Introduction

Grid tariffs for India's commercial and industrial sector are climbing 3-5% annually. Renewable Purchase Obligation (RPO) compliance deadlines are tightening. And global frameworks like RE100 and CDP are making clean energy sourcing a hard requirement for many export-linked and large-cap businesses. For C&I buyers, renewable energy procurement is now a direct cost and compliance issue—not a sustainability afterthought.

Procurement, however, is not a single decision. Renewable energy sourcing in India spans multiple distinct pathways—each with different cost structures, regulatory requirements, and suitability based on your state, load size, and financial model.

A pathway delivering ₹3-5 per unit savings in one state may turn uneconomical in another due to surcharge variations. A model suited to a 10 MW steel plant may be entirely inaccessible to a 500 kW warehouse.

This article explains the four main procurement pathways available to regional C&I buyers: Open Access Corporate PPA, Group Captive Power Plant, Behind-the-Meter Solar, and RECs/Green Tariffs. You'll learn how each works, what distinguishes them, and how to select the right fit for your business.

Key Takeaways

- Renewable energy procurement pathways are the structured routes C&I buyers use to source green power: bilateral contracts, onsite generation, or market-based certificates

- India's four main pathways are: Open Access Corporate PPA, Group Captive Power Plant (GCPP), Behind-the-Meter/Rooftop Solar, and RECs/Green Tariffs

- State-level regulations, open access charges, and cross-subsidy surcharges vary sharply across regions, making pathway economics highly location-dependent

- Larger consumers (1 MW+) typically unlock greater savings through PPAs or GCPP; smaller buyers can use rooftop solar or RECs

- Choosing the right pathway requires matching your load profile, state regulations, financial capacity, and sustainability goals to the correct structure

What Are Renewable Energy Procurement Pathways?

Renewable energy procurement pathways are the distinct contractual, financial, and regulatory mechanisms through which C&I buyers source power generated from solar, wind, or hybrid projects—rather than relying solely on Discom grid supply.

These pathways are used across India's industrial and commercial sectors—from steel plants and textile mills to IT parks, data centres, hospitals, and warehouses. They serve three core business objectives: controlling energy costs, meeting RPO compliance obligations, and demonstrating sustainability credentials to stakeholders and supply chain partners.

Each pathway has direct financial and regulatory consequences:

- Landed cost per unit of electricity you pay

- Your ability to claim green attributes for ESG reporting

- Regulatory complexity you must navigate

The pathway you choose can mean paying ₹4.5 versus ₹7 per unit after all charges. It determines whether you can meet RE100 requirements—and whether your procurement takes weeks or requires months of legal structuring for equity arrangements.

Why Procurement Pathways Matter for Regional Buyers in India

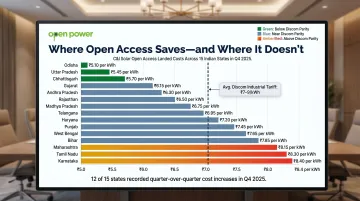

India's power market is not uniform. Each state operates its own Discom structure, open access regulations, cross-subsidy surcharges (CSS), wheeling and transmission charges, and RPO targets. A pathway that delivers strong economics in Karnataka may be financially unviable in Maharashtra due to higher surcharge rates.

Corporate customers account for 51% of India's total power consumption, yet direct renewable procurement accounts for only 6% of corporate electricity demand. That gap exists largely because buyers choose the wrong pathway for their state and load profile.

With industrial tariffs ranging from ₹7–9 per kWh in major states and escalating 3–5% annually, the cost of a wrong choice compounds quickly.

What goes wrong without the right pathway:

- Buyers who default to purchasing RECs without evaluating PPAs may satisfy compliance but miss 30-40% cost savings

- Organizations pursuing open access PPAs without assessing state-level charges find that CSS and additional surcharges erase projected savings—in Q4 2025, third-party open access savings turned negative in Punjab and Tamil Nadu

- Large consumers with high baseload who miss the GCPP route leave significant money on the table, since GCPP users are exempt from CSS

The numbers confirm how much state context shapes outcomes. Landed costs for C&I solar open access ranged from ₹5.0 to ₹8.4 per kWh across 15 states in Q4 2025, with 12 of 15 states recording quarter-over-quarter increases. A buyer in one state can save significantly; a buyer in another, using the same procurement structure, can end up paying more than the grid rate.

Types of Renewable Energy Procurement Pathways

No single procurement pathway suits all buyers. The optimal route depends on your connected load, location, financial model, sustainability commitments, and appetite for regulatory complexity.

These four pathways are not mutually exclusive—some large consumers combine strategies (rooftop solar plus a PPA) to maximize coverage and savings.

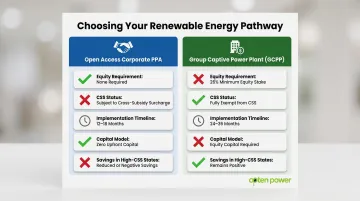

Open Access Corporate Power Purchase Agreement (CPPA)

How it works:

A Corporate PPA is a long-term bilateral contract (typically 10-25 years) between a C&I buyer and a renewable energy developer.

You source power from an off-site solar, wind, or hybrid project — delivered through the state or inter-state transmission network under open access provisions. You pay a fixed or indexed tariff to the developer and avoid Discom retail supply rates.

How it differs:

Unlike rooftop solar, the generation asset is off-site and you don't own the infrastructure. Unlike GCPP, you hold no equity stake—the relationship is purely contractual. You are subject to full open access charges including CSS, transmission and wheeling charges, and scheduling fees.

Best suited for:

- Large C&I consumers with connected load of 1 MW or more

- Industries with stable, high-load-factor consumption: steel, cement, manufacturing, data centres, IT parks

- Buyers in states with competitive open access regimes and favourable landing costs

Strengths and trade-offs:

Solar open access tariffs typically range from ₹3.0 to ₹4.5 per kWh, offering substantial savings versus Discom industrial tariffs of ₹7-9 per kWh. Key strength is long-term price certainty and ability to claim bundled RECs for ESG reporting.

That said, state-level open access charges—especially CSS—can significantly reduce net savings. Q4 2025 analysis shows that rising PPA tariffs and OA charges narrowed margins, turning savings negative in some states. Gujarat increased its additional surcharge by 22% (from ₹0.82 to ₹1.00 per kWh), narrowing OA savings substantially.

Thorough state-specific cost modelling is essential before signing any PPA.

Group Captive Power Plant (GCPP)

How it works:

An India-specific procurement model where the C&I buyer acquires a minimum 26% equity stake in a renewable energy project and commits to off-taking at least 51% of the project's annual generation. This qualifies you as a "captive user" under the Electricity Act, 2005. Legally, that means you are classified as a partial owner of the generating asset — not a third-party consumer.

How it differs:

The defining differentiator: GCPP consumers are statutorily exempt from cross-subsidy surcharge (CSS)—the charge that most significantly erodes savings under a standard open access PPA. This makes GCPP the most cost-efficient pathway in high-CSS states. In contrast to a PPA, this pathway requires equity capital commitment upfront.

Best suited for:

- Large industrial buyers (typically 5 MW and above) with long-term, baseload consumption profiles

- Fertiliser conglomerates, cement plants, heavy process industries

- Consortium arrangements among multiple medium-to-large buyers where individual load alone may not qualify

Real-world examples:

- Tata Power Renewable Energy commissioned a 198 MW group captive wind project in Karur, Tamil Nadu (55 WTGs, 3.6 MW each)

- Equinix commissioned a 26.4 MWp group captive solar project with CleanMax

Strengths and trade-offs:

CSS exemption delivers meaningfully better economics than open access PPA in high-surcharge states. Mercom's Q4 2025 analysis indicates that group captive savings generally exceeded third-party OA savings because of CSS and additional surcharge exemption—in states where third-party savings were negative, group captive remained positive.

The trade-off is complexity: equity structuring, corporate governance of the SPV, and longer project timelines (24-36 months versus 12-18 months for a PPA). This pathway demands greater upfront commitment and legal sophistication.

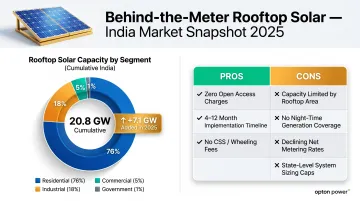

Behind-the-Meter: Rooftop and Onsite Solar

How it works:

Rooftop or onsite solar installs panels on your premises—rooftop, carport, or available land—with power consumed directly at the site. Because generation never enters the grid, this pathway bypasses open access charges, CSS, wheeling, and transmission costs entirely.

Surplus generation can be exported under net metering arrangements, though the value varies by state. Many states have shifted toward gross metering and net billing variants, with 22 state and UT regulations adopting gross metering provisions.

Best suited for:

- Buyers with significant rooftop or land availability relative to consumption

- Commercial complexes, warehouses, hospitals, hotels, IT parks where rooftop area is substantial

- Supplementary layer for larger industrial buyers wanting to reduce grid dependence during high-tariff daytime hours without open access complexity

Market growth:

India added 7.1 GW of rooftop solar in 2025, a 123% YoY jump from 3.2 GW in 2024. Cumulative rooftop capacity reached 20.8 GW as of December 2025. Segment shares: Residential 76%, Industrial 18%, Commercial 5%, Government 1%.

Strengths and trade-offs:

Zero open access charges is a clear economic advantage. Fastest implementation timeline (typically 4-12 months). Visible sustainability signal for stakeholders.

Capacity is constrained by available rooftop or land area and typically covers only a portion of total consumption. State-level caps on system sizing and declining net metering rates limit scalability further. This pathway also doesn't address night-time or cloud-impacted load.

Renewable Energy Certificates (RECs) and Green Tariffs

How it works:

RECs are tradeable instruments (each representing 1 MWh of renewable generation) that C&I buyers can purchase on the Indian Energy Exchange (IEX) to claim renewable consumption without changing their physical power supply. Green tariffs are Discom-sponsored programs allowing buyers to pay a premium for renewable-attributed electricity within their service territory.

Unlike the other pathways, both options involve no change to physical supply arrangement—they are purely attribute-based procurement tools.

Best suited for:

- Buyers needing to meet RPO compliance quickly

- Organizations requiring initial ESG reporting credentials (sustainability disclosures, supplier audits) where load profile, state regulations, or infrastructure constraints make PPA or GCPP impractical

- Bridge solution while longer-term procurement arrangements are structured

Market data:

In FY26, IEX traded 187.20 lakh REC units; Q4 FY26 volume was 71.70 lakh units. March 2026 clearing price: ₹340 per REC. RECs are explicitly recognized as instruments for obligated entities to meet RPO under CERC regulations.

Strengths and trade-offs:

Highly flexible—no long-term contracts, minimum load requirements, or infrastructure investment needed. Fastest to implement.

RECs do not reduce actual energy costs, and rising floor prices make them increasingly expensive over time. International sustainability frameworks also draw a clear line: RE100 Technical Criteria and CDP Scope 2 guidance both prefer physical procurement with additionality over market-based RECs. For organizations with global reporting commitments, RECs work best as a complement to physical procurement — not a substitute.

How to Choose the Right Renewable Energy Procurement Pathway

The right pathway is determined not by what is most popular in the market, but by structured assessment of your specific load, location, financial model, and goals. Misalignment on even one factor can quickly erode the business case.

Factor 1 — Load size and consumption profile

Connected load and annual consumption directly determine which pathways are accessible:

- Sub-1 MW buyers: Typically limited to rooftop solar or RECs due to minimum open access thresholds

- 1-5 MW buyers: Can access open access PPAs in qualifying states; most state electricity regulatory commissions set minimum connected load for open access at 1 MW, though some states allow intrastate open access from lower thresholds

- 5 MW+ buyers: Unlock full economics of GCPP and large-scale PPAs with high load factors

Also assess load factor. If you have 24x7 baseload consumption (steel, cement, textiles), you benefit from wind or hybrid projects. If consumption is daytime-only (commercial complexes, IT parks), solar-only PPAs may not fully serve night-time industrial loads.

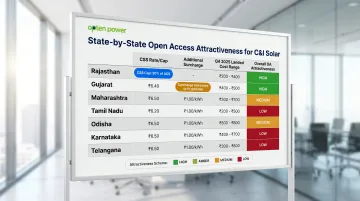

Factor 2 — State-level regulatory and cost landscape

The same PPA tariff delivered in two different states can yield dramatically different net savings once state-specific open access charges, CSS, banking charges, and scheduling norms are applied.

Q4 2025 data shows landed costs for C&I solar open access ranged from ₹5.0 to ₹8.4 per kWh across 15 states — highest in Maharashtra, Tamil Nadu, and Karnataka; lowest in Odisha, Uttar Pradesh, and Chhattisgarh. State-level policy shifts compound this further: Rajasthan caps CSS at 20% of average cost of supply for up to 12 years, while Gujarat raised its additional surcharge to ₹1.00 per kWh in Q4 2025, narrowing open access savings.

Map your Discom's landing cost and surcharge regime before shortlisting any pathway. Platforms like Opten Power's Real-Time Discom Intelligence provide standardised, up-to-date landing prices across states, enabling state-aware pathway comparisons without manual regulatory research.

Factor 3 — Financial structure and capital availability

Two structural choices shape every pathway decision:

- CAPEX models: You own the asset (as in a self-funded rooftop system); eligible for accelerated depreciation benefits

- OPEX models: Developer owns the asset; you pay per-unit tariff under a PPA or GCPP lease structure with no upfront capital outlay

GCPP requires a minimum 26% equity stake upfront but delivers stronger unit economics through CSS exemption and per-unit savings of ₹3–5.

Before committing, run IRR and payback period analysis across options — factoring in interest rates, depreciation benefits, and contract tenure. Rooftop solar typically pays back in 3–4 years; GCPP projects often reach IRRs in the 18–24% range depending on state and load profile.

Factor 4 — Sustainability reporting and compliance obligations

Identify whether your mandate is:

- RPO compliance only: RECs may suffice, as they are explicitly recognized for RPO compliance

- ESG reporting to domestic standards: PPAs or GCPP provide stronger credentials

- International commitments (RE100, CDP Scope 2): Require higher-integrity procurement with additionality—typically a new-build PPA or GCPP

RE100 Technical Criteria introduce commissioning or repowering date limits for eligible supply and strengthen additionality expectations over time. Mismatching the pathway to the reporting standard creates either over-engineering or reputational risk.

Factor 5 — Implementation timeline and organisational capacity

- Rooftop solar: Fastest (4-12 months)

- Open access PPAs: Can reach financial close in weeks on streamlined platforms

- GCCPs: Typically require 24-36 months for equity structuring and project commissioning

Buyers with urgent compliance deadlines or upcoming sustainability disclosures should factor realistic timelines into pathway selection and not assume all options are equally fast to execute.

What to Check Before Finalising a Renewable Energy Procurement Pathway

Don't Choose Based on Headline Tariff Alone

Many buyers compare PPA tariffs to their Discom rate without accounting for CSS, transmission charges, wheeling, scheduling, and banking charges. These add-ons can significantly reduce or eliminate projected savings. Always model the complete cost stack for your state before signing.

Verify Current State Regulations

Open access rules, CSS rates, and net metering policies change frequently. A pathway viable 12 months ago may have become economically unviable due to regulatory revision. Karnataka proposed a reduced wind tariff cap of ₹3.24 per kWh for FY 2027-2029; Telangana temporarily removed its additional surcharge, improving open access savings. Always verify current regulatory status with an authorised energy advisor before proceeding.

Scrutinise Contract Terms and Long-Term Flexibility

Buyers focused on upfront savings sometimes sign long-tenure contracts without reviewing exit provisions, force majeure clauses, deemed generation penalties, and renegotiation rights.

A 25-year PPA that doesn't account for future technology disruption, load reduction, or business model changes creates locked-in risk. Have contracts reviewed by both legal and commercial advisors before execution.

Before finalising any pathway, confirm you've checked:

- Complete landed cost stack, including CSS, wheeling, and scheduling charges

- Current state-level open access and net metering regulations

- Contract exit provisions, deemed generation clauses, and renegotiation rights

- Alignment between contract tenure and your business's long-term load forecast

Conclusion

India's four main procurement pathways—Open Access PPA, Group Captive, Rooftop Solar, and RECs—each serve different buyer profiles, load sizes, and regional conditions. Choosing the right pathway matters as much as the decision to procure renewable energy in the first place.

State-level regulatory complexity, consumption scale, financial model, and sustainability obligations all shape the optimal pathway. A structured, fact-based assessment of these factors — rather than market convention or peer comparison — leads to lasting cost reduction and credible sustainability outcomes.

With India's non-fossil capacity reaching 283.46 GW as of March 2026 and corporates still representing only 6% of direct renewable procurement, the gap between available supply and active buyers remains wide. The pathway you select now determines the tariff you lock in, the regulatory exposure you carry, and the timeline on which savings actually materialize.

Frequently Asked Questions

What is the difference between an Open Access PPA and a Group Captive Power Plant in India?

An Open Access PPA is a contractual off-take arrangement where the buyer pays a tariff to a developer without owning equity. A GCPP requires at least 26% equity ownership, which qualifies the buyer as a captive user and exempts them from cross-subsidy surcharge. GCPPs are financially superior in high-CSS states but require more upfront capital.

Can medium-sized enterprises below 1 MW access corporate renewable energy procurement in India?

Sub-1 MW consumers generally cannot access open access PPAs due to minimum load thresholds set by state regulations. Alternatives include behind-the-meter rooftop solar (no minimum load), REC purchases on the exchange, or consortium models where smaller buyers pool demand to meet thresholds.

How do state-level Discom regulations affect renewable energy procurement economics?

Each state applies its own cross-subsidy surcharge, wheeling and transmission charges, and banking norms to open access consumers. The same PPA tariff can result in significantly different net savings across states. Buyers must model the full landed cost stack specific to their Discom before selecting a procurement pathway.

What is the minimum connected load required to sign a corporate PPA in India?

While thresholds vary by state, most state electricity regulatory commissions set the minimum connected load for open access at 1 MW, though some states allow intrastate open access from lower thresholds. Inter-state open access typically requires higher load levels. Verify the applicable threshold in your state before initiating a PPA process.

Are RECs sufficient to meet Renewable Purchase Obligation (RPO) compliance in India?

RECs are accepted under the Electricity Act and CERC regulations, making them sufficient for domestic RPO compliance. However, they do not reduce actual energy costs and fall short of high-integrity international frameworks like RE100 or CDP Scope 2, which require physical additionality through new-build PPAs or GCPPs.

How long does it typically take to commission renewable energy under an open access arrangement?

Timelines depend on whether the project is greenfield or already commissioned. A new greenfield project typically takes 18–24 months from contract signing to delivery. Procuring from an existing asset via a secondary PPA can reduce contracting to 3–6 months, with power delivery beginning almost immediately.