Introduction

The corporate renewable energy market is shifting fast. Global procurement hit 55.9 GW in 2025—down 10% from the previous year's record—yet the buyers still active are structuring fundamentally more sophisticated deals. Co-located solar+storage, hybrid projects, and 24/7 carbon-free energy matching have moved from pilot stage to standard expectation.

That shift closes the "easy era" of renewable buying, when companies could purchase cheap Renewable Energy Certificates (RECs) and declare sustainability targets met.

Commercial and industrial (C&I) buyers—particularly across India's fast-growing industrial sectors—now face a direct choice: upgrade to procurement instruments that reflect actual carbon impact and meet tightening regulatory standards, or risk significant cost savings while exposing their organizations to compliance and reputational risk.

What follows breaks down the forces driving this change and the concrete steps your organization can take to stay ahead of them.

Key Takeaways

- Sophisticated corporate buyers are moving beyond standalone RECs toward PPAs, hybrid deals, and co-located arrangements

- The GHG Protocol's proposed hourly Scope 2 tracking will make broad "100% renewable" claims much harder to sustain without quality instruments

- Next-stage procurement is defined by additionality, temporal matching, portfolio diversification, and data-driven decision-making

- Indian C&I buyers face real but solvable barriers; acting now cuts energy costs and gets ahead of tightening compliance requirements

The Shifting Landscape of Corporate Renewable Procurement

The Global Trend Reversal

After nearly a decade of continuous growth, corporate clean energy buying fell 10% to 55.9 GW in 2025, according to BloombergNEF. Rising project costs, policy uncertainty, and market consolidation drove the decline—a signal that buyers can no longer rely on the straightforward deal structures that worked in earlier markets.

This isn't simply a temporary dip. The pullback reflects fundamental market restructuring as buyers face higher capital costs, longer development timelines, and greater regulatory scrutiny of renewable energy claims.

Market Consolidation Among Super Users

Procurement is increasingly concentrated among large hyperscalers and industrial "super users." Meta, Amazon, Google, and Microsoft comprised 49% of all corporate PPA activity in 2025, while the number of unique U.S. corporate buyers dropped 51% year-on-year to just 33.

The implication for mid-sized C&I buyers: Unless you adapt to more sophisticated procurement structures, you risk being priced out of the most attractive renewable deals as hyperscalers dominate developer pipelines and lock in favourable terms.

Technology Shifts Reshaping Deal Structures

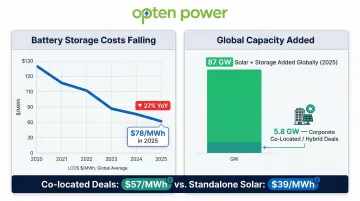

Battery storage costs fell 27% year-on-year to a record low of $78/MWh in 2025, making co-located solar+storage and hybrid deals economically viable at scale. Developers added 87 GW of combined solar and storage globally, with 5.8 GW signed as corporate co-located or hybrid deals.

This changes what "bankable" procurement looks like. Co-located projects deliver power with higher temporal matching to actual consumption, reducing reliance on grid electricity during non-solar hours and improving carbon accounting accuracy.

The Regulatory Catalyst

The GHG Protocol launched a public consultation in October 2025 proposing updates to Scope 2 emissions standards—moving from annual to hourly tracking of renewable energy consumption. Companies that have built their sustainability reporting on annual averages will need to restructure both their procurement contracts and their data infrastructure.

The rise of co-located and hybrid deals tracked in 2025 is early evidence that leading buyers are already adapting deal design to meet stricter hourly matching requirements before they become mandatory.

Implications for Indian C&I Buyers

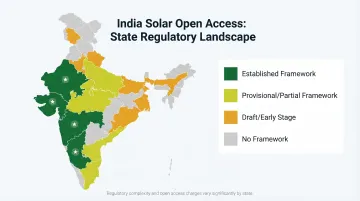

India's renewable energy ambitions—283.46 GW of non-fossil capacity installed as of March 2026 and a 500 GW target by 2030—mean corporate buyers in 16+ states operate in a rapidly evolving regulatory and tariff environment. India added 7.8 GW of solar open access capacity in 2025 alone, driven by corporate decarbonization needs.

Multinational customers and ESG investors are already scrutinizing supply chain Scope 2 emissions with far greater precision. Indian C&I companies still relying on RECs or basic open access agreements—without hourly matching or verified additionality—are exposed to both compliance failures and reputational risk in global value chains.

Why Traditional Procurement Methods Are Falling Short

The Credibility Gap in REC-Based Procurement

Companies claim an average of 29% renewable electricity usage, but only 16% is verifiable with transparent mechanism disclosure, according to CDP data. RECs purchased across different grids than where electricity is consumed send no meaningful market signal and don't drive new renewable capacity.

A REC from a decades-old hydro project in another region provides zero additionality—it doesn't finance new renewable capacity or reduce emissions where your company operates.

The Additionality Problem

Industry initiatives are tightening criteria. RE100 now requires procurement from projects commissioned or repowered within the past 15 years, ensuring claims reflect new renewable capacity. The SBTi's Corporate Net-Zero Standard Version 2.0 proposes a 10-year limit, tightening to 5 years by 2035.

Purchasing RECs from old projects no longer counts under stricter voluntary and mandatory frameworks. Only instruments that finance new capacity—primarily PPAs—meet the rising bar.

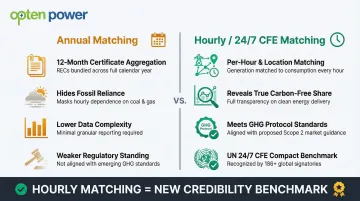

The Temporal Matching Gap

Most companies rely on annual matching (procuring enough RE certificates over 12 months to offset yearly consumption). This hides the reality that they consume fossil-fuel-powered electricity during hours when renewables aren't generating.

Hourly or sub-hourly matching—pioneered by companies like Google and Microsoft and formalized in the UN 24/7 Carbon-Free Energy Compact with 186+ signatories—is becoming the new credibility benchmark. Annual matching may soon be insufficient for regulatory compliance and stakeholder scrutiny.

The Verification Deficit

61% of companies have no third-party verification of their market-based Scope 2 emissions, making renewable claims difficult to audit or compare. As mandatory disclosure regulation like ESRS E1 in Europe expands, unverified claims create reputational and regulatory risk.

Implications for Indian C&I Buyers

These global shifts aren't distant concerns for Indian buyers. Companies relying on DISCOM green tariffs or unbundled renewable certificates face the same credibility and compliance pressures—just arriving faster than many expect.

Key risks for Indian C&I buyers without verifiable procurement mechanisms:

- Multinational customers auditing Scope 2 emissions across their supply chains

- ESG investors applying stricter sustainability screens to portfolio companies

- Export-oriented businesses losing contracts to competitors with stronger renewable credentials

- Growing regulatory scrutiny as India aligns with international disclosure standards

What the Next Stage of Corporate Renewable Procurement Looks Like

From Commodity to Portfolio Thinking

The next stage is not about buying a single REC product but building a diversified energy procurement portfolio. This includes:

- Long-term PPAs for cost certainty and additionality

- Hybrid/co-located solar+storage deals for round-the-clock coverage

- Virtual PPAs for financial hedging without physical delivery

- Calibration to load profile, geography, and sustainability targets

This portfolio approach reduces risk, improves temporal matching, and provides defensible carbon accounting.

The Rise of Co-Located and Hybrid Deal Structures

Co-located deals pair renewable generation (typically solar) with battery storage on the same site, delivering power with higher temporal matching. Developers added 87 GW of combined solar and storage globally in 2025, delivering power at an average of $57/MWh—compared to $39/MWh for standalone solar. These are global benchmarks; Indian hybrid tariffs vary by state and grid zone, but the cost trajectory mirrors the same downward trend as battery prices fall.

Co-located deals provide 24/7 or near-24/7 coverage, significantly improving hourly matching as battery prices continue to fall.

The Move Toward 24/7 Carbon-Free Energy

More than 186 companies and institutions have signed the UN 24/7 CFE Compact, committing to match electricity consumption with clean generation on an hourly basis. For Indian manufacturers and exporters supplying global supply chains, these standards increasingly apply upstream — making hourly matching a procurement reality, not just a compliance checkbox. This is a journey, not a binary switch: even partial hourly matching improves carbon accounting accuracy and additionality impact.

Start with partial hourly matching for a portion of load, expand coverage over time, and use co-located or hybrid deals to fill gaps when solar and wind generation are low.

Additionality in Practice

Achieving strong hourly matching means little if the underlying procurement doesn't fund genuinely new capacity. Procurement that finances new renewable projects creates real emissions displacement — and that's where additionality criteria become the differentiator.

Quality markers include:

- Project age criteria (e.g., RE100's 15-year limit, SBTi's 10-year limit)

- Local grid matching (procuring energy on the same grid where consumption occurs)

- Incremental funding structures (PPAs that enable project financing)

When comparing developer offers, evaluate these criteria explicitly—not all "green" procurement is equally impactful.

Green Hydrogen and Long-Duration Storage

For heavy industries (steel, cement, chemicals) with 24/7 baseload needs, green hydrogen and long-duration storage are becoming viable complements to intermittent renewables. Both are still commercializing, but procurement teams should structure agreements now that can accommodate these assets as they scale — keeping the portfolio flexible enough to integrate them without renegotiating from scratch.

How to Prepare Your Organization for the Transition

Audit Your Current Energy Procurement Baseline

Before upgrading your strategy, map your current position:

- Electricity sources: DISCOM tariff, open access, RECs, PPAs?

- Scope 2 reporting quality: Third-party verified? Mechanism-disclosed? Aligned with BRSR or GHG Protocol disclosure requirements?

- Recognised vs. claimed renewables: What share would qualify under stricter criteria?

This baseline surfaces the gap between where you are and where SEBI BRSR disclosures, RE100 criteria, and buyer due diligence are pushing the market.

Define Your Procurement Ambition and Timeline

With your baseline in hand, set an internal target — not just a percentage of renewables, but a quality target:

- For larger companies: Explore 100% RE targets with partial hourly matching by a specific year

- For smaller buyers: Start with a PPA or co-located deal covering part of your load

- Set a Scope 2 reduction goal: Quantify emissions impact, not just procurement volume

A defined timeline also tells developers you're a serious buyer — which matters when pipeline slots are competitive.

Build Supplier and Developer Relationships Early

Quality procurement means engaging developers directly — not just buying certificates through brokers. Start now:

- Research the open access and PPA landscape in your operating states

- Prequalify developers based on track record, financial stability, and project pipeline

- Launch RFP processes early — project development and grid connection have long lead times

Navigating India's Unique Renewable Procurement Landscape

Structural Advantages for Indian C&I Buyers

India is one of the fastest-growing renewable energy markets globally, with abundant solar and wind resources and an active open access framework. India added 7.8 GW of solar open access capacity in 2025, reaching 20.2 GW cumulative, providing substantial capacity accessible to corporate buyers across states.

Barriers and Complexity

State-by-state variability creates real friction:

- DISCOM regulations differ across states

- Open access charges (wheeling, banking, cross-subsidy surcharges) vary widely

- Policy unpredictability creates risk

Savings for C&I consumers narrowed in Q4 2025 as PPA tariffs rose ₹0.25/kWh due to Domestic Content Requirement mandates, and savings in Punjab and Tamil Nadu turned negative under the third-party model.

Real-time intelligence on landing prices and regulatory conditions across states is essential — procurement decisions based on outdated or generic tariff data expose buyers to avoidable cost overruns.

The Opportunity for Indian Industries to Leapfrog

Because India's corporate PPA market is still maturing, early movers who structure quality, long-term PPAs now can lock in below-market energy costs while positioning for stronger ESG compliance ahead of tightening global reporting standards affecting export-oriented or MNC-linked supply chains.

States like Karnataka, Maharashtra, and Gujarat — which hold the highest cumulative solar open access capacity — offer established regulatory frameworks that reduce execution risk for first-time corporate buyers.

Using Technology to Streamline Your Renewable Procurement

Why Procurement Complexity Demands Technology

Managing multi-state regulatory variability, comparing developer proposals in real time, and tracking portfolio performance simultaneously is a lot. Add evolving Scope 2 reporting standards into the mix, and spreadsheets or broker relationships simply can't keep up at scale.

Technology platforms that centralize discovery, comparison, contracting, and monitoring are becoming essential infrastructure for corporate energy buyers.

How Platforms Like Opten Power Address This

India's unified clean energy marketplaces—such as Opten Power—give C&I buyers:

- Access to 4+ GW of vetted renewable projects across solar, wind, and hybrid in 16 states

- Real-time DISCOM intelligence with standardized, regularly updated landing prices for accurate state-by-state cost comparison

- Automated tender engines that handle RFP creation, template customization, and bid management

- A unified portfolio dashboard to monitor all renewable investments and track savings in one place

Together, these tools help C&I buyers cut deal timelines by up to 50%—and walk into every negotiation knowing the numbers before the conversation starts.

Frequently Asked Questions

What is the difference between a REC and a PPA in corporate renewable procurement?

RECs are certificates representing renewable generation purchased separately from actual electricity, while a PPA is a direct long-term contract with a renewable energy generator, delivering both electricity and environmental attributes. PPAs are stronger instruments because they finance new capacity (additionality) and provide cost certainty.

How does hourly matching (24/7 CFE) differ from annual renewable energy matching?

Annual matching only requires procuring enough RE certificates to cover total yearly consumption, hiding reliance on fossil fuels during specific hours. Hourly matching requires renewable generation to be matched to consumption in the same hour and location, revealing the true share of carbon-free electricity in real time.

What regulatory changes are pushing companies toward more sophisticated renewable procurement?

The GHG Protocol's proposed Scope 2 updates require hourly tracking, while expanding frameworks like ESRS E1 in Europe mandate stricter disclosure. Voluntary initiatives like RE100 and SBTi are also tightening quality criteria, collectively raising the bar for credible renewable energy claims.

What is a co-located or hybrid renewable energy deal?

Co-located deals pair a renewable energy source (such as solar) with battery storage on the same site, enabling more consistent and round-the-clock delivery of clean power. They're particularly valuable for C&I buyers with 24/7 operational loads and are increasingly cost-competitive as battery prices fall.

How can C&I companies start transitioning from RECs to Power Purchase Agreements?

Start by auditing your current energy mix and Scope 2 baseline, then engage directly with renewable developers or marketplace platforms to issue RFPs for open access PPAs. Compare offers across states on a like-for-like basis using standardized cost metrics, including DISCOM charges and regulatory fees.

Why is third-party verification of Scope 2 emissions important in renewable procurement?

Without third-party verification, renewable energy claims cannot be externally audited or trusted by investors, customers, or regulators. As mandatory disclosure regulation expands globally, unverified claims expose companies to greenwashing risk and compliance gaps — especially those with cross-border supply chains or ESG-linked financing.