Introduction

Solar developers and financiers in India commit capital for 15–25 year Power Purchase Agreement (PPA) contracts. A commercial buyer's creditworthiness is often the single most decisive factor in whether a deal gets signed, priced favourably, or rejected entirely.

Most buyers focus on tariff rates and savings potential. Few realise that developers are simultaneously evaluating the buyer's financial stability, consumption reliability, and legal standing before committing to any project.

The stakes are significant. India's commercial and industrial (C&I) sector added 7.8 GW of solar open access capacity in 2025, with over 45 GW in the development pipeline. Yet deal execution faces persistent friction:

- Transmission constraints limiting project viability

- Land acquisition hurdles delaying timelines

- DISCOM reluctance to grant open access approvals

Beyond these structural barriers, counterparty due diligence failures during the creditworthiness assessment phase cause significant deal restructuring or outright rejection. Industry reports confirm that a buyer's financial health, regulatory compliance, and load consistency are primary evaluation criteria — yet these factors rarely receive the attention they deserve.

This guide breaks down exactly what solar developers and financiers assess when evaluating a commercial buyer — so you can enter negotiations prepared.

Key Takeaways

- Creditworthiness assessment evaluates whether a business can meet a 15–25 year solar PPA without default risk

- Key parameters include DSCR (minimum 1.20x average), debt-equity ratio (typically 70:30 max), load stability, business tenure, and open access eligibility

- Weak profiles trigger higher tariffs, shorter tenors, larger security deposits, or outright rejection

- Buyers improve their standing by clearing DISCOM arrears, submitting 24-month load history, and resolving property encumbrances

- Platforms like Opten Power accelerate due diligence with real-time DISCOM intelligence and pre-approved contract templates

What Is Commercial Solar Creditworthiness — and Why Does It Matter?

Commercial solar creditworthiness is a structured assessment of a business's financial, operational, and legal capacity to honour a long-term solar PPA obligation — typically spanning 15 to 25 years — without default or early termination risk. Unlike traditional bank lending that focuses primarily on balance sheet strength, solar PPA creditworthiness goes further. It incorporates energy consumption behaviour, regulatory compliance history, and site-level factors alongside conventional financial metrics.

Why it matters from both sides:

For the developer and financier, creditworthiness determines project bankability and the ability to raise debt. Lenders like IREDA and SBI prioritise PPAs with strong off-takers (A+ rated or higher) to minimise payment delay risks — historically prevalent with state DISCOMs. To cover this exposure, financiers require security packages that typically include:

- Trust and Retention Accounts (TRA) to ringfence project cash flows

- Escrow mechanisms ensuring payment priority to lenders

- Debt Service Reserve Accounts (DSRA) providing a liquidity buffer against missed payments

For the C&I buyer, creditworthiness directly influences the PPA tariff offered, the contract terms, and whether security deposits or parent guarantees are demanded. A strong profile unlocks better pricing and flexible terms; a weak one narrows options or closes doors entirely.

Key Parameters Used to Evaluate Commercial Solar Creditworthiness

Financial Health Indicators

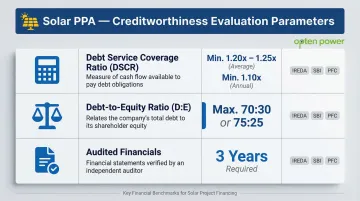

Developers and their financiers examine audited financials for at least 2–3 years, focusing on specific ratios that indicate debt serviceability and financial resilience.

| Financial Parameter | Benchmark Requirement | Source |

|---|---|---|

| Debt Service Coverage Ratio (DSCR) | Minimum average 1.20x to 1.25x; minimum annual 1.10x | IREDA, SBI |

| Debt-to-Equity Ratio | Typically capped at 70:30 or 75:25 | IREDA, PFC |

| Audited Financial Statements | 3 years required for appraisal | Standard across lenders |

Weak metrics trigger demand for additional credit enhancements like bank guarantees, higher security deposits, or parent company guarantees. For example, a buyer with a DSCR below 1.15x may still qualify but will face stricter terms — shorter initial contract periods, higher upfront deposits, or stepped payment structures.

Energy Consumption Profile and Load Stability

Monthly energy consumption data — typically 12–24 months of electricity bills or DISCOM records — is used to verify that the buyer has consistent, predictable load. Developers analyse:

- Load factor (average vs. peak load) and how closely it tracks solar generation hours

- Month-to-month consumption volatility and seasonal swings

- Planned capacity expansions or contractions over the PPA term

Volatile or seasonally dependent loads create revenue uncertainty for the developer, often resulting in conservative contract sizing or penalty clauses. Industries with 24x7 operations — such as steel, cement, textiles, data centres, and hospitals — are viewed more favourably due to stable baseload demand.

Business Tenure, Sector Stability, and Operational Continuity

A company's years of operation, sector classification, and likelihood of continued operations over the PPA term are critical evaluation factors.

| Industry Sector | Share of Open Access Offtake (2024) |

|---|---|

| Steel / Iron | 33.2% |

| Data Centres / IT | 13.6% |

| Cement | 12.4% |

| Mining | 11.9% |

| Chemicals / Petrochemicals | 10.0% |

Textile manufacturers achieve 20–30% savings through open access, making them attractive counterparties. Startups or businesses in volatile sectors face greater scrutiny, often requiring parent guarantees or shorter initial contract periods with renewal options.

Legal and Ownership Structure

Legal due diligence covers four core areas:

- Ownership title or a long-term lease (minimum 20 years preferred) on the facility where solar assets will be sited

- Clean property title — no encumbrances, active litigation, or disputed ownership

- Entity type entering the PPA: limited companies generally carry lower risk than partnership firms

- Parent company financials, which become relevant when the contracting subsidiary has limited operating history

Open Access Eligibility and Regulatory Compliance

The Ministry of Power's Green Energy Open Access (GEOA) Rules 2022 reduced the minimum eligibility threshold from 1 MW to 100 kW, expanding market access significantly.

| State | Contracted Demand Threshold |

|---|---|

| National (GEOA 2022) | 100 kW |

| Maharashtra | 100 kW |

| Karnataka | 100 kW |

| Gujarat | 100 kW |

| Rajasthan | 100 kW |

| Andhra Pradesh | 100 kW |

| Tamil Nadu | 63 kVA (EHT/HT consumers) |

Beyond threshold eligibility, three compliance factors shape the credit view:

- DISCOM payment history — outstanding arrears or active billing disputes can stall open access approvals

- Energy banking headroom — GEOA rules cap banked energy at 30% of monthly consumption, limiting flexibility for variable loads

- State-level CSS and Additional Surcharges (AS) — these directly affect the landed cost advantage and vary significantly by state

For example, Gujarat increased its AS by 22% in Q4 2025 (from ₹0.82/kWh to ₹1.00/kWh), narrowing developer margins and affecting buyer economics. Maharashtra's revised Time-of-Day (ToD) banking rules restrict drawal of banked energy to the same or lower tariff time blocks, complicating consumption planning.

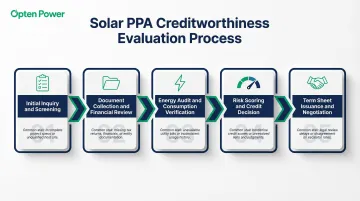

How the Creditworthiness Evaluation Process Works – Step by Step

Here are the five stages a commercial buyer moves through during creditworthiness due diligence — and where delays most commonly occur.

Step 1 – Initial Inquiry and Preliminary Screening

The buyer submits basic information: industry type, contracted load, location, annual energy consumption, and DISCOM utility details. The developer or platform conducts a quick-check against open access eligibility criteria and blacklisted sectors.

Common stall point: Deals most frequently stall here when buyers don't know their contracted demand or have pending DISCOM arrears. Clearing these issues before approaching developers accelerates the process.

Step 2 – Document Collection and Financial Review

A formal documentation request is issued covering:

- 2–3 years of audited financial statements

- Board resolutions authorising the PPA

- Entity incorporation documents

- Property ownership or long-term lease deeds

- Electricity bills (12–24 months)

Evaluators calculate DSCR, net worth, and debt obligations. Incomplete or outdated documents at this stage are the leading cause of timeline delays. Having these documents prepared in advance can cut review time by two weeks or more.

Step 3 – Energy Audit and Consumption Profile Verification

Electricity bills and DISCOM data are analysed to map consumption patterns, peak load hours, load factor, and seasonal variations. For manufacturing clients, shift schedules and planned capacity expansions may also be reviewed.

This step determines the bankable system size and whether shadow tariff modelling holds up. Buyers with erratic consumption patterns typically face one of two outcomes:

- Conservative sizing — systems undersized to ensure full offtake

- Penalty clauses — contractual charges triggered by under-consumption

Step 4 – Risk Scoring and Credit Decision

The developer's risk team or the financing institution assigns a credit score or risk band based on aggregated financial, operational, and regulatory inputs. This score determines:

- PPA tariff (risk premium)

- Contract tenor

- Security deposit requirements (typically 3–6 months of expected payments)

- Additional covenants (e.g., step-in rights, parent guarantees)

Platforms and developers use proprietary risk matrices, but the core inputs are consistent across evaluators: financial ratios, load stability, sector risk, and regulatory compliance. Once the credit band is assigned, it directly triggers the terms offered in the next step.

Step 5 – Term Sheet Issuance and Negotiation

A conditional term sheet is issued outlining the offered PPA rate, contract term, performance obligations, and credit enhancement requirements. Both parties negotiate and resolve open items before a final LOI or PPA is executed.

Common mistake: Buyers often overlook security deposit and termination clauses. Understanding these provisions upfront — particularly step-in rights and accelerated termination conditions — prevents surprises later.

A Practical Walkthrough: Creditworthiness Assessment for a C&I Buyer

Consider a mid-sized textile manufacturer in Maharashtra seeking a 2 MW open access solar PPA. Here's how the developer screens their application at each step:

Initial Screening:

- Contracted demand: 2.5 MW (eligible under 100 kW threshold)

- Industry: Textiles (favourable — 24x7 operations)

- DISCOM account: Clean, no arrears

- Result: Passes preliminary screening

Financial Review:

- Years in operation: 10 years (strong tenure)

- DSCR: 1.18x average (slightly below 1.20x benchmark due to recent capex debt)

- Debt-to-Equity: 68:32 (within acceptable range)

- Result: Moderate financial profile — flagged for credit enhancement

Energy Audit:

- Load factor: 0.72 (stable)

- Seasonal variation: <15% (predictable)

- Consumption: 1.8 MW average baseload

- Result: Strong consumption profile supports full 2 MW system

Credit Decision:

The developer offers a PPA tariff of ₹3.85/kWh — slightly above the ₹3.70/kWh offered to A-rated buyers — and requests a 6-month security deposit equivalent. The deal proceeds on a 15-year contract term.

That outcome changes sharply when the profile deteriorates. If the same buyer had DISCOM arrears of ₹5 lakh and unresolved property litigation, the developer would likely reject outright or demand a parent company guarantee plus a 12-month security deposit. At that point, the economics stop working.

Knowing your creditworthiness profile before approaching developers lets you close gaps early — and that translates directly into faster deal timelines and better tariff pricing.

Common Pitfalls and How to Strengthen Your PPA Creditworthiness Profile

Most common disqualifying or deal-delaying issues:

- Unresolved DISCOM dues or disputes

- Inconsistent energy consumption records or missing bills

- Property ownership disputes or short-lease tenure (<10 years remaining)

- Outdated financials (older than 12 months)

- Lack of awareness about open access eligibility thresholds in the buyer's state

Practical steps to strengthen your profile:

- Clear DISCOM arrears before approaching developers — even small outstanding amounts can stall or kill deals

- Compile 24 months of electricity bills to demonstrate stable load history

- Ensure lease agreements extend beyond the PPA tenor — short tenure is one of the most common deal blockers

- Prepare a board-authorised entity profile, including your incorporation certificate and board resolution

- Map state-specific open access norms upfront: banking limits, cross-subsidy surcharge, and additional surcharge vary significantly by state

Once documentation is in order, the next challenge is finding developers whose risk appetite matches your profile — and negotiating on equal footing.

Opten Power's marketplace provides real-time DISCOM intelligence across 16 states and pre-approved contract templates, so buyers can assess eligibility, prepare documentation in days, and match with developers suited to their risk profile. Most users close deals up to 50% faster than the traditional procurement route.

How Opten Power Can Help

Opten Power is India's unified clean energy marketplace, built specifically for C&I buyers navigating the creditworthiness evaluation process from preparation through PPA closure. With 4+ GW of renewable capacity across 16 states, the platform gives buyers the data and tools to approach developers from a position of strength.

Key capabilities for C&I buyers include:

- Real-Time DISCOM Intelligence — Standardised landing prices across all states let buyers verify open access eligibility and compliance standing before approaching any developer.

- Automated RFP Engine — Modular templates speed up tender creation and bid collection, while pre-approved contract templates cut negotiation time on legal and commercial terms.

- Transparent Tariff Comparison — Compare PPA terms, IRR, and projected savings across multiple developers in real time, so you know exactly what your creditworthiness profile qualifies for before the first conversation.

- Portfolio Management Dashboard — Track performance, savings, and compliance across all renewable projects from one interface.

To assess your PPA eligibility and get matched with the right developer, contact Opten Power at +91 78959 41766 or visit the platform to start your first evaluation.

Frequently Asked Questions

What is the 20% rule for solar?

There is no uniform national "20% rule" limiting solar injection or consumption for C&I open access. The GEOA Rules 2022 actually stipulate that permitted banked energy shall be at least 30% of total monthly consumption from the distribution licensee. State implementations vary; for example, Rajasthan limits banking to 25% of injected energy or 30% of consumption, whichever is higher.

What is a good PPA rate?

A good PPA rate for commercial buyers in India delivers 25–30% savings against the applicable DISCOM tariff. C&I open access tariffs run higher than utility-scale benchmarks (such as Karnataka's 2025–2026 rate of ₹3.07/kWh) due to surcharges and smaller project scales. The rate you're offered depends on your creditworthiness profile and contract tenor.

What financial documents are typically required for a commercial solar PPA creditworthiness evaluation?

Standard documents include: 2–3 years of audited financial statements, entity incorporation certificate, property ownership or long-term lease deed, recent electricity bills (12–24 months), board resolution authorising the PPA, and any existing loan or encumbrance documents. Having these prepared in advance speeds up the review process.

Can a growing or mid-sized company qualify for a solar PPA?

Yes, mid-sized companies can qualify, but may face stricter terms — shorter contract periods, higher security deposits (6–12 months), or parent guarantee requirements — if financials show high leverage or DSCR below 1.20x. Stable load and business continuity often offset moderate financial metrics, especially in textiles, manufacturing, or hospitality.

How does poor creditworthiness affect PPA pricing and contract terms?

Poor creditworthiness raises costs and tightens terms across the board. Typical impacts include:

- Higher PPA tariff — risk premium of ₹0.15–₹0.30/kWh above market rates

- Shorter contract tenor — 10 years instead of 15–20 years

- Larger security deposits — 12 months upfront instead of 3–6 months

- Developer-protective clauses such as step-in rights or accelerated termination

Each of these reduces the buyer's net savings and overall ROI.