Introduction

Indian businesses — from steel plants and data centres to manufacturing units and IT parks — collectively consume over half the country's electricity, yet most still procure energy reactively, treating it as a fixed utility expense rather than a strategic lever. The industrial sector alone accounts for 42% of India's total electricity consumption, while commercial users add another 8%. For heavy industries, energy represents a massive cost driver; in cement manufacturing, logistics, power, and fuel account for more than 60% of production costs.

The problem? Most businesses still rely on passive procurement — accepting whatever tariff their state distribution company (DISCOM) charges, renewing contracts annually without benchmarking alternatives, and leaving significant savings uncaptured. With DISCOM industrial tariffs ranging between ₹6-8 per unit across states and rising due to increasing power purchase costs, this reactive approach is becoming unsustainable.

The B2B energy procurement landscape in India is undergoing a structural shift — driven by falling renewable costs, policy evolution, and digital disruption. This article covers four trends redefining how commercial and industrial buyers source, structure, and manage energy: the rise of corporate PPAs, real-time market intelligence, automated procurement tools, and portfolio-level energy management.

Key Takeaways

- B2B energy procurement is shifting from reactive annual renewals to proactive, tech-enabled strategic sourcing

- Corporate PPAs give energy-intensive industries direct access to renewable capacity with predictable, long-term pricing

- ESG mandates are now core procurement criteria, driven by BRSR reporting and global carbon regulations

- Digital platforms and real-time market intelligence replace opaque broker-led negotiations

- Companies that act on these trends now lock in lower energy costs and reduce regulatory exposure before competitors do

Trend 1: The Shift Toward Long-Term Corporate Power Purchase Agreements (PPAs)

Why Energy-Intensive Industries Are Bypassing the Spot Market

Energy-intensive sectors — cement, steel, textiles, chemicals — are increasingly signing long-term bilateral PPAs directly with renewable developers, typically spanning 10–25 years. These contracts lock in predictable, below-grid tariffs while bypassing volatile spot markets and unreliable DISCOM supply.

India's C&I open access market achieved a 46% compound annual growth rate from FY2022 to FY2024, reaching 18.7 GW of cumulative capacity. In 2024 alone, India added 6.9 GW of solar open access — a 77% year-over-year increase.

Group Captive Models Deliver 25-30% Cost Savings

The group captive model has emerged as the preferred PPA structure for C&I buyers. Key financial advantages over on-grid tariffs include:

- 25–30% lower landed costs compared to grid supply

- Complete exemption from Cross-Subsidy Surcharges (CSS) and Additional Surcharges (AS)

- Net open access charges of ₹2–3.5 per unit across India's top ten C&I states

Third-party open access remains viable but attracts heavier CSS and AS penalties. For businesses able to structure group captive arrangements, the cost gap is substantial.

Heavy Industries Lead the PPA Charge

Those savings are driving concrete action. Major industrials are moving aggressively:

- JSW Energy signed 1,325 MW of renewable PPAs, including a 1,025 MW wind PPA with SECI at ₹3.62/kWh and a 300 MW solar PPA at ₹2.66/kWh

- Tata Steel executed a fixed-tariff long-term agreement to source 379 MW of captive renewable power

Deals at this scale signal a structural shift: locking in fixed tariffs for 10–25 years hedges against grid price volatility while advancing decarbonisation targets simultaneously.

Trend 2: Digital Platforms and Marketplace-Driven Procurement Are Replacing Opaque Broker Models

The End of Fragmented, Broker-Dependent Sourcing

Traditional renewable energy procurement involved fragmented broker networks, limited visibility into available projects, and weeks-long negotiations with individual developers. Procurement teams had no standardized way to compare tariffs, assess project quality, or benchmark offers across states.

Digital energy marketplaces are changing this. Businesses can now access pre-screened project listings, compare real-time DISCOM-level landing prices across states, run automated RFPs, and get instant financial analysis — all on a single platform.

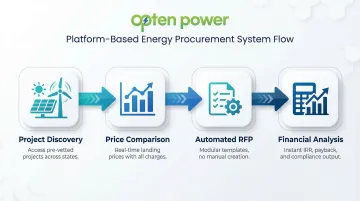

How Platform-Based Procurement Works in Practice

Modern procurement platforms enable businesses to:

- Discover pre-vetted solar, wind, and hybrid projects across multiple states

- Compare real-time landing prices that include wheeling, banking, and cross-subsidy charges

- Run automated RFPs using modular templates — no manual document creation needed

- Receive instant IRR, payback period, and regulatory compliance analysis

Organizations using AI-assisted procurement tools report 25-40% increases in procurement efficiency, with AI reducing transactional sourcing time by 30-50%.

Government Infrastructure Supports Digital Shift

These platform capabilities don't exist in isolation — regulatory infrastructure is actively supporting the shift. The Green Energy Open Access Registry (GOAR) portal acts as a single-window platform for open-access registration. By December 2024, over 37,558 applications for GEOA had been approved, representing 19,892 million units of electrical energy.

Platforms like Opten Power are purpose-built for this environment. With access to 4+ GW of solar, wind, and hybrid projects across 16 states, real-time DISCOM intelligence, and an automated tender engine, they give procurement teams full visibility and control — and cut deal timelines by up to 50%.

Trend 3: ESG and Sustainability Mandates Are Becoming Core Procurement Criteria

Sustainability Is No Longer Optional for Large Industrials

Regulatory pressure, investor scrutiny, and export market requirements have made green energy sourcing a procurement prerequisite — not a differentiator — for large industrials. Three frameworks are driving this urgency:

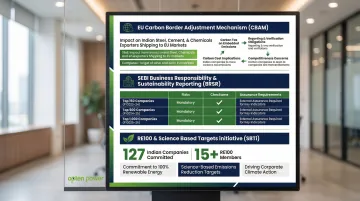

EU Carbon Border Adjustment Mechanism (CBAM): Indian exporters in steel, cement, and chemicals now face the EU's carbon border tax on emissions embedded in production. Procuring certified green energy isn't optional — it's a condition of EU market access.

SEBI BRSR Reporting: The Securities and Exchange Board of India mandated Business Responsibility and Sustainability Reporting (BRSR) for the top 1,000 listed companies starting FY 2022-23. The phased rollout of BRSR Core assurance forces companies to rigorously audit Scope 2 emissions:

| Financial Year | Applicability | Requirement |

|---|---|---|

| FY 2023-24 | Top 150 listed entities | Reasonable assurance of BRSR Core |

| FY 2024-25 | Top 500 listed entities | Reasonable assurance of BRSR Core |

| FY 2025-26 | Top 1,000 listed entities | Reasonable assurance of BRSR Core |

RE100 and Corporate Net-Zero Targets: With 127 Indian companies committed to SBTi net-zero targets, India ranks sixth globally. More than 15 India-headquartered firms are RE100 members, while over 200 international RE100 members operate here — sourcing 39% of their India electricity from renewables. Suppliers in their value chains face mounting pressure to match that standard.

REC Market Growth Reflects Rising Compliance Demand

REC transaction volumes tell the story clearly. In 2023-24, 138.53 lakh RECs were transacted — a near 4.5x jump from 26.32 lakhs the prior year. Clearing prices fell from ₹1,000/MWh to ₹442/MWh over the same period.

For procurement teams, that price drop signals an opportunity: compliance supply is scaling, but locking in long-term green power through PPAs remains more cost-stable than relying on spot REC purchases.

Trend 4: Data-Driven Decision-Making and Real-Time Market Intelligence

From Annual Reviews to Continuous Intelligence-Led Sourcing

Procurement teams are shifting from reactive annual reviews to continuous, data-driven sourcing. Real-time market data, AI-assisted tools, and digital dashboards enable teams to monitor tariff movements, benchmark offers from multiple suppliers, and time procurement decisions strategically.

Real-Time Visibility Into True Landed Costs

State-wise DISCOM tariffs, open access charges, wheeling and banking charges, and RPO obligations vary significantly across India. Real-time visibility into these variables gives procurement heads the ability to identify the lowest true cost of procurement across geographies.

For example, Maharashtra's MSEDCL tariff order for FY 2025-26 applies a 25% surcharge during evening peak hours (1700-2400 Hrs) and a 15-25% rebate during daytime solar hours for HT industrial consumers. Data-driven procurement allows businesses to optimize consumption patterns against these Time-of-Day (ToD) tariffs.

Quantified Financial Case for Data-Driven Procurement

Businesses leveraging data-driven procurement achieve measurable advantages. Forty percent of organizations now use generative AI in procurement, with efficiency gains of 25-40% and annual savings improvements of up to 40%. For Indian C&I buyers navigating multi-state tariff complexity, the practical impact includes:

- Identifying the lowest landed cost across DISCOM zones before committing to a supplier

- Flagging ToD windows where consumption shifting reduces monthly bills

- Benchmarking PPA offers from multiple developers against real-time open access charges

- Tracking RPO compliance gaps before they become regulatory penalties

What's Driving These Four Trends

These trends share a common foundation: a set of structural forces reshaping how Indian businesses source and manage energy.

Technology and Digital Innovation

Declining costs of renewable energy paired with AI, automation, and cloud-based platforms are lowering barriers to sophisticated energy procurement. Capabilities once available only to large enterprises are now accessible to mid-sized industrials through digital marketplaces.

Rising Grid Tariffs and Cost Pressure

DISCOM commercial and industrial tariffs have risen steadily, forcing businesses to seek alternatives beyond passive utility dependency. C&I renewable PPAs typically range from ₹3.20-4.50/kWh, offering considerable savings over grid tariffs.

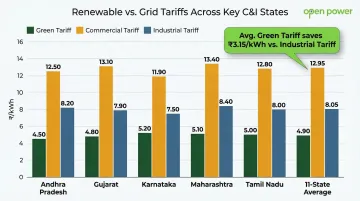

A state-by-state comparison illustrates the gap:

| State | Green Tariff (₹/kWh) | Commercial Tariff (₹/kWh) | Industrial Tariff (₹/kWh) |

|---|---|---|---|

| Andhra Pradesh | 6.18 | 10.54 | 7.14 |

| Gujarat | 6.56 | 7.27 | 7.12 |

| Karnataka | 6.27 | 12.36 | 9.33 |

| Maharashtra | 7.43 | 15.40 | 8.42 |

| Tamil Nadu | 7.64 | 9.57 | 7.90 |

| 11-State Average | 6.50 | 10.17 | 7.79 |

Regulatory and Policy Evolution

Key Indian policy drivers are making renewable energy procurement both easier and, in some sectors, obligatory:

- Green Energy Open Access Rules 2022: Reduced eligibility from 1 MW to 100 kW, with a May 2023 amendment allowing consumers to aggregate multiple connections to meet the threshold

- Renewable Consumption Obligation (RCO): Designated consumers must reach 43.33% total RCO by 2029-30

- 15-day approval window: GEOA Rules mandate rapid processing of open access applications

Market Maturity and Developer Ecosystem Growth

India's renewable developer ecosystem has matured. As of December 31, 2024, India's total installed capacity was 462.07 GW, with renewable energy accounting for 209.44 GW or 45%. That installed base means C&I buyers can now source multi-megawatt renewable capacity without running into developer pipeline constraints.

How These Trends Are Impacting B2B Businesses

Procurement Becomes a Continuous Strategic Function

Energy procurement is shifting from an annual administrative task to a continuous strategic function. Businesses now manage energy as an active portfolio — multiple contracts, multiple states, multiple sources — requiring real-time monitoring and rebalancing.

Measurable Cost Savings Through Optimized Procurement

Long-term PPAs and optimized procurement strategies enable businesses to predictably reduce energy costs. State-level incentives lower the landed cost of power by 25-30% compared to on-grid tariffs.

Unilever, for example, partnered with Brookfield for a 45 MW off-site solar project in Rajasthan to supply 32 sites across 15 states, expecting cost savings of approximately 25% over 20 years compared to grid electricity.

Sustainability-Driven Procurement Creates Competitive Advantages

Green energy sourcing supports market access (export compliance), attracts ESG-focused investors, and reduces carbon liability risk under emerging regulatory frameworks. For export-oriented manufacturers facing carbon border taxes, renewable procurement is now a business continuity imperative.

Workforce Evolution and Capability Requirements

Managing this external complexity — multi-state regulations, sustainability mandates, and dynamic tariff structures — demands a fundamentally different kind of procurement team. Businesses are evolving from contract administrators to multi-disciplinary strategists, building expertise across:

- Energy markets and tariff structures

- Regulatory compliance across multiple states

- Financial modelling and PPA analysis

- Sustainability reporting and carbon accounting

This shift creates demand for specialized in-house talent or technology platforms capable of consolidating these functions. Opten Power's portfolio management dashboard, for instance, gives procurement teams a single view across all renewable assets, contracts, and state-level data — reducing the operational load of managing multi-state, multi-source portfolios.

What Lies Ahead: Future Signals in B2B Energy Procurement

While these four trends define the present, the next 1–3 years will introduce new layers of complexity and opportunity.

Round-the-Clock and Hybrid PPAs Become Standard

To address supply variability, the market is shifting toward hybrid and Round-the-Clock (RTC) models. In 2025, the majority of grid-scale RE tendering shifted to projects having storage and hybrid components.

Green Hydrogen Emerges for Hard-to-Abate Sectors

Green hydrogen is emerging as a long-term decarbonization lever. NITI Aayog projects that green hydrogen costs can fall to approximately ₹132/kg by 2030 and ₹58/kg by 2050, making it competitive with grey hydrogen by 2030.

Near-Term Signals to Watch

- Single-window clearance for interstate open access: Progress on simplifying approvals will accelerate adoption

- Hybrid renewable projects (solar + wind + storage): Preferred PPA structure for 24x7 industrial loads

- Real-time carbon accounting integration: Procurement decisions will increasingly incorporate live carbon footprint tracking

The Strategic Imperative

These signals point to a market that's scaling fast. CRISIL expects C&I renewable capacity to reach 57 GW by fiscal 2028 — a ~40% surge over two fiscals — while JMK Research estimates the Indian iron and steel sector alone will add 20–25 GW of renewable capacity by 2030.

For C&I buyers, the window to lock in favorable long-term tariffs is narrowing. Companies that move early — with clear procurement frameworks and the right project partners — will be better positioned to absorb rising grid tariffs and meet mandatory sustainability disclosures as they take effect.

Frequently Asked Questions

What is B2B in procurement?

B2B (business-to-business) procurement refers to the process by which a company sources goods or services from another business. In the energy context, it means large commercial or industrial consumers directly negotiating energy contracts with suppliers or developers through intermediary platforms, rather than simply accepting utility-assigned tariffs.

How does energy procurement work?

Energy procurement involves analyzing a business's consumption profile, identifying suitable suppliers, negotiating contract terms (price, duration, type), and monitoring the market for optimization opportunities. It's typically managed through an internal team, broker, or digital platform providing real-time market intelligence.

What is B2B solar?

B2B solar refers to solar energy transactions between businesses — where a commercial or industrial consumer procures solar power directly from a developer through an open access agreement or PPA, rather than buying from the grid at standard DISCOM tariffs.

What is a Power Purchase Agreement (PPA) in B2B energy procurement?

A PPA is a long-term contract between an energy buyer (such as a manufacturer or data centre) and a renewable developer, fixing the price of power over a defined period — typically 10–25 years. It gives the buyer price stability, below-grid tariffs, and verifiable green energy supply.

How can businesses reduce energy costs through procurement?

Businesses can reduce costs through several active strategies:

- Switch from DISCOM dependency to open access procurement

- Sign long-term renewable PPAs to lock in below-grid tariffs

- Aggregate load across multiple sites for better negotiating leverage

- Use digital platforms to compare real-time offers from multiple developers

What is open access in B2B energy procurement in India?

Open access is a regulatory mechanism that allows large commercial and industrial consumers (typically above 100 kW or 1 MW, depending on the state) to buy power directly from generators of their choice. Consumers pay wheeling, transmission, and cross-subsidy surcharge fees — but often still achieve substantial savings over DISCOM tariffs.