Introduction: The Data Center Power Crunch

Global data center capacity is undergoing explosive growth. Nearly 100 GW of new capacity will be added between 2026 and 2030, doubling the current footprint at a 14% CAGR, according to JLL's 2026 Global Data Center Outlook. This infrastructure supercycle—requiring up to $3 trillion USD in investment by 2030—is driven primarily by artificial intelligence, cloud computing, and digital services expansion.

In India, the supply-demand imbalance is even more acute. The country's data center inventory stands at 1,123 MW with a tight 4.3% vacancy rate and is projected to reach 2,073 MW by end of 2027, requiring USD 6.3 billion in capital investment, per JLL's December 2025 India Data Centre Market Dynamics report.

In both markets, the binding constraint isn't land or connectivity—it's power. Data centers require 24/7 uninterrupted supply, held to the industry's "Five 9s" standard: 99.999% uptime, allowing just 5.26 minutes of downtime annually.

Grid infrastructure is struggling to keep pace. As JLL states directly: "Power, not location or cost, will be the primary site selection criteria due to multiyear wait times for a grid connection."

This guide covers what offtake capacity is, why securing it has become the defining challenge in data center development, and how operators can structure agreements to stay ahead of the queue.

TL;DR:

- Available offtake capacity—uncommitted power that data centers can contract—is now scarcer than land or connectivity in most markets

- Firm, 24/7 offtake capacity determines project bankability, site selection, and ESG credibility

- Hyperscalers command 49% of global clean energy PPAs; mid-market operators must pursue aggregation, platforms, and diversified portfolios

- India offers cost advantages alongside complex state regulations; platforms like Opten Power can compress procurement timelines by 50%

- Interconnection backlogs, shape risk from renewables, and regulatory fragmentation are the top barriers to securing adequate offtake

What Is Offtake Capacity?

Offtake capacity is the amount of energy—measured in megawatts (MW)—that a data center can reliably draw from the grid or contract from a generator to power its operations. It represents a committed agreement between an energy seller (generator, utility, or grid operator) and a buyer (data center), guaranteeing a specified volume of power over a defined period.

Available offtake capacity is distinct from total installed generation capacity. A region may have 5,000 MW of installed solar and wind capacity, but available offtake is only the uncommitted portion—what a new data center can actually access and contract.

According to Landgate's industry guidance, offtake capacity "refers to the amount of energy that can be safely and reliably withdrawn from the electric grid at any given point," and it shifts with grid upgrades, consumption patterns, and technological changes.

Offtake capacity sits at the intersection of supply and demand. It connects power generators and renewable projects with data centers and industrial loads through structured agreements that lock in:

- Fixed, formulaic, or indexed pricing

- Committed volume in MW capacity and expected MWh delivery

- Long-term duration, typically 10–20 years for corporate PPAs

These agreements function as risk management instruments, not just supply contracts. Tech for Net Zero notes that offtake agreements provide "early avoidance of market risks through fixed volumes and prices" and deliver "future revenue certainty to both lenders and investors"—critical properties for any large-scale infrastructure that requires long-horizon project financing.

Why Available Offtake Capacity Is Critical for Data Centers

Energy Intensity and Operational Viability

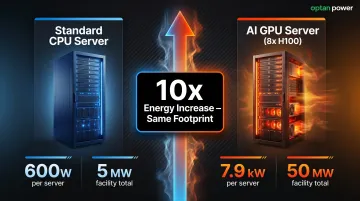

Data centers are among the most energy-intensive infrastructure assets on the planet. A conventional dual-processor server draws approximately 600 W; an AI-accelerated server equipped with 8-GPU NVIDIA H100 chips consumes approximately 7.9 kW operational (rated at 10.2 kW), according to Lawrence Berkeley National Laboratory's 2024 US Data Center Energy Usage Report.

Deloitte's June 2025 analysis illustrates the dramatic impact of AI workloads: switching from CPUs to specialized GPUs can increase a five-acre facility's energy consumption from 5 MW to 50 MW—a tenfold increase on the same footprint.

This intensity has two implications:

- Data centers require not just large volumes of power but firm, dispatchable supply with zero tolerance for interruption

- Available offtake capacity in a region directly determines whether a facility can be built, scaled, or even remain operational

Financial and Bankability Dimension

Lenders and investors use the quality and certainty of a data center's offtake arrangements as a key criterion for project bankability. Long-term agreements with creditworthy counterparties improve project IRR, tighten debt terms, and signal operational stability to equity investors.

Locking in energy costs over a 10–20 year horizon insulates facilities from market volatility. In India specifically, DISCOM tariffs, open access surcharges, and wheeling charges vary significantly by state—making structured offtake agreements essential to protecting project economics.

Scalability and Phased Expansion

That financial certainty directly enables growth planning. Operators who map available offtake capacity before committing to expansion can avoid the costly mismatches that emerge when load outpaces contracted supply. Key planning advantages include:

- Matching each growth phase (e.g., 50 MW → 150 MW) with pre-contracted supply

- Avoiding construction delays caused by last-minute power procurement

- Retaining site flexibility rather than relocating to power-abundant markets

Sustainability and ESG Differentiation

For data centers with clean energy pledges or ESG commitments, **offtake agreements structured with renewable energy projects** are the primary mechanism for achieving and demonstrating carbon-free operations.

Over 400 companies have committed to 100% renewable electricity through the RE100 initiative. BloombergNEF's 1H 2026 Corporate Energy Market Outlook reports that Meta, Amazon, Google, and Microsoft alone accounted for 49% of all global corporate clean energy PPA activity in 2025, contracting 55.9 GW total. For hyperscalers, these deals do more than meet compliance targets—they unlock preferential financing terms and satisfy enterprise customer sustainability requirements. Indian data center operators face the same pressure, with domestic RE100 signatories and export-facing clients increasingly requiring verifiable clean energy procurement as a condition of partnership.

Types of Offtake Agreements Data Centers Use

The right offtake structure depends on the data center's load profile, location, regulatory environment, sustainability targets, and risk appetite. Here are the primary models:

Physical Power Purchase Agreements (PPAs)

Physical PPAs involve actual delivery of electricity from a generator to the data center. The buyer receives the power and, for renewable projects, the associated renewable energy certificates (RECs).

Key terms:

- Duration: 10–20 years

- Pricing: Fixed or formulaic (with inflation escalators or fuel adjustments)

- Delivery: Requires coordination with grid operators and transmission access

Advantages:

- Price certainty over the contract term

- Direct renewable energy claims with bundled RECs

- Reliability through contractually committed supply

Constraints:

- Requires geographic proximity or co-location with the generator

- Complex interconnection and grid scheduling

- Not viable in all regulated markets where open access is restricted

Virtual PPAs (VPPAs)

Virtual PPAs are financial instruments, not physical delivery contracts. The data center procures energy from its local utility while settling a fixed-for-floating price swap with a remote generator. The data center also acquires RECs to claim clean energy use.

How it works:

- Generator sells power into the wholesale market at market price

- Data center pays the generator a fixed contract price

- Generator reimburses the data center if market price exceeds contract price (or vice versa)

Advantages:

- Geographic flexibility—no need for physical proximity

- Supports additionality (funding genuinely new renewable capacity that wouldn't otherwise be built)

- Enables corporate offtake from remote, high-quality resource zones

Trade-offs:

- Market price risk: if wholesale prices diverge significantly from the fixed contract price, settlement payments can become unpredictable

- Requires separate utility supply contract

- Complex accounting and financial structuring

Columbia University's Center on Global Energy Policy notes that VPPAs represented approximately 80% of US corporate renewable procurement from 2016 to 2019—a share driven by companies that needed clean energy credits without the geographic constraints of physical delivery.

Corporate PPAs and Long-Term Bilateral Agreements

Where VPPAs settle financially, corporate PPAs go a step further: they are direct, negotiated agreements between a data center (or hyperscaler) and a power developer, structured for dedicated renewable capacity over multi-year or multi-decade horizons.

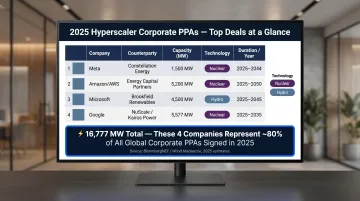

Recent examples:

| Company | Counterparty | Capacity | Technology | Duration | Year |

|---|---|---|---|---|---|

| Meta | Constellation Energy | 1,121 MW | Nuclear (Clinton plant, IL) | 20 years | Jun 2025 |

| Amazon/AWS | Talen Energy | 1,920 MW | Nuclear (Susquehanna) | Through 2042 | 2024 |

| Microsoft | Constellation Energy | 835 MW | Nuclear (TMI Unit 1 restart) | 20 years | Sep 2024 |

| Brookfield Renewable | Up to 3,000 MW | Hydroelectric | 20 years (first PPAs) | Jul 2025 |

These agreements represent the dominant procurement model for large-scale data centers. S&P Global reported in February 2026 that Amazon, Google, Meta, and Microsoft signed 16,777 MW of corporate renewables contracts in 2025, approximately 80% of the total 20,448 MW signed globally.

Utility Tariffs and Green Tariffs

In regulated markets where direct procurement is restricted, data centers rely on utility-administered tariffs.

Green tariffs allow customers to source bundled renewable electricity from a specific project, often at a premium to standard grid tariffs.

Emerging 24/7 clean energy tariffs go further, matching real-time load with clean generation on an hourly basis to enable credible carbon-free energy claims under tightening greenhouse gas accounting standards.

Constellation and Microsoft's 2023 agreement to provide up to 35% of a Boydton, Virginia data center's environmental attributes from nuclear power using hourly carbon-free energy (CFE) matching demonstrates this trend. The proposed GHG Protocol Scope 2 amendments would require hourly matching and deliverability for market-based reporting, making annual RECs insufficient for credible clean energy claims.

How Offtake Capacity Shapes Data Center Site Selection

CBRE's H1 2025 North America Data Center Trends report is direct: "Power availability remains the foremost site selection criterion for greenfield data center developments." Available offtake capacity now drives decisions ahead of location, cost, and connectivity.

Energy Factors in Regional Assessment

Data center operators now evaluate locations based on a cluster of energy factors:

- Proximity to renewable generation assets — reduces transmission losses and wheeling charges

- Existing transmission and grid infrastructure — shorter interconnection timelines

- DISCOM or utility tariff structures — competitive retail rates and transparent open access policies

- Availability of pre-contracted or readily accessible power capacity — uncommitted generation or reserved grid headroom

In India, state-level policy differences make this assessment particularly complex. Mercom India reported that India added 7.8 GW of solar open access capacity in 2025, with cumulative capacity exceeding 30 GW as of December 2025.

That growth is heavily concentrated: Karnataka, Maharashtra, Rajasthan, Gujarat, and Tamil Nadu account for over 85% of installations — reflecting sharp state-by-state variation in regulatory support for open access procurement.

Cross-subsidy surcharges and additional surcharges vary dramatically. Telangana's GERC set additional surcharge for open access consumers at ₹0.13/kWh for H1 FY2026-27, far below the ₹0.59/kWh DISCOMs had requested, but this regulatory uncertainty complicates long-term procurement planning.

Co-Location Models

Some data centers are sited adjacent to renewable energy projects or power plants to reduce transmission costs, gain behind-the-meter access to generation, and improve reliability.

Amazon's co-location with Talen Energy's Susquehanna nuclear plant is a prominent example. AWS secured 1,920 MW of nuclear capacity through a co-located arrangement, transitioning to a "front-of-the-meter" configuration after transmission reconfigurations expected in Spring 2026, with Amazon committing $20 billion in Pennsylvania investment.

Co-location deals of this scale require navigating FERC interconnection rules, state utility commission approvals, and grid stability reviews — each capable of adding 12–24 months to project timelines.

Key Challenges in Securing Adequate Offtake Capacity

Interconnection Queue Backlogs

Interconnection delays are the single largest bottleneck for data centers seeking offtake capacity.

Lawrence Berkeley National Laboratory's Queued Up 2025 Edition puts the scale of the problem in stark terms:

- ~2,290 GW of active capacity sits in US queues (1,400 GW generation + 890 GW storage) across ~10,300 projects

- Median wait time has grown from under 2 years (2000–2007) to over 4 years (2018–2024)

- Only 13% of projects entering queues between 2000–2019 reached commercial operation; 77% were withdrawn

This creates a practical gap: data center construction runs 18–24 months, but grid connection timelines now exceed 4 years. Operators are forced to:

- Build onsite generation (gas, diesel, or modular nuclear)

- Acquire existing interconnection rights through M&A

- Relocate to markets with available capacity and shorter queues

Shape and Volume Risk: Renewable Intermittency vs. 24/7 Load

Data centers require flat, 24/7 power, but the cheapest clean energy sources—solar and wind—are intermittent.

This creates shape risk: a VPPA with a solar project delivers power during daylight hours but provides no generation at night. If wholesale power prices are higher at night, the data center's settlement payments increase, creating financial volatility.

Hyperscalers are addressing this through pivots to nuclear, hydro, and geothermal. BloombergNEF reported that in 2025, 5.8 GW of co-located and hybrid deals were tracked as battery costs continued to decline—and these deal structures are expected to become the new standard for corporate procurement.

The economics are shifting fast. BNEF's February 2026 analysis shows the global benchmark cost for a four-hour battery project fell 27% year-on-year to $78/MWh in 2025. Developers added 87 GW of combined solar-plus-storage at an average of $57/MWh—cost parity with baseload generation in many markets.

Regulatory and Market Fragmentation

These global supply-side constraints are compounded in India by regulatory complexity that is entirely its own. The patchwork of state-level DISCOM regulations, open access policies, and transmission charges means that offtake capacity available on paper may be significantly more expensive or harder to access in practice.

For example:

- Wheeling charges (for transmission of power) vary by state

- Banking charges (for energy stored on the grid) differ by DISCOM

- Cross-subsidy surcharges can add ₹1–3/kWh in some states

- Open access thresholds (minimum contracted demand) exclude smaller operators in some jurisdictions

For a data centre operator evaluating sites across multiple states, these variables can swing the landed cost of power substantially—making state-by-state regulatory analysis as important as the underlying tariff.

How Data Centers Can Access Available Offtake Capacity

Early Engagement and Parallel Planning

The most effective strategy is early engagement—initiating interconnection studies, PPA negotiations, and regulatory approvals in parallel with land acquisition and construction planning, not as a downstream activity.

Waiting to secure offtake capacity until after site selection or permitting is complete introduces significant project risk. Data centers that treat power procurement as a first-order constraint are better positioned to lock in capacity before grid queues and developer pipelines fill up.

Energy Intelligence Platforms and Clean Energy Marketplaces

Emerging energy intelligence platforms and clean energy marketplaces are accelerating offtake capacity discovery and procurement by:

- Aggregating available renewable capacity across states and project types

- Providing real-time tariff and pricing data across utilities and DISCOMs

- Offering automated RFP and contract workflows

- Compressing time from site selection to signed offtake agreement

For example, platforms like Opten Power offer access to 4+ GW of pre-vetted renewable capacity across solar, wind, and hybrid projects in 16 states in India, with real-time DISCOM intelligence and automated procurement tools. Data centers can compare developers, tariffs, and projected savings in one place—rather than managing dozens of separate conversations with developers—cutting procurement timelines by up to 50%.

Portfolio Diversification as Risk Management

Faster procurement only solves part of the problem. Data centers that rely on a single offtake source remain exposed to price volatility and supply disruptions. Mixing sources reduces single-point-of-failure risk and builds operational flexibility.

Common approaches include:

- Combining long-term corporate PPAs with grid tariffs

- Pairing renewable PPAs with battery storage arrangements

- Maintaining backup generation (diesel, gas, or modular nuclear) for critical load

- Structuring hybrid PPAs that blend solar, wind, and storage

S&P Global reported in March 2026 that data centers consumed approximately 270 TWh of electricity in 2025 and procured approximately 180 TWh of clean energy through PPAs—indicating approximately 67% clean energy coverage, with the remainder sourced from grid tariffs and backup generation. The figures, drawn from North American PPA market data, reflect a broader global pattern: leading operators run multi-source portfolios rather than depending on any single offtake mechanism.

Frequently Asked Questions

What is the purpose of a data center offtake agreement?

A data center offtake agreement is a contract that secures a reliable, price-certain supply of electricity from a generator or grid operator. It ensures operational continuity, manages energy cost risk, supports sustainability goals, and underpins project financing by giving lenders confidence in long-term revenue and cost structures.

How much does a 50 MW data center cost?

A 50 MW facility typically costs ₹3,962.5 crore to ₹6,312.5 crore (USD 475M–750M), based on global averages of ₹792.5–₹1,126.25 crore per MW for standard hyperscale builds, per Cushman & Wakefield's 2025 Data Center Development Cost Guide. India (Mumbai/Chennai) ranks among the lowest-cost regions at ₹626–₹792.5 crore per MW, with energy infrastructure accounting for 15–20% of total project cost.

What is available offtake capacity for a data center?

Available offtake capacity refers to power generation or grid headroom that can be contracted or drawn upon by a data center. It's distinct from total installed capacity in a region, representing the uncommitted supply that a developer can access through offtake agreements to meet their load requirements.

What is the difference between a physical PPA and a virtual PPA for data centers?

A physical PPA delivers electricity directly from a specific generator to the data center. A virtual PPA (VPPA) is a financial contract — the data center buys grid power locally but settles price differences with a remote generator and acquires RECs. Physical PPAs guarantee direct supply; VPPAs offer geographic flexibility at the cost of market price exposure.

How does offtake capacity availability affect data center site selection?

Regions with readily accessible offtake capacity—shorter interconnection queues, lower tariffs, and available renewable generation—attract data center investment because they reduce time-to-power, lower operational costs, and simplify ESG compliance. Power availability is now as critical a siting factor as land cost or network connectivity, often determining whether a project is viable at all.

How long does it take to secure an offtake agreement for a data center in India?

Timelines vary by state and procurement route. Direct corporate PPAs through open access can take several months to over a year when including regulatory approvals, DISCOM coordination, and RFP processes. Platforms that offer pre-vetted projects and automated procurement tools can cut deal closure time by up to 50% compared to traditional procurement methods.