Introduction

For India's commercial and industrial (C&I) businesses, the electricity bill is no longer just an operating cost — it's a strategic liability. Grid tariffs have climbed steadily, with industrial rates now ranging from ₹4.80 to ₹8.36 per unit across states, alongside volatile peak demand charges and tightening sustainability mandates. Solar PPAs offer a direct hedge: fixed tariffs locked in for 10–25 years, with no upfront capital and predictable savings from day one.

But choosing the wrong PPA partner can be just as costly as staying on the grid. The decision is simultaneously operational, financial, and regulatory — and getting it wrong means years locked into unfavourable terms.

This guide covers what you need to evaluate:

- Which developers have the strongest track records across Indian states

- What contract clauses separate reliable PPAs from risky ones

- How to compare tariffs, savings, and risk provisions across multiple offers

- What to look for in 2026 given updated regulatory and DISCOM dynamics

Key Takeaways

- A solar PPA lets C&I businesses source solar power from a developer-owned plant with zero upfront capital, paying only for units consumed at a pre-agreed tariff under India's open access framework

- India's top solar PPA providers are compared here on capacity, geographic reach, tariff competitiveness, and C&I track record

- Key companies include Tata Power Solar, CleanMax Solar, Amplus Solar (Gentari), Hero Future Energies, and ReNew Power

- C&I businesses in manufacturing, data centers, hospitality, and heavy industry typically cut energy costs 20–40% through a well-structured corporate PPA

- The selection criteria and company profiles below support shortlisting and RFP preparation

What Is a Solar PPA and Why Are India's C&I Businesses Adopting It?

A solar PPA (Power Purchase Agreement) is a long-term contract — typically 10 to 25 years — where a developer finances, builds, and operates a solar asset while the business pays a fixed or escalating tariff per unit consumed. The business carries no capital expenditure, no ownership burden, and no maintenance obligations.

India's C&I Solar Market in 2026

India added 7.8 GW of solar open access capacity in 2025, bringing cumulative solar open access capacity to over 30 GW by year-end. The open access segment now represents a significant share of India's total solar installations, with C&I consumers driving growth through direct renewable energy procurement.

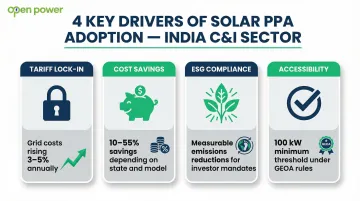

Key adoption drivers:

- Locks in tariff rates while grid costs escalate 3-5% annually, giving multi-year cost predictability

- Delivers 10-55% savings depending on state and PPA model, with higher-tariff states seeing the largest benefit

- Satisfies investor and board-level ESG pressure to demonstrate measurable emissions reductions

- Becomes accessible to smaller buyers after Green Energy Open Access Rules dropped the eligibility threshold from 1 MW to 100 kW

The five companies profiled below cover the range of what's available to C&I buyers in 2026 — from large IPPs with pan-India open access footprints to specialized developers with strong regional track records. Each was evaluated on contracted C&I capacity, multi-state credentials, financial backing, and verified tariff delivery.

Top Solar PPA Companies & Installers in India for 2026

These five companies were shortlisted based on installed C&I PPA capacity, multi-state open access credentials, financial backing, client portfolio size, and track record of delivering contracted tariff savings.

Tata Power Solar

Background: Tata Power Solar, through Tata Power Renewable Energy Limited (TPREL), operates one of India's largest integrated solar portfolios. As of FY 2024-25, TPREL's total renewable portfolio stands at 10.9 GW, including 5.4 GW under implementation.

Its rooftop solar business has achieved 3 GWp in the C&I segment, with 254 MWp commissioned across 3,778 C&I installations in FY 2025-26.

Standout: TPREL has surpassed 1.5 GW in group captive project capacity, making it a leader in this procurement model. Notable contracts include a 379 MW captive solar-wind hybrid PPA with Tata Steel for 25 years and a 131 MW wind-solar hybrid PPA with Tata Motors structured as a co-investment.

Tata Group backing provides clear bankability advantages for long-tenor contracts — a key consideration for C&I buyers committing to 25-year agreements.

| Parameter | Details |

|---|---|

| PPA Structure | Captive, Third-Party, and Group Captive models across Maharashtra, Gujarat, Rajasthan, Karnataka, Madhya Pradesh, and Chhattisgarh |

| Typical Tenure & Tariff Range | 15-25 years; tariffs range from ₹2.75/kWh (utility-scale solar) to ₹3.6/kWh (hybrid projects) |

| Capacity Range & States Active | Minimum 100 kW (per GEOA rules); active in 6+ states with open access approvals |

CleanMax Solar

Background: CleanMax is India's largest C&I renewable energy provider, specializing in net-zero and decarbonization solutions through onsite and offsite solar, wind, and hybrid projects. As of March 2026, CleanMax's total contracted capacity reached 5.7 GW, with 3.0 GW operational.

Standout: CleanMax serves over 500 corporate clients across data centers, AI/technology, cement, steel, FMCG, pharmaceuticals, and automotive sectors. Notable clients include Amazon, Google, Cisco, Equinix, CEAT, and BASF.

The company holds the largest geographic reach among C&I players, with STU-connected farms in 10 states and upcoming CTU-connected farms for pan-India supply. A recent highlight: a 33 MW captive wind-solar hybrid PPA with Equinix for its Mumbai data centers.

| Parameter | Details |

|---|---|

| PPA Structure | Group captive and third-party open access models; strong focus on hybrid (solar + wind) solutions |

| Typical Tenure & Tariff Range | Weighted average tenure of 22.85 years; tariffs competitive with state-specific open access benchmarks |

| Capacity Range & States Active | Projects from 10 MW to 100+ MW; active in 10 states including Gujarat, Karnataka, Maharashtra, Tamil Nadu, Haryana, Rajasthan |

Amplus Solar (A Member of Gentari)

Background: Originally backed by I Squared Capital, Amplus Solar was acquired by Malaysia's PETRONAS in 2019 and fully integrated under Gentari in May 2025. As of May 2025, the platform had over 2.4 GW of operational and under-construction distributed energy assets, serving over 350 multinational firms across automotive, industrial, technology, consumer goods, and hospitality.

Standout: Amplus/Gentari specializes in distributed renewable energy with a strong presence in Rajasthan, Maharashtra, and Karnataka. A notable project is a 360 MWp ISTS solar plant in Bikaner, Rajasthan, supplying power to C&I clients nationwide. The company is also developing India's first integrated on-site solar-wind-battery storage project, commissioned in 2025, designed to eliminate curtailment risk for round-the-clock C&I supply.

| Parameter | Details |

|---|---|

| PPA Structure | Group captive (64% developer stake, 26% C&I stake), BOOT model for rooftops, third-party open access |

| Typical Tenure & Tariff Range | 10-25 years; fixed tariffs from ₹3.20/unit (group captive solar) to ₹4.4/unit (rooftop portfolios) |

| Capacity Range & States Active | Minimum 100 kW; strong presence in Rajasthan, Maharashtra, Karnataka with pan-India ISTS connectivity |

Hero Future Energies

Background: Hero Future Energies (HFE) is an Independent Power Producer with a strong focus on complex, high-CUF hybrid and storage-integrated projects. As of March 2025, HFE's total portfolio stood at 6.5 GWp of renewable capacity plus 2 GWh of Battery Energy Storage Systems.

Standout: HFE's India C&I portfolio totals 709 MWp, with all under-construction and development projects structured under the group captive model. The company specializes in Firm and Dispatchable Renewable Energy (FDRE), Round-the-Clock (RTC), and Peak Power projects integrating solar, wind, and storage. HFE secured a 120 MW FDRE project from SJVN at ₹4.25/kWh and commissioned India's first commercial-scale green hydrogen blending project for automotive client Rockman Industries.

| Parameter | Details |

|---|---|

| PPA Structure | Group captive model; specializes in hybrid (solar + wind + storage) for round-the-clock power supply |

| Typical Tenure & Tariff Range | 15-25 years; FDRE/RTC projects priced at ₹4.25-4.38/kWh, reflecting premium for firm power |

| Capacity Range & States Active | Minimum 100 kW; operational in Karnataka, Andhra Pradesh, Telangana, Rajasthan; expanding in Maharashtra, Haryana |

ReNew Power

Background: Listed on NASDAQ (RNW), ReNew is one of India's largest renewable energy IPPs, backed by Goldman Sachs, Canada Pension Plan Investment Board (CPPIB), and Abu Dhabi Investment Authority (ADIA). As of May 2024, ReNew's total portfolio was 15.6 GW, with ~9.5 GW operational.

Standout: ReNew's dedicated C&I arm, ReNew Green Solutions, manages a committed portfolio of 2.7 GW, serving over 80 corporate clients including Amazon and Google. Its pan-India presence spans 10 states, with the bulk of capacity in Rajasthan (46%), Karnataka (14%), and Maharashtra (11%).

ReNew's PPAs include performance guarantees and irrevocable bank guarantees — structural protections that matter for offtakers signing long-tenor deals. The company recently signed a 1 GW FDRE PPA with SJVN at ₹4.39/kWh.

| Parameter | Details |

|---|---|

| PPA Structure | Captive, third-party, and group captive models; flexible structures with CTU and STU connectivity |

| Typical Tenure & Tariff Range | 3-25 years (majority 25 years); corporate solar ₹2.81-5.66/kWh, corporate wind ₹3.35-6.32/kWh, corporate hybrid ₹3.16-3.81/kWh |

| Capacity Range & States Active | Minimum 100 kW; active in 10 states with over 23 GW of interconnection capacity secured for future growth |

Key Factors to Consider Before Signing a Solar PPA in India

Understanding PPA Structural Models

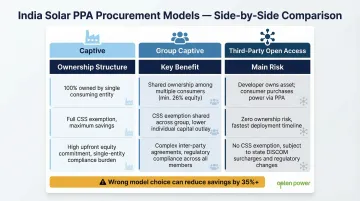

Three procurement models dominate India's C&I solar market, each with distinct regulatory treatment under the Electricity Act, 2003:

| Model | Ownership Structure | Key Benefit | Watch Out For |

|---|---|---|---|

| Captive | End-user owns ≥26% equity, consumes ≥51% of generation | Exempt from Cross-Subsidy Surcharge (CSS) | Requires upfront equity participation |

| Group Captive | Multiple consumers form an SPV; 26%/51% thresholds apply collectively (±10% variation) | CSS exemption shared across group | Consumption must stay proportional to ownership share |

| Third-Party Open Access | Developer owns 100%; no consumer equity required | Zero upfront investment | Attracts full open access charges including CSS and Additional Surcharge |

Choosing the wrong structure can cost more than it saves. A 100 kW consumer in Maharashtra might cut bills by 50% under a captive model — but only 15% under third-party open access once CSS charges apply.

State-Wise Open Access Charges Vary Dramatically

Open access charges — wheeling, transmission, cross-subsidy surcharge, and banking charges — vary significantly by state and can reduce PPA savings by 30-60%. Net landed costs for open access power in Q4 2025 ranged from under ₹5/kWh to over ₹8.4/kWh across states.

Sample state-wise charges (FY 2024-25):

| State | Wheeling Charges (₹/kWh) | Cross-Subsidy Surcharge (₹/kWh) | Additional Surcharge (₹/kWh) |

|---|---|---|---|

| Maharashtra | HT: 0.60, LT: 1.17 | Varies by category | - |

| Karnataka | HT: 0.29, LT: 0.67-0.68 | HT Industrial: 2.08 | - |

| Rajasthan | HT (11kV): 0.62 | HT Industrial: 1.58 | 0.72 |

| Gujarat | HT: 0.63, LT: 1.00 | HTMD-1: 1.53 | - |

These numbers matter more than the headline tariff. A PPA quoted at ₹3.50/kWh might land at ₹6.20/kWh after regulatory charges in one state — but only ₹4.80/kWh in another. Platforms like Opten Power provide real-time DISCOM intelligence so businesses can compare true landed costs across states before signing anything.

Contract-Level Risk Factors C&I Buyers Often Overlook

State charges are only half the picture — the contract itself carries risks most C&I buyers don't examine until it's too late. Before signing, scrutinize these four clauses:

- Escalation rate: Most PPAs include 1-3% annual tariff escalation. A ₹3.50/kWh rate at 2% annual escalation reaches ₹5.19/kWh by year 20 — factor this into your long-term cost model.

- Deemed generation provisions: If your plant goes offline for maintenance or your consumption drops, many PPAs still require payment for unconsumed power. Confirm exactly how curtailment is handled.

- Exit penalties: Early termination is calculated on remaining contracted generation or outstanding project debt. A 10-year exit from a 25-year PPA can run ₹2-5 crore depending on project size.

- Developer sale rights: If the developer sells the project mid-PPA, do you have consent rights? Confirm whether performance guarantees transfer to the new owner automatically.

How We Chose the Best Solar PPA Companies

Each company on this list was evaluated across five criteria:

- Total C&I PPA capacity contracted

- Multi-state open access approvals

- Client diversity across industrial verticals

- Financial credibility of the developer entity

- Availability of flexible PPA structures (captive, third-party, group captive)

Common mistakes C&I buyers make:

- Quoted tariff ≠ landed cost: a ₹3.20/kWh PPA can reach ₹5.80/kWh once wheeling charges, CSS, and transmission fees are added

- Commissioning delays void tariff commitments, pushing buyers back to full-price grid power — always check the developer's on-time track record

- Exit and curtailment clauses determine how much flexibility you have if business conditions shift — skipping legal review here is a costly oversight

The evaluation surfaces developers with genuine regulatory competence, financial stability, and fair contract terms — the three factors that determine whether a PPA actually delivers its projected savings.

Conclusion

Selecting a solar PPA partner in India goes beyond the per-unit tariff. It requires vetting the developer's financial standing, state-wise regulatory competence, and ability to deliver on contracted generation over a 15–25 year horizon.

Before shortlisting, compare multiple developer proposals against standardized criteria:

- Open access charge benchmarks by state

- Escalation structure and rate caps

- Curtailment protections and grid reliability terms

A rigorous evaluation now prevents costly surprises across a decade-plus contract.

Ready to compare PPA proposals? Opten Power lets C&I businesses run IRR and payback analysis, benchmark landed costs across states, and connect with pre-vetted solar developers — all on one platform built for procurement across 16 states.

Frequently Asked Questions

What is a solar PPA and how does it work for commercial businesses in India?

A solar PPA is a long-term agreement where a developer builds and owns the solar plant while the business pays only for consumed units at a locked-in tariff, with no upfront capital required. The developer handles financing, construction, operation, and maintenance for 10-25 years.

Are solar PPAs worth it, and how do they compare to buying solar panels?

PPAs eliminate capex and O&M responsibility but offer no ownership benefits or depreciation. Buying panels delivers better long-term ROI and asset ownership, but requires upfront capital (₹4-6 crore per MW) and active management. PPAs suit businesses prioritizing cash flow; capex suits those with capital availability and long-term facility ownership.

What is the difference between captive solar and third-party PPA in India?

Captive solar requires the consumer to hold at least 26% equity and consume 51% of generation — this qualifies for CSS exemption under the Electricity Act. Third-party PPAs involve zero consumer ownership; the developer retains full ownership but you bear full open access charges, including CSS and Additional Surcharge, which can significantly raise your landed cost.

How are solar PPA tariffs structured in India, and what charges affect the final landed cost?

PPA tariffs are fixed or escalating per-unit rates (₹2.75-5.66/kWh depending on technology and structure). The actual landed cost adds wheeling (₹0.29-1.17/kWh), transmission (₹0.12-0.62/kWh), cross-subsidy surcharge (₹1.53-2.08/kWh for third-party), and banking charges that vary by state and can add ₹1.50-4.00/kWh to the base tariff.

What is the typical contract duration for a solar PPA in India?

Most C&I solar PPAs in India range from 10 to 25 years, with tariff escalation clauses typically set at 1-3% per year. Longer tenures generally offer lower base tariffs (₹2.75-3.50/kWh for 25 years vs. ₹4.00-5.00/kWh for 10 years) but lock businesses into extended commitments.

Can a business exit a solar PPA agreement before the contract ends?

Early exit is possible but typically incurs significant penalties based on remaining contracted generation or outstanding project debt. For a 10-year exit from a 25-year, 5 MW PPA, expect penalties in the range of ₹2-5 crore. Review exit provisions carefully before signing — some developers calculate penalties on deemed generation rather than actual consumption.