Introduction

India's electricity demand grew 4.17% to reach 1,693.9 billion units (BU) in FY2025, with peak demand hitting 249.85 GW. Projections for FY2026 indicate continued acceleration, with the Central Electricity Authority forecasting demand to reach 277.2 GW—potentially climbing as high as 296 GW. This surging trajectory raises a critical question: how can utilities and commercial & industrial (C&I) buyers secure reliable, cost-effective power over the next two to three decades?

The answer lies increasingly in long-term Power Purchase Agreements (PPAs): multi-decade contracts that lock in tariffs, ensure capacity availability, and provide the revenue certainty needed to finance new generation projects. India's PPA market is shifting fast. Thermal PPAs have returned after nearly a decade of dormancy, renewable PPAs are breaking tariff records, and DISCOM financial health remains a persistent risk factor affecting contract sanctity.

This article examines the current state of India's long-term PPA market, the forces driving renewed contracting activity, the risks that continue to challenge bankability, and what C&I buyers must evaluate before committing to multi-decade energy agreements.

TLDR:

- Long-term PPAs (20-25 years) are critical for financing India's power capacity additions amid 4%+ annual demand growth

- Thermal PPAs have returned at ₹5.30-5.45/kWh while renewable PPAs now clear below ₹2.60/kWh

- DISCOM accumulated losses of ₹6.47 lakh crore create ongoing payment and contract sanctity risks

- C&I buyers can use platforms like Opten Power to compare 4+ GW of renewable capacity across 16 states

What Is a Long-Term PPA and How Does It Work in India?

A long-term PPA is a legally binding contract between a power generator and a buyer, typically spanning 20–25 years for utility-scale projects and 10–25 years for corporate/C&I agreements. These contracts form the backbone of India's independent power ecosystem by providing developers with the revenue certainty needed to secure project financing.

Contract Structure: Long-term PPAs typically include:

- Fixed charges covering debt servicing, return on equity, and fixed operating costs

- Variable charges (in thermal PPAs) that pass through fuel costs to buyers

- Defined payment security mechanisms (Letters of Credit, escrow accounts)

- Change-in-law provisions protecting both parties from regulatory shifts

- Termination clauses specifying default conditions and exit payments

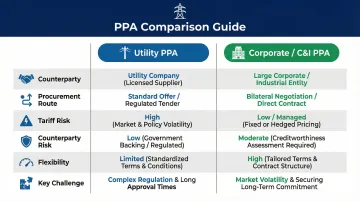

Two Primary PPA Categories in India

| Utility PPAs | Corporate / C&I PPAs | |

|---|---|---|

| Counterparty | DISCOMs (distribution companies) | Industrial or commercial buyers via open access |

| Procurement Route | Competitive bidding through SECI or state agencies | Direct negotiation |

| Tariff Risk | Lower | Moderate |

| Counterparty Risk | Higher — tied to DISCOM financial health | Lower for creditworthy C&I buyers |

| Flexibility | Limited | Higher — buyer controls energy mix and pricing |

| Key Challenge | DISCOM payment delays | State-specific open access charges and regulations |

The Bankability Factor

Whichever PPA category a developer pursues, lenders scrutinize the same fundamentals before a project can achieve financial close. Per IREDA and Power Finance Corporation lending norms, bankability depends on:

- Robust payment security mechanisms (Trust and Retention Accounts, DSRA creation)

- Confirmation from DISCOMs to deposit payments into designated escrow accounts

- The creditworthiness of the offtaker—whether DISCOM or C&I buyer

- Unconditional, irrevocable Letters of Credit maintained throughout the contract term

Offtaker creditworthiness ultimately determines project viability. A PPA with a financially distressed DISCOM can stall financing regardless of the tariff, while a well-structured C&I agreement backed by a creditworthy buyer routinely reaches financial close faster—sometimes within weeks.

India's Long-Term PPA Market: Where Things Stand Today

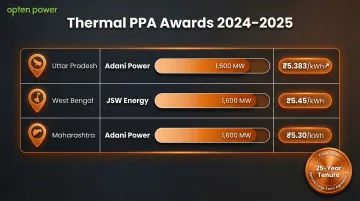

The Thermal PPA Revival

After nearly a decade of minimal thermal contracting activity, state utilities have returned to long-term coal-based PPAs in 2024-2025:

| State | Developer | Capacity | Tariff (₹/kWh) | Term |

|---|---|---|---|---|

| Uttar Pradesh | Adani Power | 1,500 MW (ultra-supercritical, Mirzapur) | 5.383 (Fixed: 3.727 + Fuel: 1.656) | 25 years |

| West Bengal | JSW Energy | 1,600 MW (greenfield, Salboni) | 5.45 | 25 years |

| Maharashtra | Adani Power | 1,600 MW (commencing FY2030-31) | 5.30 | Long-term |

These awards reflect a deliberate strategy: as renewable penetration deepens, states are contracting firm baseload capacity to cover intermittency gaps — and thermal remains the instrument of choice for continuous supply reliability. That calculus sits alongside, not against, the renewable build-out happening in parallel.

Renewable PPA Momentum

Renewable long-term PPAs continue to dominate new capacity additions. India's total installed renewable capacity (solar, wind, hydro) reached 212 GW as of January 2026, with Bridge to India reporting a pipeline of 132.56 GW under development — including 32.19 GW in the C&I segment alone.

Recent SECI auctions have discovered highly competitive tariffs:

- ₹2.57/kWh for 1,500 MW ISTS-connected solar (Tranche XIV)

- ₹3.43/kWh for 1,200 MW wind-solar hybrid (Tranche VIII)

Corporate PPAs from C&I buyers are growing rapidly as a share of total renewable contracting, driven by cost savings, ESG commitments, and the need to hedge against volatile short-term power exchange tariffs.

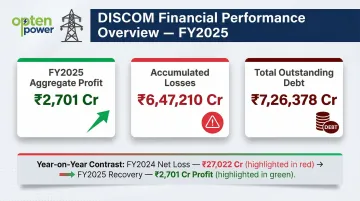

DISCOM Financial Health: The Defining Structural Tension

DISCOM finances show mixed signals. According to PFC's 'Performance of Power Utilities 2024-25' report:

- Aggregate DISCOMs posted a profit of ₹2,701 crore in FY2025 (recovering from a ₹27,022 crore loss in FY2024)

- Yet accumulated losses remain staggering at ₹6,47,210 crore

- Total outstanding debt stands at ₹7,26,378 crore

These numbers tell two different stories depending on where you look. States with stronger DISCOM creditworthiness — Gujarat, Maharashtra, Karnataka — attract consistent developer interest. States with chronic payment delays (Punjab, Rajasthan, Uttar Pradesh historically) create persistent counterparty risk that prices into every long-term PPA negotiation.

State-Wise Variation in PPA Activity

Most Active States:

- Maharashtra: Consistent PPA awards, strong regulatory framework; MERC permits simultaneous net-metering and open access

- Gujarat: Developer-friendly policies backed by reliable payment discipline and healthy DISCOM finances

- Karnataka: Large C&I market with strong demand, though recent GEOA rule changes have introduced some regulatory uncertainty

For C&I buyers and developers alike, state selection is as consequential as tariff discovery — creditworthiness and regulatory predictability determine whether a 25-year PPA delivers on paper or in practice.

What's Driving the Long-Term PPA Surge

Policy-Mandated Renewable Procurement

India's national target of 500 GW non-fossil capacity by 2030 creates structural, policy-mandated demand for long-term renewable PPAs. The Ministry of Power's October 2023 notification escalates Renewable Purchase Obligation (RPO) requirements to 43.33% of total energy by FY2029-30—comprising solar, wind, hydro, and distributed RE.

Both central and state agencies must procure specified RPO volumes, driving consistent long-term PPA tendering activity regardless of short-term market conditions.

C&I Demand for Cost Certainty and ESG Compliance

Large energy-intensive industries—steel, cement, data centres, EV charging infrastructure, green hydrogen production—are turning to long-term PPAs to achieve:

- Fixed tariffs that insulate buyers from volatile short-term power exchange pricing

- Verifiable carbon reduction credentials for ESG reporting and compliance

- Guaranteed power supply supporting 24x7 manufacturing operations

The numbers make the case clearly. The Indian Energy Exchange (IEX) Day-Ahead Market averaged ₹4.47/kWh in FY2025, swinging from ₹3.30/kWh to over ₹5.20/kWh depending on seasonal demand. Long-term renewable PPAs, by contrast, lock in fixed pricing below ₹3/kWh—a meaningful cost advantage that compounds over a 20-25 year contract horizon.

Grid Balancing and Baseload Requirements

As renewable penetration rises, thermal baseload PPAs are being re-contracted to ensure round-the-clock reliability and support renewable integration. States recognize that intermittent solar and wind generation requires firm, dispatchable capacity to maintain grid stability—explaining why thermal PPAs are returning despite the energy transition push.

Falling Renewable Tariffs Create Lock-In Incentives

Locking in today's renewable tariff rates through a long-term PPA provides economic protection against future tariff escalation. With solar tariffs now clearing below ₹2.60/kWh and hybrid projects at ₹3.43/kWh, buyers who commit now secure these historically low rates for 20-25 years. Any future tariff movement—driven by land costs, financing rates, or policy changes—will not affect contracted buyers.

Key Risks and Challenges in the Long-Term PPA Market

PPA Sanctity Violations

The most serious structural risk facing India's long-term PPA market is unilateral contract modification or termination by state governments or DISCOMs.

Andhra Pradesh (2019-2020): The AP government attempted to retroactively renegotiate tariffs for over 7 GW of operational wind and solar PPAs, citing DISCOM financial distress. The move caused severe market uncertainty until the AP High Court and APTEL ruled that competitively bid PPAs cannot be unilaterally renegotiated.

Punjab (2025-2026): PSPCL faced default issues with unpaid dues reaching ₹2,582 crore. The Punjab and Haryana High Court issued notices and barred alienation of PSPCL properties due to massive outstanding payments to generators.

These incidents push developers and investors to demand higher risk premiums for long-term PPAs — particularly in states with weak DISCOM governance or political instability.

Regulatory Interference Risk

Third parties such as load dispatch centres and state electricity regulatory commissions have been drawn into PPA enforcement disputes, undermining the principle that only contracting parties should modify or enforce agreements. When regulators intervene to reduce tariffs or alter payment terms post-facto, it erodes the legal sanctity that makes long-term PPAs bankable.

Payment Security Problems

Inconsistent Letter of Credit (LC) maintenance by DISCOMs leaves generators exposed to delayed or unpredictable revenue. The Electricity (Late Payment Surcharge and Related Matters) Rules, 2022 introduced stronger payment discipline, but enforcement varies significantly by state. Key provisions include:

- Legacy dues restructured into EMIs to reduce one-time default risk

- Defaulting DISCOMs barred from purchasing power through exchanges

- Late payment surcharges applicable to outstanding generator dues

Duration and Technology Mismatch Risk

25-year PPA tenures locked in at today's technology costs may become economically unviable as energy storage, hybrid projects, and next-generation solar become cheaper. Some stakeholders now advocate for shorter-duration contract structures (10-15 years) or periodic tariff reset mechanisms to accommodate technology evolution—though this introduces refinancing risk for developers.

Thermal vs. Renewable Long-Term PPAs: A Comparative View

Tariff Levels and Total Cost of Supply

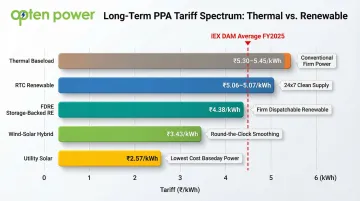

Thermal PPAs: Recent 25-year awards clear at ₹5.30–5.45/kWh, providing firm, dispatchable baseload power.

Renewable PPAs: Utility-scale solar clears at ₹2.56–2.57/kWh, wind-solar hybrids at ₹3.43/kWh.

However, total cost of supply must factor in transmission charges, RPO compliance benefits, and storage costs for round-the-clock renewable supply. When these are included, the gap narrows—especially as Round-the-Clock (RTC) renewable PPAs mature.

Use Case Logic

Thermal PPAs suit baseload-dependent industries requiring 24×7 despatchable power—steel, cement, and process industries—where reliability outweighs tariff optimization.

Renewable PPAs (especially hybrid and storage-linked) are increasingly viable for the same segments given falling costs. SECI's RTC-IV auction (1,200 MW) discovered tariffs of ₹5.06–5.07/kWh—competitive with thermal while delivering ESG benefits.

Firm and Dispatchable RE (FDRE) tenders mandate demand-following power delivery using energy storage systems. SJVN's (Satluj Jal Vidyut Nigam) 1,500 MW FDRE tender cleared at ₹4.38/kWh—positioning storage-backed renewables as a direct substitute for coal-based baseload.

Regulatory Treatment Differences

Beyond cost and reliability, the two PPA types carry distinct compliance implications that increasingly tilt long-term decisions toward renewables.

Renewable PPAs deliver RPO compliance credit for buyers and align with ESG mandates—adding regulatory and reputational value beyond cost savings.

Thermal PPAs offer reliability but carry growing transition risk on two fronts:

- India's compliance carbon market is expected to begin trading in mid-2026, introducing future carbon pricing exposure for coal-linked assets

- Stricter SO₂ emission norms require FGD installation for Category A and B thermal plants, raising long-term CAPEX commitments

What C&I Buyers Should Consider Before Signing a Long-Term PPA

Due Diligence Checklist

Before committing to a 10-25 year energy agreement, C&I buyers must evaluate:

- Verify the generator's financial health, project financing structure, and operational track record

- Confirm annual escalation rates (typically 2-3% for renewable PPAs) and model their long-term cost impact

- Check how the contract allocates regulatory changes — open access charges, RPO rules, GST — between parties

- Define force majeure terms precisely: which events qualify, how they affect payments, and contract duration

- Understand early termination costs for both buyer default and generator default scenarios

- Confirm lender approval of PPA terms — third-party sign-off signals contract robustness

Make-or-Buy Decision: Direct PPA vs. DISCOM Procurement

Direct Open Access Corporate PPA makes sense when:

- Your consumption exceeds 100 kW (post-GEOA Rules 2022)

- Current grid tariffs are high (₹10-15/unit)

- State open access charges (wheeling, cross-subsidy surcharge, banking) are reasonable

- You have internal capacity to manage regulatory compliance

DISCOM or Third-Party Aggregator Procurement is preferable when:

- Consumption is below open access thresholds

- State open access charges are prohibitively high

- You prefer operational simplicity over tariff optimization

- Your credit profile may not support direct developer contracting

Which path you choose depends heavily on your state's open access rules — and those vary considerably.

State-Level Open Access Landscape:

- Karnataka: New 2025 regulations restrict banking to monthly cycles after High Court struck down central GEOA rules

- Tamil Nadu: 8% in-kind banking charge, 15-minute block settlements, monthly banking cycle

- Maharashtra: Allows simultaneous net-metering and open access but imposes Time-of-Day slot restrictions

How Platforms Like Opten Power Simplify Long-Term PPA Procurement

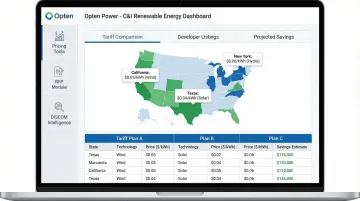

Opten Power gives C&I buyers access to 4+ GW of renewable capacity from verified developers across 16 states, with tools to compare tariffs, IRR, and projected savings in one place. The platform covers:

- Real-time pricing comparison: Analyze costs, savings, and ROI from multiple developers simultaneously — no back-and-forth with brokers

- Automated RFP tools: Build, distribute, and evaluate bids using modular templates, cutting deal closure time by 50%

- Pre-approved PPA contracts: Standardized templates across Capex, Group-Capex, and Third-Party Open Access models reduce legal friction

- DISCOM intelligence: Standardized, state-updated landing prices across all 16 states so buyers see true costs before committing

For C&I buyers navigating bilateral negotiations or broker-led procurement alone, this kind of structured visibility typically takes months to assemble manually.

Frequently Asked Questions

What is the typical tenure of a long-term PPA in India?

Utility PPAs are typically 25 years (the standard SECI template duration), while corporate/C&I PPAs range from 10-25 years. Newer structures are exploring shorter 5-10 year durations to accommodate technology evolution and reduce lock-in risk.

What is the difference between a utility PPA and a corporate PPA in India?

Utility PPAs are contracted between generators and DISCOMs for grid supply through competitive bidding. Corporate PPAs are direct contracts with industrial or commercial buyers via open access, offering more flexibility and often better pricing but requiring navigation of state-level open access regulations.

How are long-term PPA tariffs determined in India?

Tariffs are discovered through competitive bidding processes managed by SECI or state agencies. Renewable PPAs typically have fixed tariffs with modest annual escalation (2-3%), while thermal PPAs separate fixed charges from variable fuel charges that are passed through to buyers.

What are the biggest risks for C&I buyers in a long-term PPA?

Key risks include:

- Generator default and change-in-law exposure on open access charges

- Technology lock-in over long tenures

- State-level regulatory volatility (banking charges, wheeling fees) inflating landed costs

- Weak termination or payment security clauses

Can a long-term PPA be terminated early in India?

Early termination is permitted under defined default or force majeure events, with pre-agreed termination payments protecting lenders. Notably, the Supreme Court's 2021 Gujarat Urja ruling allows NCLT to stay PPA termination during insolvency proceedings if insolvency is the sole termination ground.

How do renewable long-term PPAs compare to thermal long-term PPAs for industrial buyers?

Renewable PPAs offer lower, stable tariffs (₹2.56-3.43/kWh) with ESG benefits, while thermal PPAs (₹5.30-5.45/kWh) deliver round-the-clock despatchability. Hybrid and RTC renewable structures (₹5.06-5.07/kWh) now close that gap for energy-intensive industries requiring 24x7 supply.