Introduction

When a commercial or industrial (C&I) buyer in India signs a Green Power Purchase Agreement, they're committing to a 15–25 year contract worth hundreds of crores—making it one of the largest operational decisions a business will make. For context, C&I renewable capacity is projected to surge 40% to reach 57 GW by FY28, with deals like Tata Power's recent ₹105 crore group captive solar PPA representing the scale of these commitments.

Yet many buyers focus exclusively on the headline tariff per kWh and overlook the clauses that determine financial exposure when the renewable plant underperforms, when regulations change, or when the buyer needs to exit early. A poorly negotiated deemed generation clause or an uncapped escalation rate can erode projected savings by 20–30% over the contract term.

Before signing, every C&I buyer should examine six critical clause-clusters:

- Financial clauses — tariff structure, contracted volume, payment security

- Operational clauses — scheduling, banking, deemed generation

- Risk and exit clauses — default, termination, force majeure, curtailment

- Regulatory clauses — change-in-law, RECs, open access approvals

Understanding these provisions upfront protects your bottom line for decades.

TLDR: Key Clauses in a Green PPA at a Glance

- Uncapped escalations can erase initial tariff benefits within 5–7 years—check price and escalation caps first

- Generation volume and banking provisions must match your actual consumption pattern, or you'll pay for energy you can't use

- Deemed generation and curtailment clauses shift cost liability when plants underperform or grid operators curtail output

- Default, termination, and force majeure clauses define your exit options—early termination can trigger NPV payments worth ₹ crores

- Change-in-law clauses shield you from regulatory cost shifts; REC ownership terms protect your ESG claims across states

Financial Clauses: Tariff, Volume, and Payment Security

Contract Price and Escalation

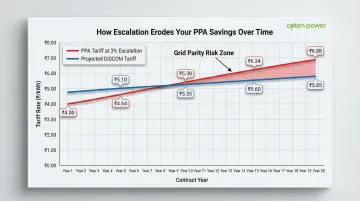

The contract price—expressed in ₹/kWh—is the fixed rate you pay for each delivered unit. But the base rate tells only half the story. Most Indian C&I Green PPAs include an annual escalation factor, typically 0–3%, that compounds over the contract term.

A PPA with a ₹4.00/kWh base rate and 3% annual escalation will reach ₹6.88/kWh by Year 20—a 72% increase. If grid tariffs rise more slowly or state policies drive down DISCOM rates due to surplus renewable capacity, your "competitive" PPA becomes a liability. Model escalation scenarios against projected DISCOM tariff trends for your state before accepting any escalation clause.

Current tariff benchmarks: Recent SECI wind-solar hybrid auctions discovered tariffs between ₹3.15 and ₹3.69/kWh, while some state tenders remain slightly higher. When evaluating offers, use platforms like Opten Power to compare real-time tariffs across multiple developers before issuing an RFP—so your benchmarks reflect current market conditions.

Annual Energy Generation Volume

This clause defines the contracted quantity (MWh/year) the seller commits to deliver. Two structures dominate:

- Take-or-pay: You pay for the contracted volume regardless of consumption, creating exposure during plant shutdowns or demand slowdowns

- Pay-as-produced: You only pay for energy actually generated and delivered

Most C&I buyers size contracted volumes at 70–80% of baseload consumption to avoid overpaying. For example, a manufacturing plant with 50 GWh annual consumption should contract for 35–40 GWh, covering steady daytime baseload while leaving headroom for demand variability and avoiding excess payment liability.

Sizing too aggressively (90–100% of consumption) creates two distinct risks:

- Paying for energy you can't use when production slows

- Losing banked energy if state banking windows don't allow full annual rollover

Payment Security Mechanism

To protect revenue certainty, most renewable PPAs in India require buyers to provide a payment security instrument—typically a Letter of Credit (LC) covering 1–3 months of contracted billing. For a 10 MW solar PPA at ₹4/kWh with 20% CUF, monthly billing is approximately ₹57.6 lakh, requiring an LC of ₹57.6 lakh to ₹1.73 crore.

This directly impacts working capital. Buyers with strong credit ratings can negotiate reduced LC tenure or substitute with alternative instruments, including:

- Performance bonds or escrow arrangements

- Payment on Order Instruments (POIs) issued by IREDA, PFC, or REC—now recognized by MNRE and SECI as valid alternatives to traditional bank guarantees

The POI route offers meaningful flexibility for creditworthy C&I buyers looking to free up working capital without weakening the seller's revenue security.

Negotiate clear invocation triggers into the contract—such as payment default beyond a defined cure period—to prevent arbitrary LC invocation.

Operational Clauses: Contract Profile, Banking, and Deemed Generation

Contract Profile and Scheduling

The contract profile defines the hourly, daily, or monthly shape of energy delivery. For industrial buyers with high daytime loads, a solar PPA profile aligns well—but mismatch during non-solar hours creates "short" positions requiring grid top-up at higher DISCOM tariffs.

India's Deviation Settlement Mechanism (DSM) penalizes buyers for scheduling errors. Under CERC DSM Regulations 2022, compensation for over-injection is eliminated beyond 10%—making accurate generation scheduling non-negotiable.

Manufacturing plants running 24x7 should negotiate a hybrid solar-wind profile to improve round-the-clock matching and reduce DSM exposure. A well-drafted scheduling clause must specify:

- Process for submitting generation schedules to the SLDC

- Lead time required for schedule submission

- How revisions are handled

- Penalties for scheduling failures

Energy Banking

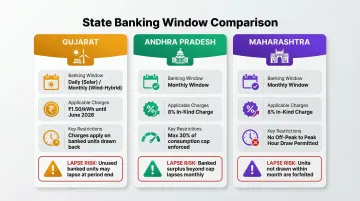

When your renewable plant generates more than you consume in a given period, the surplus is "banked" with the DISCOM and drawn down later. Banking windows (daily, monthly, quarterly, annual) determine how much value you capture.

State banking policies vary significantly—and the differences directly affect your net realized tariff:

| State | Banking Window | Charges/Conditions |

|---|---|---|

| Gujarat | Daily (Solar), Monthly (Wind/Hybrid) | ₹1.50/kWh banking charge until June 2026 |

| Andhra Pradesh | Monthly | 8% in-kind charge; capped at 30% of monthly consumption |

| Maharashtra | Monthly | 8% in-kind charge; off-peak banked energy cannot be drawn during peak slots |

Watch the lapse clause: unutilized banked energy typically expires at the end of the settlement cycle, compensated at only 75% of the PPA tariff. Not all states permit banking at all—confirm your DISCOM's policy before signing.

Deemed Generation

While banking protects buyers from surplus, deemed generation works in the opposite direction—protecting the seller. If you fail to draw contracted energy due to plant shutdowns, demand reduction, or scheduling failures, the seller is entitled to payment as if generation had occurred.

Financial exposure example: For a 10 MW solar PPA at ₹4/kWh with 20% CUF and a 30% deemed generation trigger over 15 years, a single quarter-long shutdown during which you're invoiced for deemed generation could cost ₹1.05 crore in that quarter alone—₹35 lakh per month for energy you never received.

Limit this exposure through contract negotiation:

- Negotiate a "deemed generation holiday" for pre-agreed annual maintenance shutdowns

- Exclude force majeure events (natural disasters, pandemics) from deemed generation triggers

- Cap liability at 10–15% of annual contracted volume

- Require the seller to attempt alternate off-take before invoking deemed generation

Risk and Exit Clauses: Default, Termination, Force Majeure, and Curtailment

Events of Default

The PPA must define default events for both parties with clearly defined cure periods (typically 30–60 days) before default is declared.

Buyer default events:

- Missed payments beyond cure period

- Bankruptcy or insolvency

- Unauthorized transfer of the agreement

Seller default events:

- Failure to achieve Commercial Operation Date (COD) within the longstop date

- Persistent underperformance below minimum generation guarantee

- Failure to maintain required insurance

- Project abandonment

India-specific risk: Developer default clauses should address delays caused by grid connectivity failures (STU/CTU delays) and land acquisition holdups—both common execution risks. CTU recently revoked grid connectivity for over 6.3 GW of delayed renewable projects, highlighting the materiality of this risk. Ensure developers are accountable for these delays, not just force majeure.

Termination Amount

Voluntary early termination by the buyer typically triggers a termination payment calculated as the net present value of the developer's lost future revenues, factoring in remaining contract term, current market prices, and asset depreciation.

Cost of flexibility: Model termination scenarios at Year 5, Year 10, and Year 15 before signing. In some SECI model PPAs, damages are capped at 24 months of tariff for the contracted capacity rather than open-ended NPV calculations—a significantly more favorable structure for buyers.

Lower-cost exit option: Before accepting termination costs at face value, check whether the contract allows assignment to a successor entity—for example, if you sell the manufacturing facility. This route is often cheaper than triggering a termination payment.

Force Majeure and Curtailment

Force majeure covers acts beyond either party's control—natural disasters, wars, pandemics—and typically suspends performance obligations without penalty during the event.

Curtailment works differently: it's a grid operator's instruction to reduce generation due to network congestion or excess supply. Curtailment is NOT a force majeure event and must be addressed in a separate curtailment clause specifying:

- Whether the developer is compensated by the grid operator

- Whether your payment obligation is suspended or adjusted

- Curtailment caps (for example, maximum 10% of annual generation exempt from compensation)

India-specific precedent: Renewable curtailment by SLDCs has been recurring in wind-heavy states like Tamil Nadu, Rajasthan, and Gujarat. In a landmark 2021 APTEL ruling, the tribunal directed that solar generators be compensated at 75% of the PPA tariff for arbitrary curtailment unrelated to grid security, using a POSOCO-developed methodology.

Negotiation strategy: Negotiate "must-run" status acknowledgment in your PPA and a curtailment cap to limit exposure. If curtailment exceeds the cap, demand the seller substitute energy or provide compensation.

Regulatory and Environmental Clauses: Change-in-Law, Open Access, and RECs

Change-in-Law

This clause defines how the PPA responds when new taxes, levies, or regulatory changes materially alter economics for either party. Typical triggers include revision of open access charges, new transmission surcharges, or changes to wheeling charges by state DISCOMs.

Two structures:

- Pass-through: The buyer absorbs 100% of the cost increase, with no sharing mechanism

- Shared adjustment: Costs split between both parties by a pre-agreed formula (e.g., 50/50)

Indian C&I buyers must scrutinize this clause given the volatility of state-level open access regulations. For instance, CERC recognized the GST hike from 5% to 12% on solar equipment as a valid change-in-law event — entitling developers to seek a corresponding upward revision in contracted tariffs. Without clear pass-through language in the PPA, buyers can face unexpected cost exposure from similar regulatory shifts.