA installations. Hero Future Energies commissioned a 125 MW hybrid project (99 MW solar + 26 MW wind) in Karnataka in April 2025 under a group-captive model, completing installation in under six months. For C&I buyers, that six-month timeline signals hybrid OA is no longer an emerging option — it's a deployable one.

Solar-Plus-Storage Emerges as Banking Alternative

As states tighten banking provisions, Battery Energy Storage Systems (BESS) integrated with solar OA are becoming the alternative for managing surplus energy. Solar-plus-storage is especially relevant for energy-intensive industries with 24x7 power demand—data centres, steel, hospitals, and process industries.

Rajasthan's BESS mandate: The RERC GEOA Regulations 2025 mandate that captive RE plants exceeding 100% (up to 200%) of contract demand must install BESS for at least 20% of the additional capacity's energy generation. To incentivize compliance, Rajasthan offers a 75% exemption on transmission and wheeling charges for seven years for RE projects with BESS of at least 5% of renewable capacity.

CleanMax + Sangam India: In April 2026, CleanMax partnered with Sangam India to supply 50 MW of hybrid power (30 MW solar + 20 MW wind) augmented with a 2 MWh BESS from its Bhikamkor hybrid farm in Rajasthan under an intra-state group-captive structure. The deal shows BESS paired with hybrid sourcing can resolve both banking restrictions and around-the-clock load variability in a single contract structure.

Regulatory Treatment of Storage Under Green OA

Policy support is accelerating storage-integrated OA adoption. Battery ESS connected at substations where renewable generating stations operate qualify for a 100% ISTS waiver for 12 years if commissioned by June 30, 2028 — provided the ESS meets at least 51% of its annual charging requirement from renewable sources.

That waiver, combined with falling BESS costs, is shifting storage from a compliance expense to a financial advantage for C&I OA buyers.

India's BESS tariffs dropped sharply in 2025:

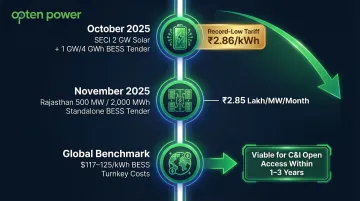

- SECI's 2 GW solar + 1 GW/4 GWh BESS tender discovered a record-low tariff of ₹2.86/kWh in October 2025

- Rajasthan's 500 MW/2,000 MWh standalone BESS tender concluded at ₹2.85 lakh/MW/month in November 2025

Global turnkey BESS costs fell to approximately $117–125/kWh (globally benchmarked; roughly ₹9,800–10,500/kWh) in 2025, making storage economically viable for C&I OA applications within the next 1–3 years.

Group-Captive Model Dominance and Green Power Market Expansion

Group-Captive Structure Delivers Lowest Landed Costs

The group-captive model continues as the preferred solar OA procurement structure in 2026 due to significant cost advantages. Under Section 9 of the Electricity Act 2003, captive generating plants are exempt from Cross-Subsidy Surcharge (CSS) and Additional Surcharge (AS), making landed costs substantially lower than third-party OA.

Legal reinforcement: The Supreme Court's 2021 ruling in Maharashtra State Electricity Distribution Co. Ltd. v. JSW Steel Limited reinforced that captive consumers form a distinct class and are not liable for additional surcharge under Section 42(4) of the Electricity Act 2003. This legal clarity strengthened the group-captive model's standing.

Regulatory requirements: To qualify as captive, projects must meet two conditions per Electricity Rules 2005:

- Captive users must hold at least 26% equity ownership

- Captive users must consume at least 51% of generated electricity annually

Persistent approval delays: Despite legal clarity, some states create friction through delayed approvals. In Haryana, HVPNL cancelled final connectivity for a 50 MW solar project in March 2025 because the developer could not satisfy DISCOM demands for captive shareholding verification prior to commissioning. Similar delays persist in Rajasthan, where DISCOMs request extensive documentation before granting approvals.

Green Power Exchange Markets Show Mixed Signals

Where state-level friction limits group-captive approvals, exchange-based green power trading offers an alternative exit. The Green Day-Ahead Market (G-DAM) and Green Term-Ahead Market (G-TAM) are emerging as complementary channels for OA developers to monetize surplus generation, particularly in states with restrictive banking policies.

Q4 2025 IEX green market trends:

- G-DAM volumes: +18% QoQ increase

- G-TAM volumes: -32% QoQ decrease

- Renewable Energy Certificate (REC) volumes: -58% QoQ decrease

G-DAM's growth reflects OA developers using the exchange to sell unbanked surplus energy, particularly in Tamil Nadu and Andhra Pradesh where banking has been curtailed. Adani Green Energy dominated G-DAM sales in 2025, accounting for 38% of traded electricity.

The sharp REC decline signals a structural shift: corporate buyers increasingly prefer direct PPAs or exchange-based green power over traditional REC mechanisms for sustainability reporting.

Emerging alternatives: Virtual PPAs (VPPAs) and International Renewable Energy Certificates (IRECs) are being explored by multinational C&I consumers with global net-zero commitments, though the Ministry of Power is yet to issue formal guidance on VPPA accounting treatment and IREC cross-border recognition under Indian law.

What Is Driving India's Solar Open Access Market in 2026

Several converging forces—cost economics, compliance pressure, technology maturity, and strategic energy security—are driving C&I adoption of solar OA at scale.

Rising Grid Tariffs Create Cost Arbitrage Opportunity

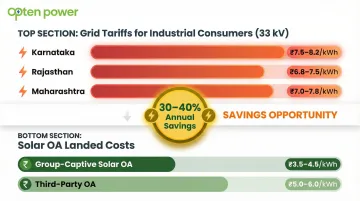

Escalating DISCOM retail tariffs for industrial consumers are the single strongest driver of OA adoption. C&I consumers pay elevated tariffs to cross-subsidise agricultural and residential users. Current grid tariffs for industrial consumers at 33 kV:

- Karnataka: ₹7.5-8.2/kWh

- Rajasthan: ₹6.8-7.5/kWh

- Maharashtra: ₹7.0-7.8/kWh

Solar OA landed costs (including wheeling, CSS where applicable, and transmission) range from ₹3.5-4.5/kWh for group-captive projects and ₹5.0-6.0/kWh for third-party OA. This translates to savings of 30-40% on annual energy costs—the primary economic driver for C&I OA adoption.

Sustainability and ESG Mandates Drive Strategic Procurement

Corporate net-zero commitments, RPO compliance pressure, and ESG ratings from institutional investors are making renewable energy OA a strategic necessity beyond cost reduction.

The numbers reflect urgency: India's C&I renewable OA cumulative capacity reached 18.7 GW by end of FY2024, with annual capacity growing 90.4% YoY. Corporate buyers are no longer treating green procurement as optional—sustainability targets and investor expectations are making it a procurement priority.

Technology Cost Declines and Digital Procurement

Falling solar module prices have improved OA project economics despite volatility from Basic Customs Duty (BCD) and polysilicon price swings. The cost of solar PV projects using Indian-made TOPCon modules fell 3.4% in Q4 2025, though domestic modules remain approximately 40% costlier than Chinese imports due to DCR premiums and ALMM requirements.

Lower module costs alone don't simplify procurement—state-specific regulations, wheeling charges, and developer comparisons still add weeks to deal timelines. Platforms like Opten Power address this directly, offering real-time DISCOM intelligence, automated RFPs, and instant IRR/payback analysis across 16 states so C&I buyers can compare tariffs and ROI from multiple developers and close deals faster.

Land Availability and Grid Connectivity Constraints

Land acquisition challenges and ISTS/InSTS connectivity bottlenecks are slowing project execution despite strong demand. The Central Transmission Utility of India (CTUIL) informed CERC that it faces challenges providing grid connectivity for approximately 60 GW of renewable capacity in Rajasthan, citing saturated conventional evacuation pathways to load centres. This supply-side constraint is a key risk factor for 2026 pipeline realisation.

Competitive Dynamics Among Developers

Large utility-scale IPPs—Adani Green, ReNew, Avaada—are entering the OA market, intensifying competition previously dominated by C&I-focused developers. Adani Green commissioned 408.1 MW of RE projects (including multiple hybrid plants) in Khavda, Gujarat, in September 2025. For C&I buyers, this translates to better tariff competitiveness, stronger project quality, and more financing options as major IPPs compete for long-term PPA volumes.

Future Signals for India's Solar OA Market

While market fundamentals are strong, several developments in the next 1-3 years will determine how quickly India realises its 45+ GW OA pipeline. Regulatory clarity, infrastructure investment, and procurement innovation will be the key differentiators.

Green OA Policy Rollout Across States

Monitor whether high-OA states — Karnataka, Maharashtra, and Rajasthan — align with mandatory banking and 100 kW eligibility provisions. The Electricity Amendment Bill, if passed, would eliminate cross-subsidies paid by manufacturing enterprises within five years and introduce RPO non-compliance penalties of ₹0.35-0.45/kWh. Either outcome reshapes procurement calculus for C&I buyers.

ISTS Charge Reintroduction Timeline

The phased 25% annual charge addition — reaching 100% for projects commissioned from July 2028 — will materially impact interstate OA economics. Developers and C&I consumers will increasingly pivot toward intra-state projects or hybrid configurations to manage transmission costs before that threshold hits.

BESS Economics Reaching a Tipping Point

As states continue restricting banking, co-located storage will cross a commercial viability threshold within 2-3 years. The Ministry of Power approved a second Viability Gap Funding (VGF) tranche of ₹5,400 Crore to support 30 GWh of standalone BESS — and with global BESS costs now at $117-125/kWh, solar-plus-storage is on track to become the standard OA configuration for heavy industries requiring 24x7 power.

C&I buyers who lock in long-term PPAs now, before ISTS charges fully phase in and banking restrictions tighten, retain more negotiating leverage and better project economics than those waiting for regulatory certainty.

Frequently Asked Questions

What is solar open access and how does it work for C&I consumers?

Solar open access allows commercial and industrial consumers to buy solar power directly from generators using the transmission/distribution grid, bypassing DISCOM supply through long-term Power Purchase Agreements (PPAs). Eligibility typically requires contracted demand above 100 kW (Central rule) or 1 MW (many state rules), with three procurement models: third-party OA, captive, and group-captive.

Which states are leading India's solar open access market in 2026?

Karnataka, Maharashtra, and Rajasthan led 2025 additions, accounting for over 60% of installations. Maharashtra, Tamil Nadu, and Gujarat dominated Q4 2025 specifically. OA charge structures, banking provisions, and approval timelines vary by state and directly shape project viability.

Why is the group-captive model the preferred solar open access structure?

Group-captive projects are exempt from Cross-Subsidy Surcharge (CSS) and Additional Surcharge (AS) under the Electricity Act 2003, making landed costs substantially lower than third-party OA. The Supreme Court's 2021 ruling reinforced this exemption, though Haryana and Rajasthan DISCOMs still cause delays through extensive pre-commissioning documentation demands.

How does the expiry of ISTS charge waivers affect solar open access projects in 2026?

Projects commissioned before June 2025 received 25-year ISTS charge waivers. Post-June projects face 25% annual charge addition (75% waiver in FY26, 50% in FY27, 25% in FY28, 0% from July 2028). This raises costs for inter-state OA projects by ₹0.15-0.25/kWh, pushing developers and buyers toward intra-state configurations or hybrid models to reduce transmission exposure.

What are the biggest regulatory challenges for solar open access in India right now?

Three main pain points dominate: state-level banking restrictions (or complete withdrawal in Tamil Nadu and Andhra Pradesh with 15-minute block settlements), inconsistent OA charge structures and approval timelines across states, and ongoing Centre-vs-state friction over Green OA Policy implementation—especially the 100 kW eligibility threshold versus states' 1 MW limits.

How can businesses compare and procure solar open access power efficiently across multiple states?

Navigating 16+ state-specific DISCOM tariffs, OA charges, and regulatory frameworks manually is complex. Opten Power simplifies this with real-time DISCOM intelligence, standardised RFP tools, instant IRR/payback analysis, and live tariff comparisons—so C&I businesses can evaluate project economics and transact across states from a single dashboard.