Introduction

Global renewable energy investment hit nearly half a trillion dollars in 2025, yet corporate clean energy buying volume fell for the first time in nearly a decade. The two trends aren't contradictory — they reflect a market restructuring that procurement heads, energy managers, and C&I business leaders can't afford to ignore.

Capital is concentrating in fewer, larger projects, dominated by hyperscalers whose power needs dwarf traditional C&I buyers.

This roundup covers four themes reshaping corporate renewable procurement: the 2025 global buying dip driven by rising costs and policy uncertainty, Big Tech's growing share of nearly half of all clean energy deals, the systemic inefficiency crisis slowing capital deployment despite record investment, and accelerating PPA market growth toward 2030.

For Indian C&I buyers navigating state-level DISCOM complexity and open access regulations, these global headwinds signal an urgent need to modernize procurement approaches before costs and complexity widen further.

TLDR: Key Takeaways at a Glance

- Global corporate clean energy procurement fell to 55.9 GW in 2025, down from 62 GW in 2024, driven by rising project costs and policy uncertainty

- Big Tech accounted for 49% of global corporate clean energy activity, with fewer unique buyers entering the market

- The renewable PPA market is projected to reach USD $59.58 billion by 2030 (11% CAGR), with long-term growth outpacing near-term headwinds

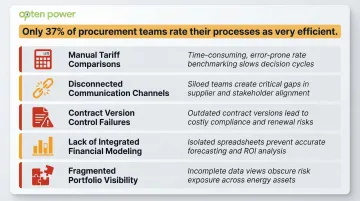

- Only 37% of procurement teams rate their processes as "very efficient" — a growing liability as ESG regulations tighten globally

- Indian C&I buyers can cut through procurement fragmentation using unified marketplace platforms like Opten Power — closing deals up to 50% faster

Global Renewable Energy Procurement in 2025: The Numbers That Matter

The corporate clean power market experienced a historic reversal in 2025. According to BloombergNEF's 1H 2026 Corporate Energy Market Outlook, worldwide corporate Power Purchase Agreement (PPA) volumes fell 10% to 55.9 GW, down from a record 62 GW in 2024. This marks the first year-on-year decline in nearly a decade, driven by two primary forces: rising project costs across solar and wind technologies, and persistent policy uncertainty in key markets.

Regional Divergence Shows Market Fragmentation

While global volumes contracted, regional performance varied sharply. The Americas emerged as the only region where deal volume did not drop, with the US hosting a record 29.5 GW of deals. This resilience contrasts starkly with declines across Europe and Asia-Pacific — a pattern driven by large tech company (hyperscaler) demand concentrated in North America, which is reshaping global procurement geography.

Capital Concentration: More Money, Fewer Deals

The capital flow tells a revealing story. Global energy transition investment reached a record $2.3 trillion in 2025, yet transaction volumes rose only modestly. Capital is flowing into fewer, larger, more complex projects rather than a broader base of deals — a trend that favors well-resourced buyers with the technical capabilities to structure complex transactions.

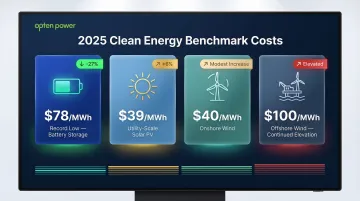

Technology Cost Signals: The Battery Storage Breakthrough

Technology costs diverged dramatically in 2025, creating new procurement opportunities:

| Technology | 2025 Benchmark Cost | Year-on-Year Change |

|---|---|---|

| Battery Storage (4-hour) | $78/MWh | -27% (record low) |

| Utility-Scale Solar PV | $39/MWh | +6% |

| Onshore Wind | $40/MWh | Modest increase |

| Offshore Wind | $100/MWh | Continued elevation |

According to BloombergNEF's February 2026 analysis, battery storage costs hit record lows while renewable generation costs rose modestly. This divergence is accelerating hybrid and co-located solar-plus-storage deals: 5.8 GW of such projects were tracked in 2025, with developers adding 87 GW of combined solar and storage capacity globally.

Europe's Structural Shift

Wind and solar overtook fossil fuels to generate 30.1% of EU electricity in 2025, while all fossil sources generated 29.0%. Coal fell to a historic low of 9.2%, reshaping procurement expectations as European grids decarbonize faster than anticipated. This shift is raising the bar for corporate clean energy claims globally, as buyers face pressure to demonstrate additionality rather than simply purchasing renewable electricity from increasingly clean grids. For Indian C&I buyers, these global signals reinforce the same direction: the economics increasingly favor procurement over inaction, particularly as solar-plus-storage hybrid structures become more cost-competitive.

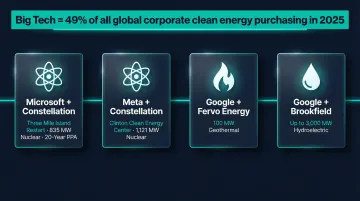

Big Tech's Outsized Role and What It Signals for Corporate Buyers

Hyperscaler Market Dominance

Technology giants Meta, Amazon, Google, and Microsoft collectively drove 49% of all global corporate clean energy purchasing in 2025. Meta and Amazon alone contracted a combined 20.4 GW, including 4.7 GW of nuclear power. This concentration is narrowing market access for smaller corporate buyers, who face stiffer competition for projects and developers increasingly prioritizing large, creditworthy hyperscale deals.

The Pivot to 24/7 Firm Power

Hyperscalers are moving beyond simple solar and wind contracts toward nuclear, hydro, and geothermal — technologies that deliver firm, round-the-clock power. Compute requirements for data centres could reach 220 GW by 2030 according to McKinsey, making intermittent renewables insufficient for operational continuity.

Notable 2025 deals demonstrate this strategic pivot:

- Microsoft signed a 20-year PPA with Constellation to restart Three Mile Island Unit 1, adding 835 MW of carbon-free nuclear energy

- Meta secured 1,121 MW of emissions-free nuclear energy from Constellation's Clinton Clean Energy Center

- Google invested in Fervo Energy's 100 MW firm geothermal power project

- Google signed a Hydro Framework Agreement with Brookfield to deliver up to 3,000 MW of carbon-free hydroelectric capacity

The GHG Protocol's Hourly Matching Requirement

These deals aren't purely commercial — they're also positioning ahead of stricter emissions accounting rules. The GHG Protocol's 2025 public consultation on Scope 2 Guidance proposes requiring that all contractual instruments used in market-based Scope 2 accounting be issued and redeemed for the same hour as energy consumption. Under this proposed framework, annual renewable energy certificate claims would no longer satisfy market-based reporting, pushing buyers toward co-located, hybrid, and time-matched procurement structures.

For Indian C&I buyers, the parallel is direct. SEBI's Business Responsibility and Sustainability Reporting (BRSR) framework and growing pressure from global supply chain partners are pushing large Indian manufacturers, data centres, and IT parks toward verifiable, time-aligned clean energy claims — not just annual REC retirement.

The Mid-Market Squeeze

As Big Tech crowds out simpler deal structures and drives up project costs, mid-market C&I companies face a more competitive procurement environment. In India, this dynamic is already visible — large hyperscale data centre operators entering the market are absorbing premium wind and solar capacity in high-demand states like Rajasthan, Gujarat, and Tamil Nadu.

For industrial buyers in steel, cement, and manufacturing, the window to lock in long-term PPA pricing at favourable rates is narrowing. Companies that move early — with clear load profiles, structured RFPs, and multi-developer comparisons — will secure better terms than those responding reactively to rising grid tariffs and tightening ESG disclosure timelines.

The Procurement Efficiency Gap: Why Capital Alone Isn't Enough

Despite record capital deployment, renewable energy procurement processes remain deeply inefficient. Ansarada's Renewable Energy Infrastructure Outlook 2026 surveyed 150 senior executives and revealed a troubling efficiency gap.

Only 37% of EMEA and Americas respondents describe their most recent renewables procurement process as "very efficient." This drops to just 24% in Asia-Pacific. The gap costs organizations in project delivery speed, capital deployment efficiency, and ultimately, competitive advantage as faster-moving peers secure better projects.

The Transparency Crisis

Approximately 90% of EMEA respondents say transparency and auditability are essential to their procurement process, yet nearly a third admit their processes lack clarity for internal stakeholders. As ESG regulations tighten and investors demand accountability, that lack of clarity becomes a direct commercial risk. This same accountability gap extends into how organizations manage their procurement tools.

The "Frankenstack" Problem

Organizations claiming to use purpose-built procurement software are running an average of 3.8 disconnected systems simultaneously. More than half still rely on email for sensitive bidding correspondence. This fragmentation breaks the accountability "golden thread" that investors and regulators now require, creating version control nightmares and audit trail gaps.

Key inefficiencies plaguing renewable procurement:

- Manual tariff comparisons across multiple developers and geographies

- Disconnected communication channels with no centralized record

- Contract version control failures during negotiation

- Lack of integrated financial modeling across procurement options

- Fragmented portfolio visibility across multiple investments

The Indian C&I Context

Indian C&I buyers face parallel fragmentation challenges: state DISCOM tariff variations, open access regulations that differ by jurisdiction, and the need to compare offers across solar, wind, and hybrid developers. These inefficiencies mirror global challenges but are compounded by regulatory complexity across India's 16+ state electricity markets.

Unified marketplace platforms are emerging as a direct response to this complexity. Opten Power, for instance, consolidates DISCOM intelligence across 16 states, automates RFP creation, and delivers instant IRR and payback analysis — cutting procurement timelines by up to 50% for C&I buyers navigating this fragmented landscape.

The Renewable PPA Market: Growth, Sophistication, and New Structures

Despite near-term volume declines, the long-term PPA market outlook remains strong. The global renewable PPA market is projected to reach $59.58 billion by 2030 at an 11% CAGR, driven by corporate decarbonization goals, regulatory support, and falling technology costs.

Solar PPAs are expected to comprise the largest market segment, followed by wind. Growth drivers include mandatory corporate sustainability reporting, investor pressure for credible decarbonization pathways, and the economic case for long-term price certainty amid volatile wholesale electricity markets.

Evolving Deal Structures

With battery storage costs hitting record lows, co-located renewable-plus-storage projects are becoming mainstream. These structures offer:

- Fixed-price models that lock in long-term electricity costs

- Index-based pricing that adjusts with market conditions while maintaining renewable attributes

- Hybrid pricing that combines elements of both for balanced risk management

The 5.8 GW of co-located and hybrid deals tracked in 2025 represent a clear move away from simple solar or wind contracts — buyers now expect energy solutions that deliver power when it's needed, not just when conditions allow.

Virtual vs. Physical PPAs

As deal structures grow more complex, the virtual vs. physical PPA decision has become a defining factor for C&I buyers managing electricity price risk:

- Virtual PPAs (VPPAs) settle financially on the difference between the contract strike price and wholesale market prices — widely used by corporate buyers seeking price hedges without physical delivery obligations

- Physical PPAs deliver actual electricity through open access or direct connection, providing greater delivery certainty but requiring more complex grid arrangements

The right structure depends on grid constraints, basis risk tolerance, and whether the buyer's sustainability framework requires hourly matching — making procurement advisory a critical step before signing.

What These Trends Mean for Indian C&I Buyers

While global headwinds are real, India's renewable energy buildout continues at scale. As of November 2025, India's total renewable installed capacity reached 253.96 GW, including 132.85 GW of solar and 53.99 GW of wind. Indian C&I buyers in steel, cement, textiles, manufacturing, and data centers are increasingly turning to long-term renewable procurement as a hedge against grid tariff volatility and as part of ESG commitments.

The Indian Open Access Surge

India added 7.8 GW of solar open access capacity in 2025, pushing cumulative installed capacity past 30 GW. The pipeline remains massive, with more than 45 GW of solar open access projects under development. This growth is concentrated in Karnataka, Maharashtra, Rajasthan, Gujarat, and Tamil Nadu, which collectively contribute over 85% of installations.

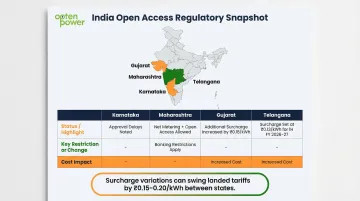

Navigating State-Level Complexity

Indian C&I procurement faces unique challenges due to state-level regulatory variations:

- Karnataka led 2025 installations, though green energy open access approval delays continue to slow project timelines

- Maharashtra provided clarity by allowing simultaneous net metering and open access, though energy banking restrictions remain

- Gujarat increased the additional surcharge for open access consumers by ₹0.18/kWh, narrowing developer margins

- Telangana set an additional surcharge of ₹0.13/kWh for 1H FY 2026-27, adding cost pressure that buyers need to factor into landed tariff comparisons

These state-level variations make direct cost comparison difficult — the surcharge alone can swing landed tariffs by ₹0.15–0.20/kWh between states. Platforms providing real-time DISCOM intelligence with standardized landing prices across states give C&I buyers a clearer view of true costs and where the best procurement opportunities actually sit.

The Strategic Procurement Imperative

For Indian businesses, energy procurement deserves the same rigor as any capital allocation decision — with clear cost reduction targets, ESG reporting requirements, and long-term price certainty built in from the start. Opten Power's marketplace gives buyers access to 4+ GW of capacity across 16 states, with tools to compare tariffs, model IRR and payback periods, and close deals up to 50% faster than going developer-by-developer. That kind of structured approach is what separates businesses locking in cost advantages now from those still reacting to the next tariff revision.

Frequently Asked Questions

What is renewable energy procurement and how does it work?

Renewable energy procurement is the process by which businesses contract to purchase electricity from renewable sources like solar, wind, or hydro. It works through Power Purchase Agreements (PPAs), green tariffs, or open access arrangements — covering both physical delivery and virtual/financial settlement structures.

What is a Corporate PPA and why are companies signing them?

A Corporate Power Purchase Agreement (PPA) is a long-term contract between a renewable energy developer and a corporate buyer. Companies sign them to lock in predictable electricity prices, directly support new renewable capacity, and establish credible paths to meet ESG and decarbonization goals.

Why did global corporate clean energy buying fall in 2025?

Rising project costs across solar, onshore wind, and offshore wind, combined with policy uncertainty in key markets, caused the first year-on-year decline in nearly a decade. While the Americas held steady at 29.5 GW driven largely by Big Tech hyperscalers, Europe and Asia-Pacific experienced significant volume drops.

What are co-located and hybrid renewable energy deals?

Co-located deals pair renewable generation (typically solar) with battery storage at the same site, enabling firms to deliver power at more predictable times. Global battery costs fell 27% to a record $78/MWh in 2025, making these hybrid structures increasingly standard in corporate procurement.

What are the biggest barriers to efficient renewable energy procurement today?

The primary barriers are fragmented systems (averaging 3.8 disconnected tools), poor process transparency, and manual correspondence management. Only 37% of organizations globally rate their procurement processes as "very efficient," leaving most unable to meet the accountability standards investors and regulators require.

How can Indian businesses start procuring renewable energy more effectively?

Indian C&I businesses should assess their energy load profile, understand state-level open access regulations and DISCOM tariffs, and use a unified marketplace platform to compare developer offerings, model financial returns, and manage the full procurement lifecycle in one place — cutting deal closure time by up to 50%.