Introduction

Grid power is unreliable, renewable energy is intermittent, and operating costs keep rising. Standalone solar or wind projects can't deliver the firm, round-the-clock supply that steel plants, cement manufacturers, and data centres need.

Hybrid solar-wind energy storage systems—combining photovoltaic panels, wind turbines, and battery energy storage systems (BESS)—solve this directly by delivering dispatchable, bankable clean power regardless of weather variability.

According to Research Nester, the global hybrid solar wind energy storage market reached $2.4 billion in 2025 and is projected to hit $4.9 billion by 2035, expanding at an 8.3% CAGR. For C&I energy buyers, these trends directly shape procurement strategy, PPA negotiations, and long-term cost competitiveness.

TL;DR

- Hybrid market grows at 8.3% CAGR through 2035, backed by a 93% battery cost reduction and rising C&I demand

- Five 2026 trends: advanced BESS, AI-powered dispatch, hybrid PPAs, policy tailwinds, modular distributed systems

- India's MNRE hybrid policy, RPO mandates, and 500 GW non-fossil target favour hybrid procurement now

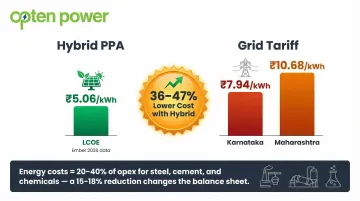

- Hybrid PPAs offer LCOEs as low as ₹5.06/kWh vs. grid tariffs of ₹7.94–₹10.68/kWh

Advanced Battery Energy Storage Is Redefining Hybrid System Performance

Co-locating lithium-ion, flow, and emerging battery chemistries with hybrid solar-wind plants transforms intermittent renewables into dispatchable, grid-quality power. Battery systems capture surplus generation that would otherwise be curtailed, store it, and dispatch it during demand peaks or periods of low renewable output, making the plant bankable for both developers and corporate buyers.

The economics have shifted decisively. IRENA reports that total installed utility-scale BESS costs dropped 93% from $2,571 USD/kWh in 2010 to $192 USD/kWh in 2024. More recently, BloombergNEF documented a 45% year-over-year decline in stationary storage battery pack prices, reaching a record low of $70 USD/kWh in 2025.

These falling costs are directly reflected in India's latest round of storage-coupled tenders:

- SECI FDRE-VII (2025-2026): 1,200 MW of ISTS-connected renewable power with 4,800 MWh assured peak supply (1,200 MW × 4 hours)

- SECI ISTS-XX (2025): 2,000 MW solar PV with 1,000 MW/4,000 MWh energy storage systems

- NTPC (Dec 2024): 500 MW solar capacity requiring 250 MW/1,000 MWh battery storage

These MW-scale tenders demonstrate that storage-coupled hybrid systems are now economically viable at utility and C&I scale, transforming hybrid power from a premium product to a competitive mainstream option.

AI-Powered Controls and IoT Are Optimising Hybrid Dispatch

Smart energy management systems using artificial intelligence, machine learning, and IoT sensors manage solar, wind, and storage dispatch in real time—maximising yield, minimising curtailment, and extending battery cycle life.

Measurable gains from AI-based control:

A 2.5 MW solar PV + BESS agrifood facility in Australia deployed Schneider Electric's EcoStruxure Microgrid Advisor, an AI-driven energy management platform. Results:

- 21.6% annual electricity cost reduction

- 328.6 tCO₂e emissions reduction

- Optimised battery cycling to maximise arbitrage revenues

Siemens Energy's Omnivise Hybrid Control platform integrates wind, solar, storage, and hydrogen into a single dispatch framework, delivering single-digit percentage increases in efficiency and generation output by coordinating multi-source assets algorithmically.

For C&I buyers—particularly industries managing high 24x7 loads under Open Access—AI-driven dispatch reduces dependence on grid backup, extends battery lifespan through intelligent charge-discharge cycles, and unlocks participation in ancillary services markets. In markets with DISCOM grid volatility, that translates directly to lower effective tariffs and higher supply reliability.

Commercial and Industrial Buyers Are Becoming the Dominant Adopters

Large C&I users—steel plants, cement manufacturers, data centres, hospitals, and IT parks—are shifting procurement strategies toward hybrid renewable PPAs to achieve 24×7 clean power supply at predictable costs. Standalone solar or wind simply cannot satisfy round-the-clock load profiles on their own.

Why hybrid PPAs appeal to heavy industry:

- Firm generation profiles reduce exposure to grid tariff hikes (which averaged ₹7.94/kWh in Karnataka and ₹10.68/kWh in Maharashtra for large industrial users in 2024-25)

- RPO compliance becomes simpler — hybrid systems meet multiple Renewable Purchase Obligation sub-targets under a single contract

- Net-zero commitments require consistent, verifiable clean power, not intermittent renewables that rely on grid backup

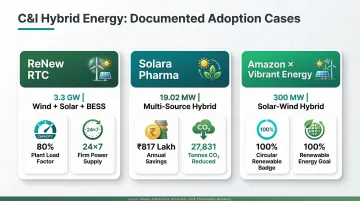

Documented C&I Adoption Cases

- ReNew RTC Project: 3.3 GW wind + solar + 100 MWh BESS achieving an 80% plant load factor, providing 24×7 firm dispatchable power to SECI

- Solara Active Pharma: 19.02 MW multi-source hybrid system (wind + solar + hydro) delivering 36% renewable energy penetration, ₹817 lakh annual electricity cost savings, and 27,831 tonnes/annum carbon reduction

- Amazon (via Vibrant Energy): 300 MW solar-wind hybrid PPA supporting the company's 100% renewable energy goal

These cases share a common thread: procurement complexity. Evaluating tariffs, IRR, and payback across multiple developers — at speed — remains the bottleneck for most C&I buyers. Platforms like Opten Power address this directly, cutting what was once a months-long procurement process down to hours through standardised pricing intelligence across 16 states.

Policy Tailwinds and Grid Modernisation Are Unlocking Market Scale

India's Regulatory Environment

India's Ministry of New and Renewable Energy (MNRE) hybrid renewable energy policy defines a hybrid plant as one where the rated power capacity of one resource is at least 25% of the other. It allows hybrid power to fulfil both solar and non-solar RPO obligations simultaneously.

The government has also granted must-run status to hybrid plants, shielding them from curtailment under merit order dispatch. This directly reduces revenue risk for developers and makes hybrid projects easier to finance.

India's national target of 500 GW non-fossil capacity by 2030 creates structural demand for hybrid projects capable of delivering firm power, not just installed capacity.

Global Parallels

India isn't moving in isolation. Comparable policy frameworks are compressing development timelines and unlocking capital across major markets:

- EU Fit for 55 framework: RED III mandates a 6-month maximum permit-granting procedure for co-located energy storage in designated renewables acceleration areas

- US Inflation Reduction Act (IRA): Final rules (Dec 2024) clarify that Section 48 Investment Tax Credit (ITC) applies to energy storage co-located with and sharing power conditioning equipment with qualified renewable facilities

- Asian Development Bank: Provided a $331 million finance package for ReNew's 837 MW wind-solar + 415 MWh BESS plant in India

Significance for the industry:

Taken together, these frameworks resolve the two issues that most often stalled hybrid deals: ambiguity over ITC and curtailment exposure. With both addressed, developers can structure bankable PPAs with greater confidence, and C&I buyers gain access to a wider pool of firm-power offtake options.

Modular and Distributed Hybrid Systems Are Lowering Entry Barriers

Manufacturers and developers now offer scalable, modular hybrid architectures—from 100 kW commercial installations to multi-hundred MW utility-scale plants—that can be deployed rapidly and expanded incrementally, reducing upfront capital commitment.

Emerging sub-formats:

- Mining microgrids: Australia's Agnew Gold Mine operates a 56 MW hybrid renewable microgrid (18 MW wind, 4 MW solar, 13 MW battery, 16 MW gas), delivering over 50% renewable energy and abating 46,400 tonnes of CO₂ annually

- Floating hybrid installations: Landatu Solar deployed a modular floating solar pilot at the Port of Bilbao to test sea-adapted PV scale-up

- Rooftop solar + small wind units: Startups like Aeromine are designing motionless mini wind turbines for commercial rooftops, occupying only 10% of roof space alongside solar panels

These formats share a common logic: deploy what you need now, expand as demand grows.

Why this matters:

Modularity opens hybrid renewable adoption to medium-to-large enterprises, warehouses, and process industries that previously lacked the scale to justify a dedicated energy project. For remote industrial operations—mining, agriculture, telecom—off-grid hybrid systems offer a practical path out of grid unreliability and diesel dependency.

In India, where grid access remains inconsistent across industrial corridors and remote sites, this shift is especially relevant. Businesses can now right-size a hybrid system to their actual load profile rather than waiting for a large-scale project to pencil out.

What's Driving These Hybrid Solar Wind Energy Storage Market Trends

Five distinct forces are pushing India's hybrid renewable market into a new growth phase in 2026 — and they're all reinforcing each other. The global market is projected to expand at 8.3% CAGR through 2035, driven by:

Technology Advances

The dramatic cost reduction in solar PV modules, wind turbines, and lithium-ion batteries—combined with mature AI-based energy management software—has lowered the LCOE of hybrid systems to levels that compete directly with grid tariffs in most Indian states.

Ember reports that India's solar+battery LCOE reached ₹5.06/kWh ($56/MWh) in 2026, significantly undercutting average large industrial tariffs of ₹7.94/kWh in Karnataka and ₹10.68/kWh in Maharashtra.

Market Demand and C&I Expectations

Heavy industries with 24×7 operations face rising grid tariffs, carbon disclosure requirements, and board-level pressure to demonstrate sustainability. Hybrid renewable systems address all three pressures with a single contract, shifting them from a cost-reduction tool to a core procurement strategy.

Cost Pressures and Efficiency Needs

For energy-intensive industries — steel, cement, chemicals — energy costs represent 20–40% of operating expenses. In cement specifically, fuel and power account for 30–35% of total costs, and a higher renewable share can cut those bills by 15–18%.

A hybrid PPA that locks in below-grid tariff rates for 15–25 years is a straightforward balance-sheet decision.

Regulatory and Compliance Influences

India's RPO obligations, proposed carbon tax frameworks, and international ESG reporting standards (BRSR, CSRD for export-oriented industries) are making renewable procurement a compliance necessity, not just a CSR initiative. Key compliance drivers include:

- RPO mandates requiring minimum renewable energy consumption percentages

- BRSR and CSRD reporting tying procurement decisions to disclosed emissions data

- Proposed carbon tax frameworks that will price fossil-heavy energy use

Hybrid systems let C&I buyers tick all three boxes with a single procurement contract.

Competitive Dynamics

Renewable developers are increasingly differentiating through hybrid+storage configurations that guarantee capacity factors and generation profiles no standalone asset can match. The result: tighter competition on generation guarantees, uptime commitments, and delivered tariff rates — not just headline pricing.

How These Trends Are Impacting the Renewable Energy Industry

The convergence of these five trends is producing measurable, structural changes across operations, business models, and talent requirements throughout the renewable energy value chain.

Operational Impact

Hybrid+storage plants are now being designed to guarantee generation profiles on an hourly or block basis, fundamentally changing how renewable capacity is contracted, metered, and settled with DISCOMs. ReNew's RTC project, for example, achieves an 80% plant load factor—a metric that would be impossible with standalone solar or wind assets. This shift from intermittent to firm renewable delivery changes procurement fundamentally.

Business Impact

Developers, IPPs, and project financiers are restructuring their go-to-market models around hybrid PPAs, creating new revenue streams from capacity firming, ancillary services, and demand charge reduction products.

Platforms like Opten Power's automated RFP engine and pre-approved contract framework let C&I buyers access these hybrid supply structures up to 50% faster than traditional procurement routes — directly accelerating market adoption.

Workforce Impact

The industry now requires professionals who can bridge power electronics, battery management, AI-based dispatch, and regulatory navigation. Demand is rising fastest for:

- Hybrid system engineers with multi-source integration experience

- Energy data analysts focused on dispatch optimization

- Procurement specialists familiar with complex renewable contracting

Companies that invest in building this expertise now will be better positioned to execute as hybrid project pipelines accelerate through 2026.

Future Signals for the Hybrid Solar Wind Energy Storage Market

The market will continue to evolve rapidly. The next 1–3 years (2026–2028) will be shaped by three emerging signals:

- Long-duration storage reaching pilot-scale commercial deployments

- Green hydrogen co-generation absorbing surplus hybrid output

- Commoditisation of hybrid PPAs through standardised procurement platforms

Long-duration storage technologies — vanadium flow batteries, iron-air batteries, and compressed air energy storage — are crossing from R&D into commercial deployment. In November 2025, NTPC commissioned India's first MWh-scale vanadium redox flow battery project (3 MWh / 0.5 MW × 6 hours) at its NETRA R&D centre.

NTPC Renewable Energy has since issued an EPC tender for a 100 MWh VRFB system at the Khavda hybrid park in Gujarat — signalling that pilot-scale hybrid + long-duration projects will be operational by 2027.

Green hydrogen co-generation is emerging as a growing use case for surplus hybrid output, converting excess solar-wind generation into hydrogen for industrial feedstock or backup fuel. Adani New Industries commissioned India's first off-grid 5 MW green hydrogen pilot in Kutch, Gujarat. ACME Cleantech Solutions won India's first green ammonia auction under the SIGHT Scheme — 75,000 MTPA at a record low tariff of ₹55.75/kg.

MNRE's green hydrogen mission targets and auction pipeline serve as the clearest leading indicators for where this segment heads next.

Together, these signals point toward a broader structural shift in how hybrid power is bought and sold.

Scenario for 2026–2028: Hybrid renewable energy is expected to move from a premium, custom procurement product to a standardised offering — with templated PPAs, platform-based tariff discovery, and real-time DISCOM intelligence enabling C&I buyers to procure hybrid power as efficiently as they currently procure grid power.

Conclusion

Hybrid solar-wind energy storage has moved from pilot-phase curiosity to the default procurement architecture for industrial and commercial buyers who need 24×7 clean power at competitive cost. The five trends covered here are already restructuring project pipelines, tariff frameworks, and energy procurement strategies across India in 2026.

The window to lock in favorable hybrid PPA terms is narrowing as demand climbs and developers reprice accordingly. Businesses that act now—comparing tariffs, vetting developer capabilities, and shortlisting storage configurations—will secure long-term cost advantages that latecomers will pay a premium to access.

Key actions for C&I buyers evaluating hybrid projects in 2026:

- Map your load profile against hybrid generation curves to quantify round-the-clock coverage

- Compare landed tariffs across states using live Discom data, not historical benchmarks

- Evaluate developer track records on hybrid-specific projects, not just solar or wind alone

- Run IRR and payback scenarios across multiple PPA structures before shortlisting

Platforms like Opten Power give commercial and industrial buyers direct access to 4+ GW of solar, wind, and hybrid capacity across 16 states—with real-time tariff intelligence and automated RFP tools to accelerate the evaluation process.

Frequently Asked Questions

What is a hybrid solar-wind energy storage system?

A hybrid solar-wind energy storage system combines photovoltaic panels, wind turbines, and battery storage to deliver continuous clean power. Each source complements the other: solar peaks during daylight hours, wind often peaks at night or during monsoons, and storage maintains continuous supply across any gap.

How large is the hybrid solar-wind energy storage market in 2026 and where is it headed?

The global hybrid solar wind energy storage market was valued at $2.4 billion in 2025 and is projected to reach $4.9 billion by 2035, expanding at an 8.3% CAGR. Asia-Pacific—led by India and China—accounts for approximately 40% of global installations.

Why are C&I businesses choosing hybrid renewable systems over standalone solar or wind?

Hybrid systems solve the intermittency problem, delivering a consistent generation profile suited to 24×7 industrial loads. They also offer lower effective tariffs (₹5.06/kWh for solar and battery) compared to grid power (₹7.94–₹10.68/kWh) over a 15–25 year PPA horizon.

What role does battery storage play in a hybrid solar-wind project?

Batteries capture surplus generation from solar or wind that would otherwise be curtailed, store it, and dispatch it during demand peaks or periods of low renewable output. This makes the plant dispatchable, enabling capacity guarantees that improve project bankability (lender confidence in the project).

What are the main challenges in deploying hybrid solar-wind energy storage projects?

Three barriers stand out for most project developers:

- Higher upfront capital compared to standalone solar or wind systems

- Complex multi-source design and control integration

- Grid and DISCOM infrastructure requirements for variable hybrid output

Falling technology costs and improving policy frameworks are steadily reducing all three.

How does India's policy framework support hybrid solar-wind energy storage adoption?

Several policy levers work together to de-risk hybrid projects. MNRE's hybrid policy grants must-run status to hybrid plants, RPO sub-targets let hybrid power meet both solar and non-solar obligations, and India's 500 GW non-fossil capacity target sustains long-term financing interest.